September is a bit of an in-between month for the housing market, where it’s starting to emerge from the winter gloom but hasn’t yet built up a head of steam to charge into summer.

That makes it difficult to pick how the market might track over the usual early summer rush, before it goes into hibernation for the Christmas/new year break.

Looking at the big picture stuff, two things that usually have a major impact on the housing market are interest rates, which affect demand, and the amount of stock for sale, which affects supply.

Mortgage interest rates have been declining since August last year, with the average two year fixed rate dropping to 4.6% in September this year from 6.0% in September last year.

Such a decline would normally trigger a surge in sales and selling prices but so far, that hasn’t happened.

The Real Estate Institute of New Zealand reported 6346 residential sales in September this year, up just 3.1% compared to September last year. Meanwhile REINZ’s median selling price was 1.5% lower in September this year than it was in September last year.

Basically, median houses prices have bounced around from month to month within the $750,000 to $800,000 band since the end of 2022, suggesting prices have been more or less flat for nearly three years.

One of the main reasons for the flat prices has been an oversupply of stock on the market, which has given buyers the upper hand in price negotiations.

Anecdotal evidence suggests the main reason for this is the number of vendors with unrealistically high price expectations.

With so many properties to choose from, those that are selling are the ones that are priced to market.

Those that are overpriced are left languishing, a bit like a cat that wants to catch birds but can’t be bothered chasing them, so it sits in the sun with it’s mouth open hoping a bird will fly into it.

At the end of September this year, property sales website Realestate.co.nz had 30,721 residential properties for sale, up 2.3% compared to September last year, but up 30.3% from September 2023.

So for the time being at least, buyers still have plenty to choose from.

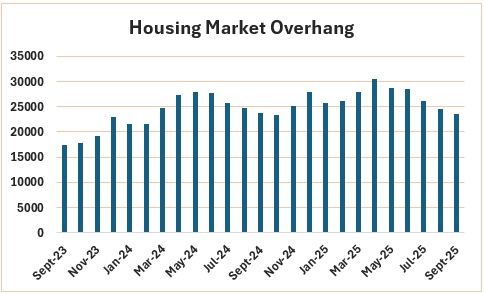

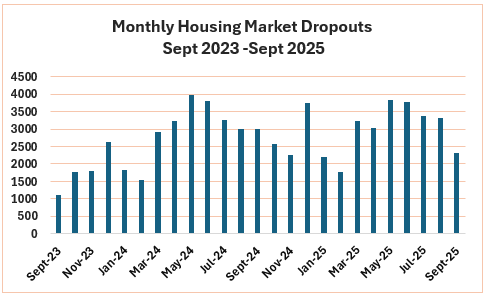

There are two other indicators interest.co.nz watches closely to get a hint of where the market is headed – the overhang and the dropouts.

The overhang is the number of properties that are left unsold at the end of their marketing campaigns each month, while the dropouts are the properties that have either been withdrawn from sale completely or are still listed for sale but are no longer being actively marketed.

Both sets of figures have steadily declined over the last four to five months, but both also follow a seasonal path. See the graphs below for the trends.

So far, the numbers suggest the overhang at the end of September this year was about the same as it was a year earlier, while dropouts have tended to be running at a higher level than 12 months ago with a sharpish drop in September.

Unfortunately all of that data doesn’t really point to any major movements in the market one way or the other, apart from the usual seasonal variations.

So if you were going to have a punt on where the market is headed over summer, it might pay to have a bob each way.

Hopefully, October’s figures will be more revealing.