A capital gains tax that applies interest to gains accumulated before an asset is sold would align with New Zealand’s principles-based regime, an international tax expert told Treasury.

Michael Keen, a former deputy director of the International Monetary Fund’s Fiscal Affairs Department and university academic, gave a public lecture at the Treasury on Wednesday.

He was responding to Inland Revenue’s recent long-term insight briefing which looked at how to design a “durable” tax system which could respond to fiscal pressures.

Keen said this should be about establishing a set of stable tax bases which could be adapted to meeting changing revenue needs and distribution priorities.

“Underlying that is the cruder question of, well, if New Zealand had to raise more revenue, how would you best go about it? We know there are these fiscal pressures, where might the money come from if needed?”

There could be a need to raise almost another 6% of gross domestic product to cover the rising cost of healthcare and superannuation by 2060. This could be met through policy reforms, improved efficiency, higher taxes, or some combination of all three.

Keen didn’t give any particular policy prescription as his talk was focused mainly on technical aspects of his tax design research. However, he did drop hints about using GST, user levies, and an advanced capital gains tax to widen the revenue base.

While he didn’t speak about these at length, the economist and tax expert said it was best to start with user fees, corrective taxes, and taxes on economic rents as these improved the market allocation of resources.

This means things like road user charges and co-payments for public services, excise taxes on things like emissions, alcohol, and tobacco, and (theoretically) excess profits above the necessary return to incentivise an investment.

But those taxes aren’t generally enough to run a government or meet distributional needs and so policymakers turn to more “distortive” taxes — those which may worsen market allocation.

