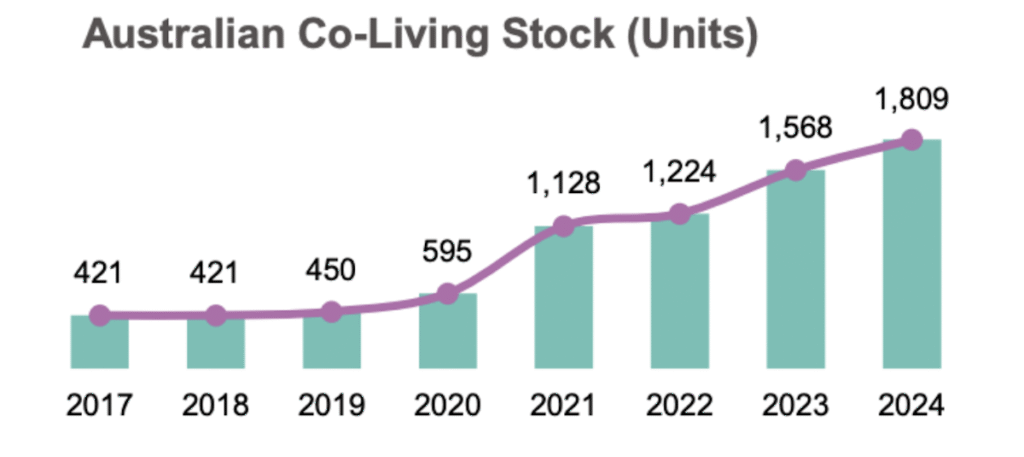

Urbis has released its Living Sector’s Market Insights, highlighting that the supply of co-living units in Australia continues to grow, with over 1,800 co-living units delivered to date. Most of the current supply stock of co-living units are in Sydney (around 70%), followed by the balance of the total in Melbourne.

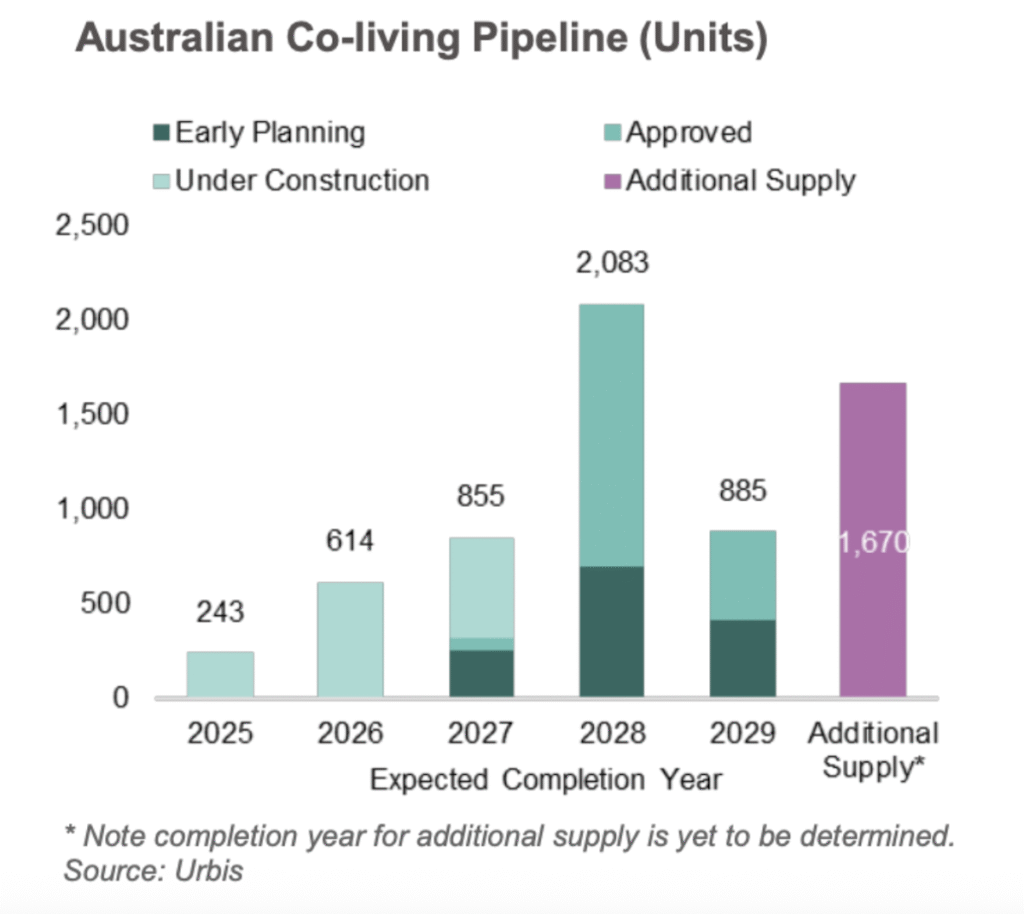

Around 1,386 co-living units are currently under construction and expected to deliver an average of 460 additional units over the next three years to 2027. The future pipeline also contains another 4,960 in early planning or with development approval.

Urbis believes that the delivery of the full pipeline of these schemes would more than triple the existing market, however, even this represents a ‘drop in the ocean’ compared to the future growth in single households – highlighting the potential of co-living in the Australian market to help ease demand pressures and provide innovative living solutions in our cities.

Compared to the international market, there are 9,000 operational co-living beds in the UK, many delivered in Greater London. Over 9,000 beds have been submitted for planning, largely in response to formal recognition of co-living in UK planning frameworks.

The sector is institutionalising, with growing investor confidence, regulatory

support, and an emerging set of standards. The model is increasingly seen as a viable sub-sector within the broader build-to-rent and urban housing ecosystem.

In the US, 74,000 co-living beds are active across major cities, typically located in New York, Los Angeles and San Francisco. The pipeline is growing steadily, but fragmented, led by private-sector initiatives.