Trevor Cox was driving his wife to hospital for an emergency shoulder replacement when a phone call changed everything.

Marie Cox had fallen on a nature strip and shattered her shoulder “like a Violet Crumble” days earlier.

On the phone was their private hospital, informing them their insurer, Bupa, would not cover the surgery the next day.

They would be out of pocket $30,000 and needed to pay $16,000 up-front.

The couple described it as “cruel”, having been with Bupa for 40 years, going back to its days as HBA.

“I still get upset. It’s not fair,” Mr Cox said.

Ms Cox was in intense pain, and the Bendigo couple felt their only option was the private system because of a shortage of shoulder specialists in their area.

The pair had to scramble, loaning money from friends and ultimately remortgaging their modest house to cover the medical bills.

“I’m just a little fish and they make so much money,” Ms Cox said.

“They had the ability to show compassion, but they didn’t.”

Marie Cox needed a complete shoulder replacement after tripping on a nature strip.(Supplied)

Marie Cox needed a complete shoulder replacement after tripping on a nature strip.(Supplied)

They are among the households questioning the value of private health insurance as the government grants the industry permission to raise premiums on average 4.41 per cent, the largest since 2017.

It follows a year of intense debate in the sector following high-profile fallouts between insurers and private hospitals, the collapse of Healthscope and the convening of a “CEO forum”, which meets regularly to try to iron out problems with the industry.

Growing discontent among patients and healthcare providers with insurers has prompted calls for price benchmarks for hospital services akin to the public sector, a mandatory code of conduct and an independent regulatory authority.

“This premium round has been guided by my commitment to maintain the value of private health insurance for Australians, while making sure the sector plays its part in supporting private hospitals facing rising costs and significant challenges,” Health Minister Mark Butler said in a statement.

Accident cover and joint replacement loopholes

When Ms Cox fell on the footpath, she also fell into a large industry crack relating to joint replacements following accidents.

The couple initially had gold-level cover, which included joint replacements, but when they went to change insurance providers in 2018, a Bupa employee convinced them to stay by downgrading to a cheaper silver plus policy.

Brett Heffernan from the Australian Private Hospitals Association said customers choosing to downgrade had become a regular occurrence during the cost-of-living crisis, but also suited insurers because silver policies were still lucrative, but with far more exclusions.

Brett Heffernan says more health insurance policies are coming with exclusions.(ABC News: Tobias Hunt)

Brett Heffernan says more health insurance policies are coming with exclusions.(ABC News: Tobias Hunt)

Some 360,000 people have downgraded their policies from gold since 2020.

“Increasingly we’re seeing the health insurers push people towards silver and bronze level,” he said.

“[Nearly] 70 per cent of Australians who have private hospital now have exclusions or restrictions built into their policies.”

Insurer industry body Private Healthcare Australia said the sharp price rise in gold polices was because they were now only taken out by those most likely to make a claim.

Insurance policies are priced based on a system of tiers, including basic, bronze, silver and gold, and the procedures covered in each group are mandated under legislation.

“There’s been huge inflation in the cost of gold hospital cover because it only covers bad risks,” PHA chief executive Rachel David said.

“Unless there is some intervention to tweak this system of gold, silver, bronze, basic, the gold product is not going to be sustainable for private health insurance and that is an issue.” Rachel David says patients should read policies carefully.(ABC News: John Gunn)

Rachel David says patients should read policies carefully.(ABC News: John Gunn)

Mr Cox said he was told that should the aging couple need elective hip or knee surgery later in life, they could simply upgrade closer to the date and serve out the waiting period.

But the devil was in the detail — the new silver policy also did not come with an add-on known as “accident inclusion”.

Accident inclusion insurance typically gives patients access to gold-level benefits, like joint replacements, in the case of an accident.

Health insurance consultant Ed Butler said it was an easy thing to miss because accident cover was not written on a Private Health Summary document — the list with ticks and crosses — where other clinical categories were covered.

“You would think it would say on those entitlements, ‘Not covered for trauma,'” Mr Cox said.

