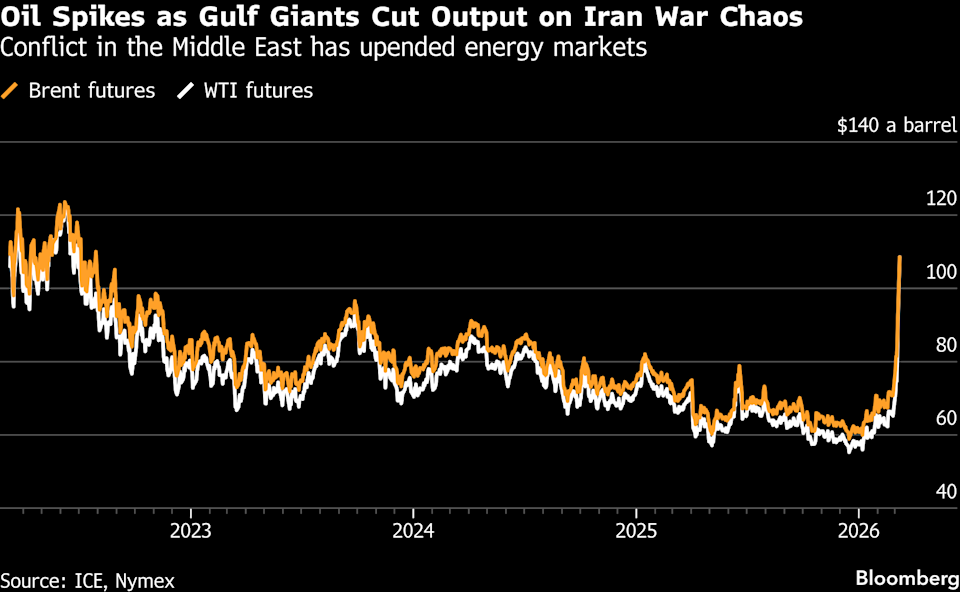

(Bloomberg) — Oil smashed through $100 a barrel as Saudi Arabia joined other major Middle East producers in cutting output, with a standstill of tanker traffic through the vital Strait of Hormuz choking off supplies to the rest of the world.

Brent traded 10% higher around $102 a barrel. Prices eased from almost $120 earlier as the world’s largest economies consider a co-ordinated release of emergency oil stockpiles, with Group of Seven finance ministers set to discuss the move on Monday.

Most Read from Bloomberg

Saudi Arabia is beginning to cut oil production as its storage tanks fill up, according to a person familiar with the situation, following similar moves in neighboring countries. The Kingdom has been diverting supplies via a pipeline to the western Red Sea port of Yanbu, but doesn’t have enough capacity to fully replace export volumes that typically transit through Hormuz.

The war in the Middle East is showing no signs of abating after US and Israeli strikes on Iran more than a week ago, and the fallout is stoking fears of an inflation crisis. The halt to shipping through Hormuz — a narrow waterway that normally handles a fifth of the world’s oil — along with attacks on key energy infrastructure have also driven up prices of natural gas and diesel.

Kuwait and the United Arab Emirates started reducing output over the weekend as storage rapidly fills up due to the closure of Hormuz. Iraq began shutting in production last week. At its peak, global benchmark Brent spiked as much as 29%.

US President Donald Trump weighed in on the oil spike with a late night post on Truth Social, saying that short-term movements are a “very small price to pay” for the US, the world, and peace. He added prices will fall rapidly “when the destruction of the Iran nuclear threat is over.”

French President Emmanuel Macron said a ship-escort mission in the Strait of Hormuz will be possible once the hottest phase of the war is over.

“The longer the Strait stays closed, the more production gets shut-in, requiring substantially higher prices to curb demand,” said Giovanni Staunovo, a commodity analyst at UBS Group AG.

More than a dozen countries have been sucked into the fray and Trump has signaled intentions to push on with the war. In a social media post early Saturday, he said the US will consider striking areas and groups of people in Iran that were not previously considered targets. The remarks came after Iranian President Masoud Pezeshkian vowed not to back down.

Story Continues

Iran named the son of the late Ayatollah Ali Khamenei as its new supreme leader, the semi-official Fars news agency said on Sunday, with the Islamic Revolutionary Guard Corps pledging obedience to the new leader. Meanwhile, the US State Department ordered American employees and diplomats in Saudi Arabia to leave the country, citing safety risks.

In a rare move, Saudi Aramco offered barrels for immediate delivery through a series of rare tenders for delivery, some of which were from a supertanker near Taiwan. The company typically only offers supply under long-term contracts. It’s one of many signs that producers are taking unusual steps to keep the oil market supplied.

One oil tanker also appears to have transited the Strait of Hormuz with its satellite signal switched off in recent days. It’s among the first major vessels to cross, though the overwhelming majority of shipowners remain reluctant to do so.

Middle East oil production shut-ins could expand to over 4 million barrels a day by the end of next week as storage fills and bottlenecks persist, JPMorgan Chase & Co. analysts including Natasha Kaneva wrote in a note dated March 8. The region accounts for roughly one-third of global output.

“Right now, the biggest fear is still disruption to flows through Hormuz,” said Haris Khurshid, chief investment officer at Karobaar Capital LP in Chicago. “Production shut ins matter but the market really worries about barrels not being able to move.”

WATCH: Saudi Arabia has started reducing oil production, following similar moves by the UAE, Kuwait and Iraq. Joumanna Bercetche reports.Source: Bloomberg

WATCH: Saudi Arabia has started reducing oil production, following similar moves by the UAE, Kuwait and Iraq. Joumanna Bercetche reports.Source: Bloomberg

Rising energy prices, including for products such as diesel, are rippling through the market. Europe’s benchmark gasoil futures were trading north of $170 a barrel on Monday.

China’s government has told the country’s top refiners to suspend exports of diesel and gasoline, and South Korea is reviewing whether to introduce an oil price cap for the first time in 30 years. India said it won’t be releasing emergency reserves and that the country has no plan to lift gasoline and diesel prices as of now. Nigeria’s giant dangote refinery is going to prioritize supplying fuel to domestic markets.

US retail gasoline prices have jumped to the highest level since August 2024, posing a significant challenge to Trump and his party at midterm elections later this year. UK Prime Minister Keir Starmer has raised the prospect of intervening to help households with soaring energy bills.

In a sign of near-term tightness, Brent’s prompt spread — the difference between its two nearest contracts earlier hit as much as $9.82 a barrel. That gap is usually just a few cents and on Monday was the highest in data since 2013.

–With assistance from Nathan Risser.

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.