There’s a very good chance New Zealand’s unemployment rate has reached its highest level in eight and a half years.

We’ll find out on Wednesday, August 6, when Statistics NZ releases the full suite of labour market figures for the June quarter – including the unemployment numbers, the employment numbers and wage rise information.

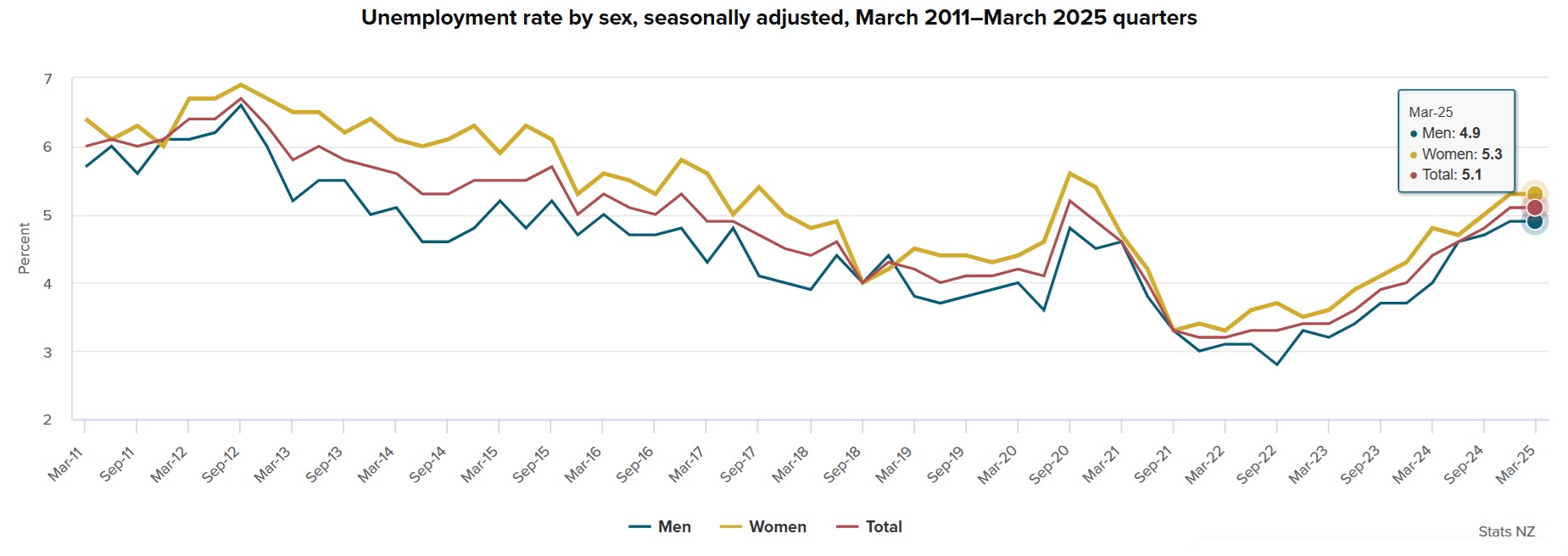

As of the March quarter, we had unemployment of 5.1%, which was the same as in the December 2024 quarter – giving rise to some hopes that the rate might have peaked.

However, it’s looking increasingly likely our economy’s had another ‘June swoon’. High frequency economic indicators are suggesting that GDP, which grew 0.8% in the March quarter might have stalled completely in the June quarter.

And a stalled economy means fewer jobs.

The Reserve Bank as of its May Monetary Policy Document forecasts was picking an unemployment rate of 5.2% for the June quarter, staying at 5.2% in the September quarter and then falling to 5.1% in the December 2025 quarter. The RBNZ forecasts the rate to gradually keep declining next year, down to 4.7% by December 2026.

However, based on more recent information than the RBNZ had when it made those forecasts, economists are now mostly picking a rate of 5.3% for the June 2025 quarter.

If that indeed proves to be the case, it will be the highest rate since December 2016, when the rate was also 5.3%. Should there be an unpleasant surprise and June quarter unemployment actually hits 5.4%, well then that would be the highest rate since September 2015 – so, nearly 10 years.

