We are going to borrow a phrase from ACC’s latest advertising campaign and describe October’s housing market results as a “have a hmmm” month.

That’s because on the face of it, October’s figures look reasonably positive for the start of the summer season, but there are a couple of things that could point to trouble ahead.

Although it’s usually house prices that get the most attention when considering the state of the market, it’s the volume of housing sales that’s the most important indicator of where it’s headed.

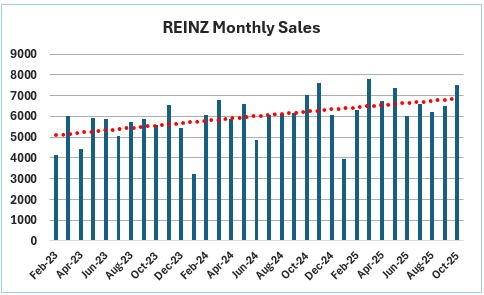

October’s sales weren’t too bad, with the Real Estate Institute of New Zealand recording 7505 residential sales for the month, up 6.4% compared to October last year.

However, monthly sales can be erratic. To get a better idea of what’s happening with residential property sales, take a look at the first graph below, which shows the REINZ’s monthly sales from February 2023.

The important feature of the graph is not the monthly sales measures, but the dotted red trend line, which evens out the bumps and dips of the monthly figures.

What it shows very clearly is that sales numbers have been slowly but steadily improving since the beginning of 2023.

So although the main focus of commentary on the housing market in recent times has been on softening prices, the underlying strength of the market as measured by sales, has been steadily improving.

So if sales numbers are looking reasonably good, what’s really happening with prices?

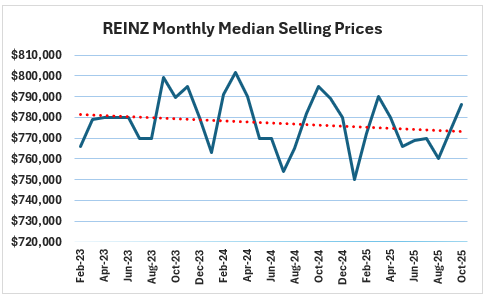

Again, a picture is worth a thousand words, so have a look at the second graph below, which plots the REINZ’s median selling price since February 2023.

As with sales, the median prices are lumpy, but its the dotted red trend line that’s important. And it shows a slow but steady decline in median prices that remains within a fairly narrow range. At best you could say that prices are flat but with an easing bias.

So overall, sales volumes are improving but prices remain soft.

A key reason for this is the high number of properties available for sale.

In short, more people are wanting to sell properties than are wanting or able to buy them. This has created a buyer’s market and that has kept a lid on prices, even as mortgage interest rates have declined.

However, an emerging feature of the market over the last few months is that vendors have started to become more realistic in their price expectations and are realising they are not going to get the prices they might have achieved back in the boom years of 2021/22.

The lower rating valuations released for the Auckland market earlier this year were a wake up call for many vendors, and gave a push to the trend of lower asking prices.

That has narrowed the gap between the prices vendors are hoping to receive and buyers are prepared to pay, resulting in more deals being done, providing the modest upward momentum of sales, while prices remain in check.

This has resulted in steady declines in both the overhang of unsold stock each month and in the dropouts, which is the number of properties taken off the market each month.

Interest.co.nz estimates the overhang of unsold stock at the end of each month has steadily declined from more than 30,000 in April this year to just over 23,000 in October, while the number of properties being taken off the market each month has halved over the same period.

Looking ahead to the major summer selling season, we are likely nearing the end of the current easing cycle for interest rates, so any further falls in mortgage rates will probably be relatively modest.

It will likely be the volume of new listings coming up for sale and the stock levels they create that will determine where the market heads from here.