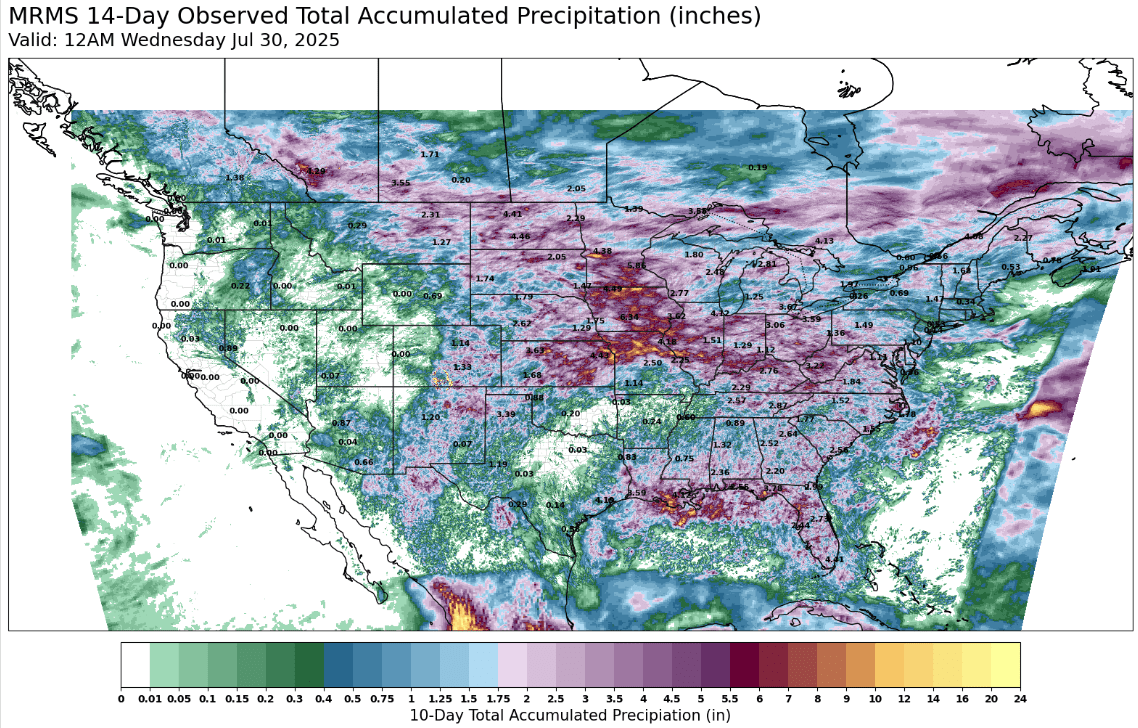

Weather: Adverse weather is impacting harvest logistics in multiple key regions, with heavy rainfall delaying Ukrainian grain flows and storms sweeping parts of the US Midwest. Meanwhile, July rainfall across Canadian canola regions is keeping crops in the game for now but more is needed.

Markets: Grain markets were mixed overnight. Soybeans were hammered as weak export sales and lack of Chinese interest. Wheat slipped again on strong global supply and sluggish demand. Corn managed modest gains, riding strength in crude oil. Canola held its ground, supported by tight old crop stocks and patchy Prairie weather, though broader oilseed sentiment remained soft.

Australian Day Ahead: The Aussie dollar getting smashed overnight should help local commodities hold their ground or firm slightly, despite wheat and canola easing and corn posting modest gains offshore

