Weil, Gotshal & Manges LLP are most popular:

within Environment, Technology and Energy and Natural Resources topic(s)

in United States

As take privates continue to play a meaningful role in

sponsor-backed transaction activity, below we compare key deal

terms from sponsor-backed take private transactions announced in

2024 to those announced in 2025 (through May 2025). While the pace

of sponsor-backed take-private deals has somewhat slowed, the below

analysis reveals that many of the differences in deal terms across

the two periods are modest. However, in some cases, we observed

meaningful differences in deal terms across the two time periods

which may suggest evolving market dynamics worth monitoring.

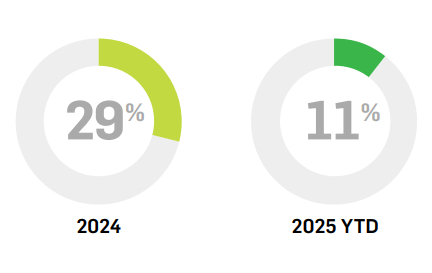

CLUB DEALS

Club deals are complex, as they involve multiple transactions

within a transaction, both to execute the take private and to

organize the business effective as of closing. Club deals accounted

for 29% of sponsor-backed take privates in 2024, reflecting a

willingness among sponsors to partner on large transactions and

driven in part by the resurgence of the so-called “mega

deals” (deals of at least $1 billion). By contrast, we have

only observed one club deal so far in 2025, suggesting a possible

shift toward single-sponsor funded transactions (and perhaps

smaller transactions), though the trend may normalize as the year

progresses.

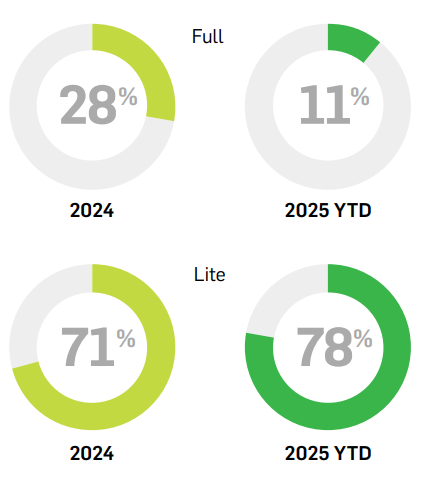

SPECIFIC PERFORMANCE

In 2024, the “specific performance lite” construct

(allowing the target to compel sponsor’s equity financing only

if buyer’s debt financing is available) reemerged as the

preferred market remedy to address an acquirer’s financing

failure and a target’s closing risk in sponsor-backed going

private transactions, due in part to the increase in debt-financed

transactions. Among 2024 deals, 28% provided for full specific

performance (whereby the target can force a closing upon

satisfaction or waiver of the applicable closing conditions,

regardless of whether an acquirer’s debt financing is

available) while 71% contemplated specific performance lite. As we

predicted in Weil’s 2024 Going Private Study, the prevalence of

specific performance lite over full specific performance has

continued in 2025 – with 11% of deals contemplating full specific

performance and 78% using specific performance lite. This seems to

indicate a continued, and perhaps growing, ability of sponsors to

limit financing risk.

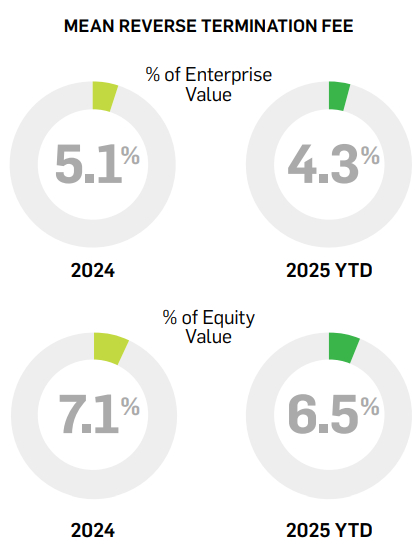

REVERSE TERMINATION FEES

The average reverse termination fee (“RTF”) as a

percentage of enterprise value and equity value in 2024 was 5.1%

and 7.1%, respectively. For 2025 deals, those averages

significantly declined to 4.3% and 6.5%, respectively. The mean RTF

of 4.3% of target enterprise value is much lower than expected, and

moreover, much lower than the mean amounts observed over the past

few years (since 2018, the mean RTF as a percentage of enterprise

value has been between 5 and 6% except in 2021 where it exceeded

6%). While these changes may normalize as the year progresses, they

may reflect slightly more sponsor-favorable risk allocations or

changes in deal leverage.

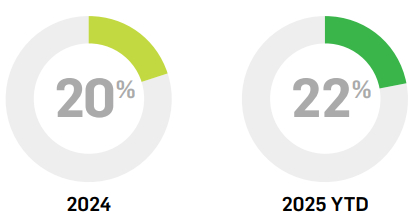

GO-SHOPS

Go-shop provisions appeared in 20% of 2024 deals and 22% of 2025

deals. The negligible increase suggests continued selectivity in

their use, which is typically tied to the target’s process. As

we’ve previously noted in our annual Weil Going Private Study,

the use of go-shop provisions in take private transactions

generally fluctuates over time due to the fact specific nature of

whether a target company’s board feels compelled to include a

go-shop provision, which is often driven by the extent to which the

company has engaged in a pre-signing market check.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.