The Reserve Bank (RBNZ) is widely expected to deliver on another ‘almost-promise’ and lower the Official Cash Rate (OCR) again in the coming week.

At its last OCR review on July 9 the RBNZ took a pause from from six consecutive cuts since August 2024 that had taken the cash rate down from the cycle peak of 5.5% to the current 3.25%. However, the accompanying statement from the RBNZ’s Monetary Policy Committee (MPC) made clear this was just a pause and not a stop.

The statement said this:

If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further.

In the raised eyebrow world of nuanced RBNZ-speak, the above phrase pretty much says: ‘Next up comes another cut, if we don’t get a nasty surprise in the meantime.’

So, here we go. That next review is upon us and on Wednesday, August 20 we get to find out if the OCR will be dropped from the current 3.25% to 3.00%.

Very probably it will be. The markets will be surprised if it is not, which could send wholesale interest rates and the Kiwi dollar haywire. And it’s unlikely the RBNZ will be wanting to create such ructions at the moment with our economy so delicately placed.

Aside from the very obvious focus on whether there will be a rate cut, the coming week’s review will be of great interest because this one (as happens every second review) will be accompanied by a new Monetary Policy Statement (MPS) – the first since May. And it will contain all the commentary, charts and graphs and – vitally – new sets of forecasts.

As ever, the main magnetic feature in this MPS will be the RBNZ’s new forecasts for the likely future level of the OCR.

The devilishly difficult detail

I’ve not really gone into detail explaining these forecasts before, so, this time I will have a go. They are not as straight forward as you might imagine.

Because the forecasts are based on quarterly averages and the figures produced don’t adhere to the reality that the RBNZ moves in 25-point lumps, these forecasts always leave a certain amount open to interpretation. That’s why you can see different economists and indeed writers each putting a slightly different slant on where the OCR may end up. It’s not just that some of us can’t read figures.

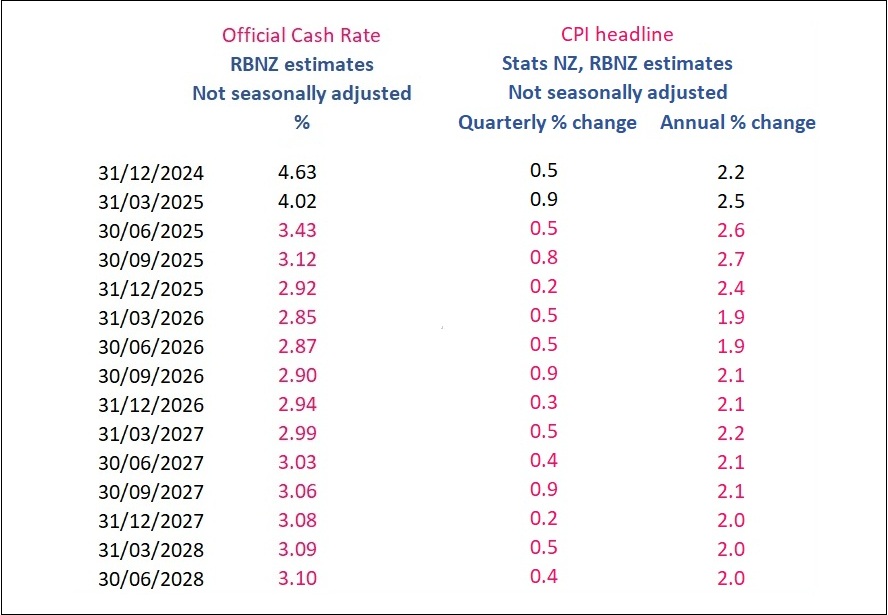

I include here the last forecasts for the OCR and the Consumers Price Index (CPI) headline inflation figures – both quarterly and annual. These figures are taken from the spreadsheet supplied by the RBNZ as part of the background material for the MPS, rather than from the MPS document itself, because these figures are not rounded and that actually makes quite a difference to how the OCR projection can be interpreted. Figures that are a projection appear in pink.

What we can see is that as per the May MPS the RBNZ was projecting a quarterly low point for the OCR of 2.85% in March 2026. Now, the OCR won’t go to 2.85%. It will either be 3.00% or 2.75%. Since 2.85% is closer to 2.75% than 3.00% the RBNZ is ascribing a bigger possibility (a 60% chance) of the OCR ending up at 2.75% than 3.00%.

So, the big question on August 20, once we’ve found out whether the OCR has actually been cut or not, is whether the odds have changed of a further cut or cuts. And also whether the timing has changed – particularly whether any cuts might be sooner than was earlier forecast.

What might we expect in the new forecasts?

Well, the expectation will be for a lower ‘terminal’ OCR figure and yes, probably also for the timing of this to be brought forward. The markets will be surprised if the RBNZ doesn’t forecast a lower OCR this time around.

But the RBNZ will also be conscious of not letting the markets run away with things. At time of writing (and this changes daily) the wholesale interest rate markets were pricing a low point for the OCR of 2.72% in May of next year.

If therefore the RBNZ were to, for example, show a low point in its new projections of 2.70% by the end of this year, the markets would start seeing it as a near certainty that there would be another OCR cut in October (to 2.75%). The markets would likely respond to this by then assessing a greater chance of a further cut or cuts beyond that one and therefore repricing the OCR down again to closer to 2.50% or maybe even below that. That means lower wholesale rates and these lower rates may then feed into further mortgage reductions.

