The slow, relentless, but orderly slide in term deposit offer rates continues.

Today, BNZ ended its 4% one year special rate, reverting it to 3.85%.

Rates in the high 3%s are where this market has settled down to.

But there are exceptions, and among those there will be opportunities. To be fair however, when rates get this low there are only relative benefits to be found.

Rates above 5% have virtually disappeared, even among non-bank deposit takers (NBDT). But there is still one, from Gold Bank Finance.

Rates above 4% from banks are now only offered for the longer terms of three years and longer (although Westpac still has a 4% rate for two years).

Among banks, for terms less than one year, only Rabobank, Bank of China, and ICBC still offer 4% or more. The chance these will last much longer is low, however. Among NBDTs they are vanishing too, although these 4%+ offers may last a bit longer.

The rate curves have flattened notably. The difference between six months and one year has fallen to eight basis points and is no longer significant. This world is essentially flat.

If you rely on term deposit interest for part of your income, the lower rates go, the more attractive a switch will seem. There may be historic memories lingering about the risks of depositing with NBDTs, but that risk has now substantially passed, and can be managed by splitting investments between institutions.

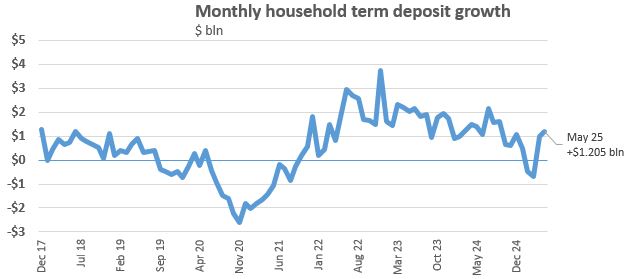

Funds flows into household term deposit accounts is still rising at more than $1 billion per month, which is likely more than banks need at present.

There is plenty of evidence that mortgage borrowers are quite comfortable switching banks, but that evidence is sparse on the deposit side. Bank deposit books ‘replicate’ strongly still, even when rates are low. With little rate variation and the actual reward being low, motivation to change will be low too. But at least now the field is open a tiny bit wider with the taxpayer guaranteeing accounts to $100,000, even at authorised NBDTs.

When you invest, always check how interest is compounded. Depending on how much you are committing, compounding more often is materially better. But some banks advertise their “interest at maturity” rates different to their compounding rates, which for some can be set a little lower. Both Kiwibank and Rabobank do this, although most other main banks don’t.

Use the calculator at the foot of this article to see the differences.

We should also point out that after-tax returns can be enhanced for some savers with higher tax rates by the choice of PIE structures. Not all institutions offer these, but most of the main banks do. For a nine month bank offer, they can be boosted by about 30 basis points going this way. In some cases that will make up any difference, or more.

Always ask a bank for a better rate. Many bank staff have discretion to offer more than the advertised rate. (And check your bank’s app offers as they too are often enhanced to retain you). But in this environment don’t get your hopes up for a positive response. Carded rates are likely to now be the ‘best rate’, except in quite special circumstances.

Use the term deposit calculator here, or the one below the table, to calculate your expected net after-tax returns.

The latest headline term deposit rate offers are in this table after the recent changes over the past month. The pink background colour-code indicates 5%+ rates still available. The yellow colour code for those under 4%. Bolded rates are the “best-bank”, the highest carded rate from any bank at this time.

This table only lists institutions covered by the Depositor Compensation Scheme.

Select chart tabs

1 year %

30 days %

90 days %

6 months %

2 years %

3 years %

4 years %

5 years %

Select chart tabs

1 year %

2 years %

3 years %

4 years %

5 years %

7 years %

10 years %