For much of the time since it started to increase the Official Cash Rate in October 2021 the Reserve Bank has actually forecast that the peak in unemployment will be in this June quarter. So, it will be interesting to see if that’s how it turns out. Remember, the RBNZ took the OCR up to a cycle peak of 5.5% before starting to reduce it in August last year. It’s currently on 3.25%. If the labour market figures to be released this coming Wednesday are downbeat as expected, this will very much give a green light for another OCR cut at the next review on August 20.

The country witnessed a short, sharp and nasty recession last year, with GDP shrinking by 1.0% in both the June and September quarters. The hope was that once the RBNZ began lowering the OCR – effectively ‘taking the brakes of’ – this would see the economy start to recover.

Grinding to a halt

And arguably, as per the March quarter, that looked the case, albeit slowly. However, recent economic indicators are suggesting things may be seriously grinding to a halt again, and that is a worry.

We won’t see official June quarter GDP figures till September, but the early glimpses we’ve been getting of NZ Inc’s performance in that quarter are not good.

The BNZ-Business NZ Performance of Manufacturing (PMI) and Performance of Services (PSI) indexes are showing results that according to BNZ economists are “consistent with an economy in recession”.

Spending is still sluggish, while surging food prices are soaking up more cash than households would want.

So, what of the labour market? What indications do we have there?

Statistics NZ’s Monthly Employment Indicators (MEI) have shown continued reduction in jobs, while monthly job ads are falling again. The MEI figures are not directly comparable with the official unemployment figures as they are sourced quite differently – coming from Inland Revenue data – but they have tended to be quite a good indicator of future trends. And they are not indicating good things at the moment.

Source: 123rf.com

ANZ senior economist Miles Workman says there’s been some anecdote in recent months that firms holding on to labour are not experiencing the pickup in demand they expected.

“A degree of ‘labour hoarding’ appears to have suppressed unemployment in recent quarters, and if a recovery in economic momentum doesn’t do the heavy lifting when it comes to ‘right-sizing’ firms’ labour input, a further reduction in headcount may be needed,” Workman said.

“With the high- frequency data currently pointing to a generalised loss in economic momentum, risks around employment growth over the next few quarters are skewed to the downside.”

And as BNZ senior economist Doug Steel points out, none of this is supportive of household spending, “which remains critical to a broader economic recovery”.

“Weak employment is a headwind on its own but comes with a kicker of raising concerns around job security. Combined with above average inflation in some essential items like food and electricity, it is another factor threatening the timing and extent of the pickup in household spending that many are forecasting.”

One of the saving graces around this monetary policy tightening cycle was that we started it with incredibly low unemployment.

In March 2022 even while the RBNZ was starting to crank up the interest rates, our unemployment was just 3.2%.

The ‘lagging indicator’ that prompts a vicious cycle?

The key thing about that of course was that it gave everybody the best chance of being able to stump up the extra money needed as mortgage rates started going up. Losing your job right when the mortgage is starting to get more expensive is just exactly what you don’t want.

Unemployment is, as they say, a ‘lagging indicator’ – it tends to start rising as other parts of the economic cycle are starting to move into recovery.

And this is where I would be a bit concerned about our current situation.

After being as low as 3.2% the unemployment rate gradually rose to 4.0% by the end of 2023 and then 5.1% by the end of 2024 – the level it was still at as of the March quarter.

With the economy appearing to have stalled in the June quarter and with unemployment appearing likely to have hit around 5.3%, it’s difficult to see where the incentives are for people to get out spending again. And of course if people don’t spend, businesses struggle to make money, and they have to reduce staff. The classic ‘vicious’ cycle.

Therefore, while a 5.3% unemployment figure may demonstrate the classing ‘lagging’ economic indicator factor, the impact of it, the optics of it, on a country short on confidence might be fairly unhelpful. It could get us into a more gloomy mood and actually make things worse.

We probably need something to break us out of the ‘cycle’. While an OCR cut next month is looking a near certainty, the odds of a follow-up cut as soon as October must be rising as well.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.