So, the RBNZ effectively has to decide whether it’s comfortable with the idea of the markets pricing in future OCR cuts or whether it wants leave its options totally open.

Source: 123rf.com

But maybe we are putting the cart before the horse. Why in any case should we be talking about more cuts in future?

Okay, well, there’s the two conflicting forces at play at the moment. There’s inflation on the one hand and then on the other there’s an economy that’s supposed to be recovering, but appears to have not yet taken that message on board.

Priority number one for the RBNZ will always be inflation. It is charged with achieving inflation within 1% and 3% and specifically it targets 2%.

Inflation has started moving up again. The RBNZ forecast (as you can see at right on the table above) that the annual rate would move up to 2.6% in the June quarter from 2.5%.

However, after making those forecasts the RBNZ was the recipient of a lot more high frequency data that suggested inflation really was on the move. And it said this on the subject in its July OCR review:

Annual consumers price inflation will likely increase towards the top of the Monetary Policy Committee’s 1 to 3 percent target band over mid-2025. However, with spare productive capacity in the economy and declining domestic inflation pressures, headline inflation is expected to remain in the band and return to around 2 percent by early 2026.

Now, the message I take from that is that the RBNZ was pretty much conceding its 2.6% inflation pick for the June quarter was a bust and it was expecting a figure maybe significantly higher (say 2.8% or 2.9%).

However, when the June quarter figures duly appeared on July 21 they were softer than virtually everybody expected. And the 2.7% rate was not so far from what the RBNZ had picked back in May.

Yes, the inflation figure probably will go higher. There’s more mileage seen yet in the spike in food prices for example. But the RBNZ doesn’t look likely to be surprised from here by any developments on the inflation front. And it expects the spike will be short-run, and it expects the impact of tariffs to be ultimately deflationary.

Conflicting forces at work

Okay, so, if we decide inflation won’t be too much of an ongoing problem, does that just mean the OCR should just be left where it is?

Well, that’s where the other ‘conflicting’ force comes in. The economy appears to have had another setback in the June quarter (we won’t see GDP figures for the quarter till next month). And we, the public, do appear to be quite grumpy. And this is not conducive to us all rushing out and spending up large and boosting the economy.

Apart from the June quarter inflation figures, the other major data release since the last OCR decision on July 9 was the unemployment figures out on August 6, which showed the unemployment rate in the June quarter rising to 5.2% from 5.1%. That was bang on the RBNZ’s forecast, lower than the market expected, but with underlying details that really weren’t wonderful. The participation rate dropped, for example, effectively meaning some people had given up on getting a job. Once people count themselves out of the workforce in this way they count themselves out of the unemployment figure – so, the figure doesn’t go as high as it might otherwise. That 5.2% figure was in reality worse than it looked.

It’s said often enough that unemployment is a ‘lagging’ indicator and it tends to be rising at the tail end of an economic cycle, when things are already starting to look up in the economy at large. But there’s no doubt at the moment in the middle of winter, when people have been dealing with interest rates higher than they want, when food prices keep going up, when house prices apparently don’t, well, unemployment’s just another thing to get grumpy about. And to worry about. We are down.

I won’t go into huge detail about what all the recent high frequency lower-level economic data has been saying, although the ANZ economists have done a nice job of wrapping up much of it in their OCR preview. So, have a look at that.

But in essence, the high frequency data’s telling us that both manufacturing and the service sector (the latter making up about two-thirds of GDP) have been contracting, retail spending’s struggling, house prices are flat or even falling a little, and so on.

Source: 123rf.com

On the face of it, everything says cut interest rates further. But if it was that simple…

If we assume the RBNZ does cut the OCR to 3.00% in the coming week, it will mean the cash rate has been reduced by 250 basis points since the start of the cuts in August 2024 (when the OCR was on 5.5%). That’s a lot. But the impact of the reductions is not immediate. It takes time for example for people to roll over on to lower mortgage rates. So, they don’t feel the OCR cuts straight away.

The question for the RBNZ then is to what extent are the cuts already made ‘working’ and to what extent is the impact of those still to be felt? Clearly, if we are to believe that what we are seeing in the economy at the moment is ‘as good as it gets’ after 250 basis points of cuts, then more reductions are warranted. But the RBNZ has to make the call of how much impact is still to be felt.

Sure to rise – the overcooked hiking cycle

I thought the RBNZ ‘overcooked it’ when rates were on their way up to 5.5%, simply because it was hard to work out in real time whether the hikes in rates were actually working as intended. The worry is that everything kind of catches up at once. I think that happened on the way up.

And it could happen on the way down. So, if the RBNZ does just bite the bullet and take the OCR below 2.5% as some would argue it should, well, does that then cause the economy to overheat again? Look, we appear to be a heck of a long way away from such a situation at the moment. A heck of a long way. But we’ve had the boom and bust thing before, particularly when it comes to our housing market.

So, it will be no surprise if the RBNZ remains cautious. The best guess then is that, yes, there will be a cut in the coming week, and the RBNZ will leave the door open for the possibility of at least another cut. But it will keep its options open.

We’ll have to wait and see if the ‘June swoon’ we’ve just had proves to be the bottom of the cycle…or whether our economy has just hit the bottom and will continue to bump along the bottom till it gets more OCR help.

I guess as long as the RBNZ takes each OCR as it comes things aren’t too complicated. The decision in the coming week is straight forward. Deciding what should be done at the following OCR review in October looks devilishly complicated. But maybe by the time we get there the options will be pretty clear too.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.