Trevor Cox helps his wife Marie with hairbrushing and other daily tasks after a shoulder replacement.(ABC News: Patrick Stone)

Trevor Cox helps his wife Marie with hairbrushing and other daily tasks after a shoulder replacement.(ABC News: Patrick Stone)

Mr Cox said he and his wife assumed all private health insurance included accident cover — but the ABC has found it varies widely from policy to policy.

It also varies between states because there can be overlap with state-based road accident and workplace insurance systems, which is designed to prevent double-dipping.

“If you’re not covered by accident, why do you bother having health insurance?” Mr Cox said.

“The word elective kept popping up and I kept saying, ‘This is not elective. I’m not choosing to have this done. This a traumatic injury,'” Ms Cox said.

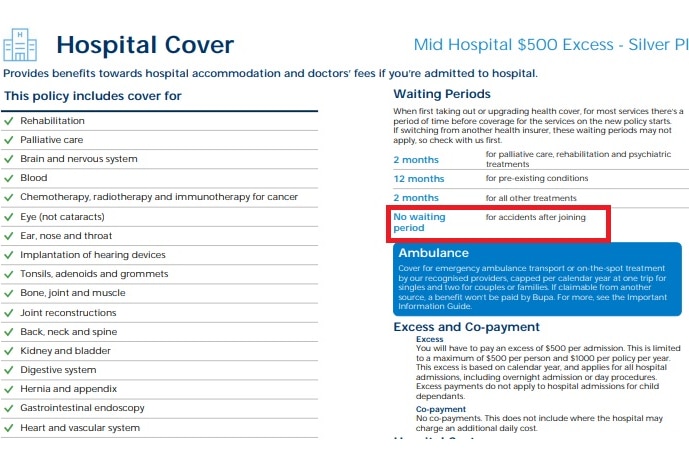

Marie Cox’s product disclosure summary mentions no waiting period for accidents but did not actually include accident cover.(Supplied)

Marie Cox’s product disclosure summary mentions no waiting period for accidents but did not actually include accident cover.(Supplied)

Adding confusion to the matter, the policy summary document does discuss waiting periods and said there was “no waiting period for accidents after joining”.

Surgeons seeing more patients with no cover

Joint replacement surgeries like Ms Cox’s are the backbone of the private hospital sector, with about three-quarters of all knee and hip replacements done in private hospitals.

They are often used to cross-subsidise more costly services covered by insurers, such as maternity and mental health.

Australian Society of Orthopaedic Surgeons chair Roger Brighton said stories like Ms Cox’s were becoming “infinitely more common” among his colleagues.

Roger Brighton says surgeons are finding more patients have private health exclusions.(ABC News: Dan Irvine)

Roger Brighton says surgeons are finding more patients have private health exclusions.(ABC News: Dan Irvine)

“Lots of people are getting a surprise. They find that they are not covered for that particular procedure and it comes as a shock to them,” he said.

The couple took their case to Bupa and the Commonwealth Ombudsman (which is also the Private Health Insurance Ombudsman) unsuccessfully, and said they felt let down by the system.

“I think they just put their hand in a barrel and say, ‘Oh, who are we gonna screw over today?'” Mr Cox said.

Dr David said it was up to consumers to be aware of policy exclusions and read their disclosure statements closely.

“There are probably ways in which the health funds can do better in explaining what accident cover actually entails, but any product that you buy that’s less than top hospital cover will have exclusions,” she said.

A Bupa spokesperson said they understood how stressful the situation was for the Cox family, but when they reviewed their policy, they were not covered for the surgery.

“We always encourage our customers to contact us at any time so we can step them through their cover and help them choose a policy that supports their current health and wellbeing needs,” the spokesperson said in a statement.

Exclusions catching many out

Patients around the country have written to the ABC with similar problems regarding joint replacements following accidents.

Orthopaedic surgeons provided us with other examples.

It has been a particularly confusing area for customers as, under law, gold cover must include joint replacements, but in some cases insurers choose to offer it in silver plus policies.

Making it even more opaque, some insurers only offer accident cover in their bronze and basic policies, not higher-tier silver or gold ones.

