Clark Johnson, financial advisor and partner at Oak Crest Wealth Management (Steve Lewis)

Ask Clark Johnson how the One Big Beautiful Bill Act will affect taxation and wealth management, and he’ll stop you short.

“It’s just a loaded question,” the North Little Rock financial adviser told Arkansas Business this month. “There are so many things in this bill, hence the name big. So I’ll have to share just some of the biggest impacts.”

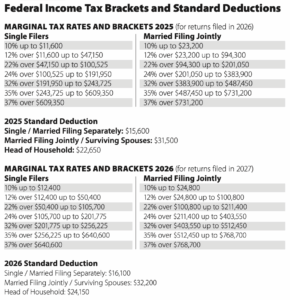

For one thing, the thousand-page OBBBA extends current tax breaks and brackets for individuals. Those were laid out in the 2017 Tax Cuts and Jobs Act during the first Trump administration, and had been set to rise to previous rates at the end of this year. For example, the top marginal tax rate for single filers will remain at 37% rather than reverting to the pre-2017 rate of 39.6%.

Little Rock financial adviser and analyst Larry Watts called eliminating the “2026 cliff” the biggest relief in the July 4 OBBBA. “The 2017 reductions in taxes had been set to expire in 2026, and that is no longer the case. So people don’t have to worry so much about it.”

The standard deduction raised in 2017 will also escape the cliff.

It went up from $12,700 to $24,000 for joint filers in 2017 and will increase to $31,500 for the current tax year and $32,200 for 2026.

“Many of the people I’ve talked to had forgotten that the standard deduction had doubled,” Johnson said. “They just look at me like, ‘Oh yeah, I did itemize once upon a time.’”

The OBBBA also spares the lifetime gift and estate tax exemption from being cut in half. Instead of falling to $7 million, in fact, it will increase in 2026 to $15 million — nearly $30 million for couples — with yearly inflation adjustments. That provision, as well as a quadrupled deduction for state and local taxes paid, could pay major dividends for higher-wealth taxpayers who plan well, Johnson said.

“If your net worth is of a certain size, you get hit with an estate tax, or death tax, as they call it,” Johnson said. “It starts out around 40%.”

From the passage of the American Taxpayer Relief Act of 2012 to the TCJA of 2017, the inflation-adjusted exemption ranged from $5.12 million to $5.45 million per individual. For this tax year, it will be $13.6 million per individual and $27 million per couple before rising further next year.

Estate planning has always involved various strategies beyond trusts alone. While revocable living trusts are valuable for avoiding probate and managing assets during life, they don’t reduce estate taxes.

Historically, high-net-worth people used lifetime gifting strategies and specialized irrevocable trusts to minimize estate taxes. The higher exclusion under OBBBA means more families can transfer wealth without triggering estate taxes, though trusts remain important for asset protection, probate avoidance, and other non-tax reasons.

Watts, a Stephens Inc. veteran and owner of Watts Wealth Management, noted that even with a $30 million estate tax exemption a couple with assets of, say, $50 million, would face paying a substantial tax on the remaining $20 million in the estate. “That would incentivize you to gift some of that now, rather than the heirs being hit with the estate tax and the income tax.”

The OBBBA maintains the annual gift exclusion at $19,000 per person, per recipient. This means an individual can give $19,000 to any number of people each year without triggering gift-tax reporting rules.

The law also allows a generation-skipping wealth transfer of $15 million. The GST exclusion involves, for example, a grandparent giving assets to a grandchild.

Watts said taxpayers may not be aware of changes involving the cost basis applied on inherited assets.

“If someone owns Walmart stock and it was worth 10 bucks and now it’s worth 100, the inheritor doesn’t have to pay anything for the capital increase in the value of that stock,” Watts said. “The step-up in basis rule remains unchanged under OBBBA, which continues to reduce the tax impact and eases the pressure to gift those assets during life.”

The OBBBA makes state and local tax payments a bigger consideration for taxpayers who itemize deductions. Lawmakers made the SALT deduction a priority to relieve tax burdens on homeowners in high property-tax states, but that relief, without further legislation, will end Jan. 1, 2030.

Larry Watts (Photo provided)

Larry Watts (Photo provided)

Until then, the deduction will go from $10,000 to $40,000 per year. Other phaseouts depend on income and tax filing status, so financial professionals urge clients to come in and discuss their situations.

“In 2028 through 2030 there will be new expiration dates for certain benefits,” Watts said. “That provides incentives for people to do their estate planning now and take advantages that are available for a few years.”

The SALT deduction and a new $6,000-per-year deduction for taxpayers above 65 offer prime examples, he said. “Seniors should capitalize on that deduction through 2028,” Watts said. “And for the SALT deduction strategy, taxpayers should consult with their tax advisers about prepayment options, since deductibility generally requires that taxes be assessed for the year in which they’re paid. Simply prepaying multiple years may not provide the intended deduction.”

“I’ll use a real example. I have a house and a condo. My home and my condo combined are about $9,000 a year in property taxes. With proper planning and timing of property tax payments, along with other state and local taxes like income taxes, I can maximize the benefit of the higher $40,000 SALT cap before it reverts back to $10,000. It’s something you don’t want to leave on the table.”

Johnson said the new deduction for seniors could be “huge” for retirees.

“I think that’s a really big deal because at least a third of American retirees have Social Security as their only source of income,” he said.

Johnson urged people who inherit nonspousal IRAs to learn about the OBBBA’s implications.

“It used to be where you can continue taking out the required minimum distribution or RMD over your lifetime,” he said. Now the heir gets just 10 years to withdraw the entire balance and should minimize the income tax impact, Johnson said.

“You’ve inherited mom or dad’s IRA, and you’ve been told that you can sandbag taking this money out until you’re in a lower bracket once you’ve retired.

“Well, they come in and say you actually have to take out a little bit every year. It’s not being talked about.”