The phrase “capacity constraints” has been thrown around quite a bit of late.

It doesn’t conjure up much for the imagination other than, perhaps, someone blowing up a balloon or maybe bloating after a large meal.

Despite its lack of clarity, the phrase is central to the language key economic policymakers are using.

A statement from the Reserve Bank (RBA) board used the phrase “capacity pressures”, but it’s essentially the same thing.

RBA lifts interest rates by 0.25pc

“The board has been closely monitoring the economy and judges that some of the increase in inflation reflects greater capacity pressures,” the RBA Monetary Policy Board said on February 3.

The crucial point to make up-front is that capacity constraints are inextricably linked to inflation, and therefore pain in your hip pocket.

Too much money, too few goods and services

When 100 people enter a supermarket, there needs to be goods to cater for those 100 people.

For those goods to appear, you need machines and people power to put them on the shelves.

If not, more people and machines need to be employed or rolled out.

“Capacity” refers to the extent that under-utilised labour and capital can be used to produce additional goods and services to meet higher demand.

Some “spare” capacity can be beneficial in fighting inflation because as demand rises, more goods and services are produced to meet that demand, and prices don’t rise.

If there is no spare capacity, too much money is chasing too few goods, and prices rise, producing inflation.

Measuring spare capacity

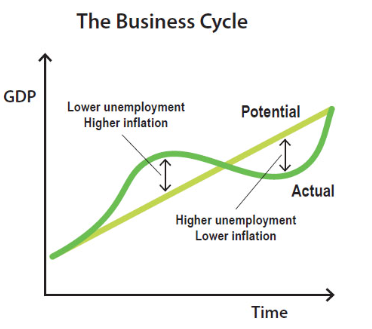

Economist Saul Eslake says, in theory, “the most comprehensive measure of ‘spare capacity’ is the ‘output gap’, that is the difference between actual GDP and ‘potential’ GDP, where ‘potential GDP’ is the level of GDP that would be produced if the economy were operating at ‘sustainable full employment.'”

Saul Eslake says a reserve army of workers is crucial in meeting demand for skilled labour as it is needed. (ABC News: Ebony ten Broeke)

Simply put, how much is the economy producing now, and how much does it need to produce to satisfy everybody’s needs?

It’d be great, wouldn’t it, if there were precisely the right number of workers in the economy with the ability to produce enough goods and services for the needs and wants of the population.

Economists say this is the economy in “equilibrium”.

Australia’s unemployment rate holds steady at 4.3 per cent

Eslake says a reserve army of workers is crucial in meeting demand for skilled labour as it’s needed.

“More recently, attention has been paid to broader measures of ‘under-utilisation’ of the labour force, eg people who are working part-time [and hence, not counted as ‘unemployed’] but would work more hours if they were offered,” he says.

“And it could be extended further to include people who are neither working nor ‘actively looking for work’ for any number of reasons, but who would look for and take up work if they thought they had a reasonable chance of finding it.”

Economy under strain

As it stands, Australia’s economic engine just can’t go any faster without overheating.

In any given sector, there is not enough skilled labour or the right kind of technology or machinery to produce what the nation needs without business costs rising significantly to meet that demand.

It’s suffering from capacity constraints.

There’s a valve to release the pressure though — goods and services providers hiking prices.

It makes sense — to reduce the surge of people coming into a shop that cannot cater for their needs, the shopkeeper hikes prices and, in the process, many leave, unable to afford what they want.

Labour’s weighing on costs

But there’s another element to this.

Goods and service providers can also make more stuff to cater for the demand.

If they do this without changing anything, it costs them a great deal extra — more staff, another machine.

Australian Chamber of Commerce and Industry (ACCI) chief executive Andrew McKellar says right now, many extra workers are being employed, but they are not working with more equipment.

Andrew McKellar says businesses are passing on higher costs to consumers. (ABC News: Matt Roberts)

It’s inefficient, he says, and businesses are being forced to pass on the extra costs of this in the form of higher prices.

“The one I would highlight as the most pressing relates to our capital intensity, reflecting a structural decline in our capital-to-labour ratio, or capital shallowing,” he says.

“In practice, this phenomenon can be gauged by comparing trends in business investment with total hours worked [utilisation of labour].

“This is at the heart of our sluggish productivity performance.”Workers need better gear

The bottom line, McKellar says, is that workers have their sleeves rolled up ready to go, but businesses have not met this with whiz-bang technology and machines.

“Of course, there are other examples of capacity constraints in access to skilled labour, innovation and take-up of technology, and the impact of excessive regulation and red-tape compliance, but this is the one I would highlight,” he says.

If workers had the best machinery to work with, businesses could pump out more at little extra cost.

And, indeed, the extra cost would be more than made up by higher profits as supply met demand.

“From a business point of view, we would prioritise reforms, which encourage stronger business investment, and which would lead to capital deepening,” McKellar said.

Or as Australian Industry Group CEO Innes Willox put it: “Anything that suppresses business efficiency — skills shortages, supply chain disruptions, inflexible workplace arrangements, or onerous regulation — contributes to capacity constraints.”

Productivity key to capacity

The key, therefore, to increasing the economy’s capacity is to boost productivity.

“That puts the focus squarely back on regulation and productivity,” Willox said.

“Why can’t Australian businesses currently supply the demands of 2 per cent economic growth, a rate which would have been considered modest only a few years ago?”

The federal government has established the Productivity Commission, led by Danielle Wood, to, at a basic level, resolve the nation’s productivity challenge.

Danielle Wood has been tasked with boosting productivity. (ABC News: Ian Cutmore)

And there appears to be some progress on that front.

The National Australia Bank’s latest business survey shows capacity constraints easing.

“[We saw a] second consecutive fall in capacity utilisation,” NAB senior economist Taylor Nugent told The Business.

“And that has been very elevated and indeed increasing through 2025.

“It’s still high,” he said.

Reserve Bank governor Michele Bullock expressed her confidence in the Productivity Commission’s work during the February interest rate decision press conference.

“Danielle Wood has plenty of good ideas about what we can be doing for productivity but it’s hard,” RBA governor Michele Bullock said at a press conference following the RBA’s February interest rate hike.

“A lot of people have a lot of hope in terms of AI, in terms of productivity, but we can’t do anything about productivity.

“The only point I’m making is that the economy can’t grow more quickly than the potential.”

What’s missing in this sentence, after the word potential, is “without inflation rising”.

The business cycle refers to fluctuations in economic growth relative to growth in potential output. (Supplied: Reserve Bank of Australia)

That is, if the Australian economy is to expand by greater than 2 percentage points per year, productivity needs to lift in order for the economy’s capacity to grow, without pressure on inflation.

“And if we think potential growth is around about 2 per cent, then the minute the private demand starts to pick up above that, then it potentially poses challenges for inflation because we’re constrained,” Bullock said.

This is why there is so much finger-pointing around the biggest contributor to “aggregate demand” or overall demand in the economy.

If it’s the public sector, the government can be blamed for rising inflation.

If it’s the private sector, it’s code blue for an emergency productivity response to prevent an inflation breakout and higher interest rates.

Treasurer Jim Chalmers noted yesterday during Question Time that increasing the economy’s “speed limit” was a priority for the government.

Put another way, increasing the economy’s ability to grow faster without pushing inflation higher.

There’s clearly work to do.

The National Australia Bank’s latest business survey shows that utilisation levels remain historically high due to tight labour markets.