Offshore

Offshore

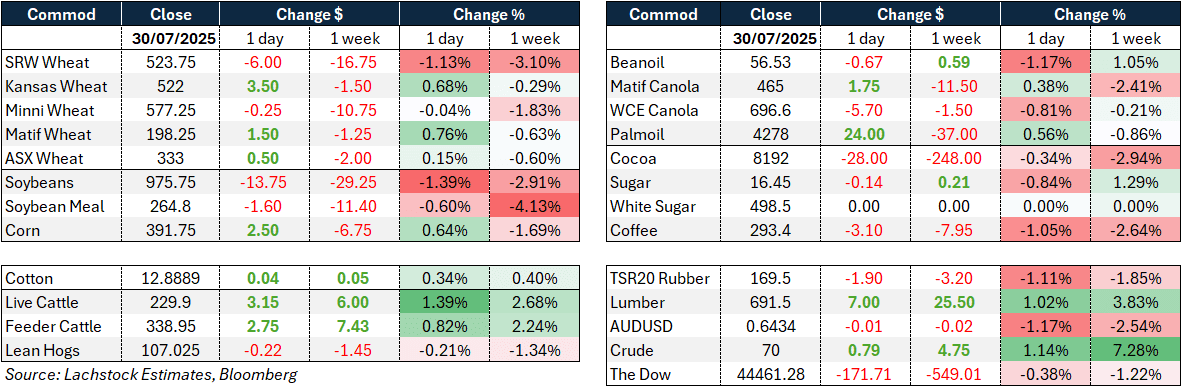

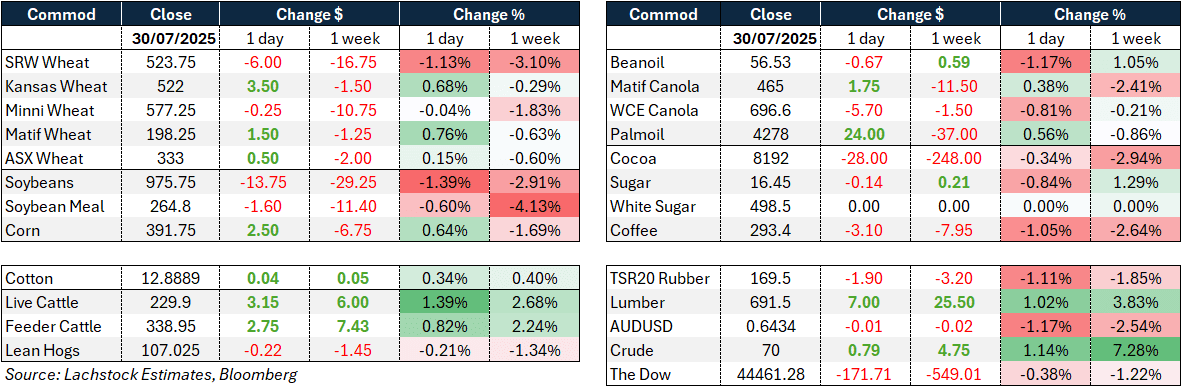

Wheat

CBOT Sep wheat slipped 1.1% to $5.24/bu, still under pressure despite a steady stream of global demand interest, including reports of Bangladesh buying US wheat under a government-to-government deal.

Kansas wheat led overnight, bucking the broader trend with a 3.5c gain, as HRW demand speculation and Baltic premium strength lifted sentiment.

SovEcon raised its 2025/26 Russian wheat export forecast by 400kt to 43.3 million tonnes (Mt) on improved crop prospects and currency weakness — adding fresh headwinds for global values.

Ukraine’s harvest is lagging, with just 2.2m ha of wheat harvested at a low 3.25t/ha yield; the Ag Ministry still calls production 21.2Mt, but trade estimates remain closer to 18.1Mt.

EU/BSEA weather and logistics continue to create headaches, and US wheat is winning demand it wasn’t expected to compete for, especially with HRW finding surprise traction.

Export sales today are expected at 500kt but could surprise to the upside, with the US only needing 315kt weekly to meet USDA targets.

Other grains and oilseeds

Corn firmed slightly overnight, with Dec up 0.4% to $4.12¾/bu, supported by crude oil strength and whispers of late-season export interest extending beyond October.

The bounce comes after a three-day slide, with analysts now watching for export sales today expected at 1.6mmt total (500k old + 1.1mmt new crop).

Soybeans were the weakest link, with Nov closing below $10 for the first time since April — down 1.3% to $9.96/bu — as questions around demand and China trade hang heavy.

Soymeal dropped to its lowest level since April 2016 amid swelling global supply, despite steady feed demand from hog and poultry sectors.

ICE canola is holding a sideways range into marketing year-end, supported by tight old crop carryout and Prairie weather variability. China’s resumption of Australian canola buying raises competition concerns, but overall S&D remains tight.

Export volumes this week are expected to rise for all three crops, with soybeans forecast as high as 900kmt — but traders need to see confirmation to break the bearish technical tone.

Macro

The Fed held rates steady, but two dissenters voted for a cut — the first time since 1993 — as Chair Powell struck a mildly hawkish tone during his press conference.

US GDP beat expectations, growing 3.0% annualised in Q2, driven by net exports and steady personal consumption — bolstering confidence in the economy’s resilience.

Trump confirmed a 25% tariff “plus penalties” on Indian imports starting Friday, citing longstanding trade imbalances. The deadline will not be extended.

China–US talks ended without a deal or truce extension, meaning tariffs will revert to April levels unless Trump approves a new plan before the August 12 deadline.

Commodities were mixed: copper plunged after Trump exempted refined metal from tariffs, crude rose to its highest since June on India-Russia tensions, and palm oil climbed on strong Dalian oils and a weaker ringgit.

The AUD/USD tumbled to the low 0.64s as the USD surged post-FOMC. Local data (Q2 retail, building approvals, trade indexes) due today may offer some direction, but broader risk remains USD-driven.

Australia

In the west of the country, wheat was slightly softer with new crop APW bid at A$360, barley was firm at $331, and canola held its ground at $865, with GM at $775.

Through the east of the country, new crop bids were slightly softer for wheat at $351 track and canola at $828, while barley held firm at $315.

The Aussie dollar got hosed last night on the back of US dollar strength and rates on hold — might make for a good day to get some new crop pulse sales on.

In South Australia, Thomas Foods International has cut processing capacity at its Lobethal plant, citing drought and a sharp decline in sheep numbers. The company expects livestock supply won’t recover until at least 2027, despite recent rainfall, highlighting ongoing structural tightness in availability.

New crop delivered barley markets are currently trading at an inverse to old crop, with NC Geelong/Melbourne bid at $330 and OC at $350.