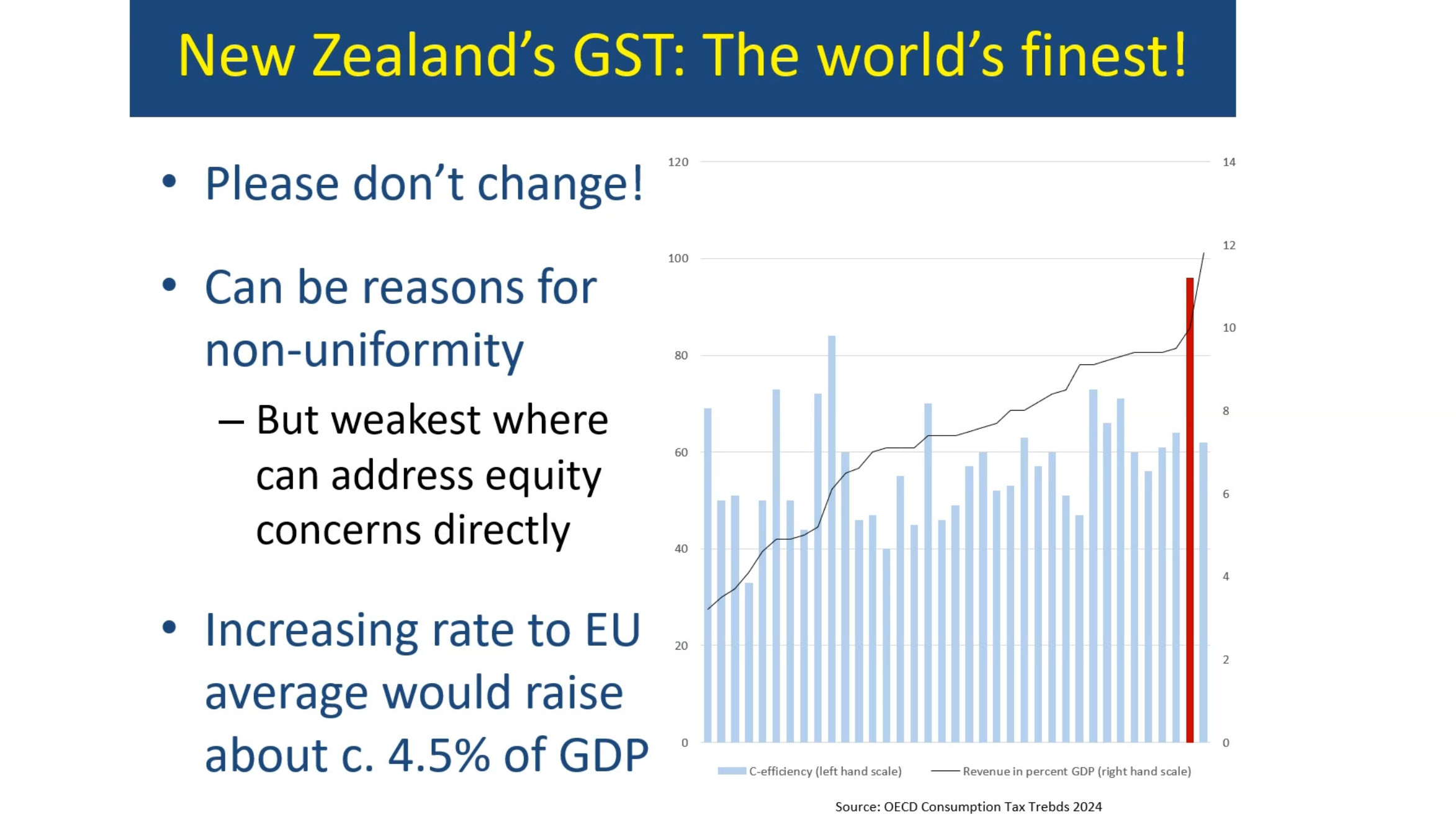

‘Please don’t change!’

Like many tax experts, Keen heaped praise on New Zealand’s comprehensive GST regime and implored policymakers not to mess it up.

“GST, well, I just want to say, don’t change it. Not much more to say about that… it’s pretty amazing, really, with a rate of 15% that you’re right up there with [such] a broad base. So don’t change it.”

The European Union’s average consumption tax rate was 22%, although often with carve outs and exemptions for various products and services. New Zealand could raise roughly 4.5% of GDP by lifting GST to that same rate, Keen said.

But a higher rate would likely require an offset for low income earners such as a means-tested tax credit, a flat payment to eligible groups, or a smart-card which deducts GST at purchase.

In its insight briefing, Inland Revenue modelled the possibility of raising $5 billion annually by lifting GST to 18% and providing a tax credit to families earning less than 60% of the median disposable income.

A slide from Keen’s lecture imploring policymakers not to meddle with GST

However, Keen focused most of his speech on the absence of a comprehensive capital gains tax, which he saw as being a flaw in New Zealand’s otherwise excellent tax regime.

“New Zealand’s principle-based income tax is based on the idea of a comprehensive income tax. That is, a tax on income from all sources added up to which you apply a progressive tax schedule,” he said.

And any textbook description of a comprehensive income tax base would include accrued capital gains as a form of income, whereas New Zealand taxes only certain capital gains.

It would make more sense to pass a law saying everything is subject to a capital gains tax and then list whatever exemptions were seen as beneficial or politically necessary, Keen argued.

“All I can do is put that thought in your mind. In terms of the politics of going in that direction, I’m going to be agnostic and even more ill-informed than on other topics”.

Living ‘the high life’ tax free

Many experts have encouraged New Zealand to broaden its capital gains tax base. Keen echoed these voices and spent a portion of his talk discussing a technical variation on the tax.

One complaint about CGT is that it is only paid when an asset is sold. This encourages owners to hold onto businesses or properties when it might otherwise be more efficient to sell.

Economists call this “the lock-in effect” and it reduces investment efficiencies and makes revenue earned from capital gains unpredictable. But it also creates equity problems.

“Wealthy people can have unrealized capital gains. They might want to borrow against those gains. And, you know, live the high life without, without incurring a [tax] liability,” Keen said.

Depending on inheritance tax settings, unrealised assets may be able to be passed onto the next generation to borrow against without ever being properly taxed.

“So taxation on realisation rather than accruals, as currently done, creates both these efficiency and these equity issues,” Keen said.

One way to address the problem is to tax gains when an asset is sold but also to charge interest on the liability as it builds up.

In practice, investors would accrue an annual tax obligation on their capital gains but could defer payment until sale, with interest added, removing the incentive to hold assets purely to avoid tax.

Keen said this would be straightforward for publicly traded assets with clear market prices, but more complicated for privately held ones. In those cases, the tax could be based on an assumed rate of return each year, with liabilities calculated that way.

The tax expert admitted this type of policy had only been tried once, in Italy in the 1980s, and had failed. But he thought it may be possible with more advanced technology and systems.

“I, at least, find it surprising that people don’t talk more about these schemes,” he said.

A well-designed capital gains tax would also reduce the need for wealth taxes, which aren’t common in other jurisdictions and are more distortive than alternatives.

“If you have a proper tax on capital income, including dealing with unrealised capital gains, what does a wealth tax add? And I think the answer will be, not much.”