Disputed definitions Hip replacements are among the surgeries insurance customers are finding themselves not covered for.(ABC News)

Hip replacements are among the surgeries insurance customers are finding themselves not covered for.(ABC News)

A Bupa customer with silver cover was denied cover for a total hip replacement after it claimed their accident cover did not meet their definition of “trauma”. They eventually paid but made the patient pay $30,000 up-front.

Insurer battle House roof.(ABC News: Michael Lloyd)

House roof.(ABC News: Michael Lloyd)

An Adelaide man who needed an elbow replacement after falling off a roof had to get a loan of $20,000 from his in-laws after finding his silver policy did not cover the surgery. After a protracted battle with the insurer, he was repaid.

Downgraded cover Commonwealth Ombudsman logo(ABC News: Supplied)

Commonwealth Ombudsman logo(ABC News: Supplied)

A Bupa customer was initially told she was covered for a joint replacement but downgraded from gold to silver plus to keep her premium the same. When she was downgraded, she was not informed joint replacements would be excluded. She complained to the ombudsman.

Delayed decision After total knee replacement(Krossbow Flickr 2.0 Generic CC BY 2,0)

After total knee replacement(Krossbow Flickr 2.0 Generic CC BY 2,0)

A WA man stepped off a verandah, damaging his knee, and over time realised he needed a $5,000 knee replacement. Because he had decided to pursue surgery more than 90 days after the accident, he was not covered. He was later compensated with two years’ free premiums.

Public wait list Surgery.(Adobe Stock: anatolly_gleb)

Surgery.(Adobe Stock: anatolly_gleb)

A WA couple downgraded from gold to silver to avoid paying pregnancy costs but were not informed joint replacements were removed, and the wife spent six months waiting in the public system for surgery.

Cheaper policy A model of a hip ball and socket joint.(ABC News: Joel Wilson)

A model of a hip ball and socket joint.(ABC News: Joel Wilson)

A Melbourne man spent six months in pain after his insurer denied his claim for a joint replacement despite the item being included on cheaper policies. He took his case to the ombudsman and won.

Dr Brighton said the health sector had not kept pace with the rising costs of joint replacements, which were a people-intensive procedure, and insurers were trying to save money at every turn.

“The insurers, from an orthopaedic surgical viewpoint, they’re seeking to get more involved than what we do,” he said.

“They’re starting to introduce restrictions in our coverage. They won’t cover certain prostheses, they won’t cover certain increases in technology.”

But the industry has argued doctors have not been forced into these agreements with insurers or hospitals and patient choice remains.

Consumers Health Forum of Australia chief executive Elizabeth Deveny said the idea of joint replacements being compulsorily included in silver-tier insurance packages had been raised in the past, but there were fears it would raise premiums too much.

Elizabeth Deveny says private health customers should not need a lawyer to understand their policies.(ABC News: Richard Sydenham)”You shouldn’t need a lawyer to understand your insurance policy,” she said.

Elizabeth Deveny says private health customers should not need a lawyer to understand their policies.(ABC News: Richard Sydenham)”You shouldn’t need a lawyer to understand your insurance policy,” she said.

“If people keep falling through the same gaps, then these loopholes need to be closed, and they need to be closed before the premiums go up again.”

Private hospitals picking up the tab

Mr Heffernan from the Australian Private Hospitals Association said patients were right to question the value proposition of private health.

He said often, when insurers did not pay, it fell to patients or private hospitals to pick up the tab.

“That shortfall is a billion dollars a year for the last four years,” he said.

The association has called for a mandatory code of conduct, while others in the sector want a dedicated private health insurance commission or authority.

“The health insurers are making a motza. Yet they’re passing on very, very little to private hospitals,” Mr Heffernan said.Is private health insurance worth it?

Dr David said the industry was already highly regulated by APRA, the ombudsman, health departments and the ACCC, and there was no need for more.

“That would be a waste of money, and the current regulators are doing a more than thorough job,” she said.

Mr Cox said despite reforms over the years, private health insurance was simply too complicated for patients to make informed choices.

Ms Cox was first injured in 2022 and the couple are still dealing with lawyers trying to get some kind of compensation, and still repaying their mortgage.

“It’s always sort of skewed to benefit them and not us,” he said.Loading…