TKO Group Holdings (NYSE:TKO) announced multi billion dollar domestic media rights deals for UFC with Paramount and WWE with ESPN. The company expanded its partnerships portfolio and launched Zuffa Boxing as a new combat sports venture. TKO approved a $1b share repurchase plan and doubled its dividend, signaling a larger capital return program. A legal dispute has emerged involving Queensberry Promotions and Saudi backed Sela over the formation of Zuffa Boxing.

TKO Group Holdings, parent of UFC and WWE, sits at the crossroads of sports, media and live entertainment, where long term rights deals often shape business models for years. As leagues, streamers and traditional broadcasters compete for live content, locked in media rights can influence how investors think about revenue visibility and bargaining power with partners. For retail investors, this kind of news is less about short term excitement and more about how consistent content demand can support a recurring cash flow profile.

At the same time, the launch of Zuffa Boxing and the new legal dispute introduce fresh opportunities and risks that are likely to shape how the NYSE:TKO story evolves. Alongside a $1b buyback authorization and a higher dividend, this creates a cluster of decisions that could affect earnings mix, balance sheet use and the company’s overall risk reward trade off. The rest of this article breaks down these moving pieces so you can decide how they fit with your own view on the live sports entertainment space.

Stay updated on the most important news stories for TKO Group Holdings by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on TKO Group Holdings.

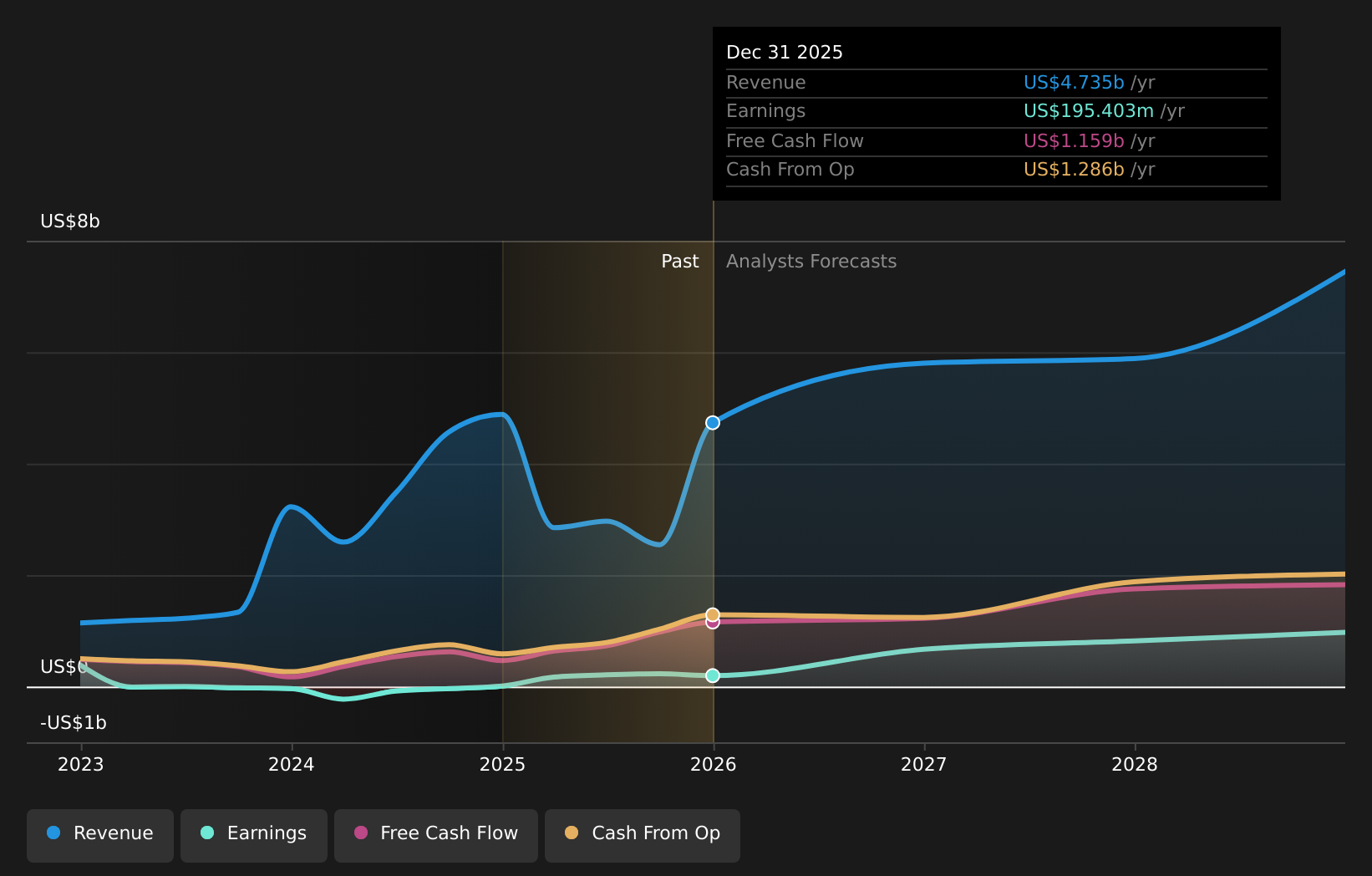

NYSE:TKO Earnings & Revenue Growth as at Mar 2026

NYSE:TKO Earnings & Revenue Growth as at Mar 2026

Quick Assessment ⚖️ Price vs Analyst Target: At US$223.87 versus a US$232.50 consensus target, TKO trades roughly 4% below where analysts sit, which is within the typical noise band. ❌ Simply Wall St Valuation: Shares are described as trading about 49% above estimated fair value, so the current price embeds a lot of optimism. ✅ Recent Momentum: A 30 day return of roughly 10.5% shows buyers have been willing to pay up following the rights deals and capital return news.

There is only one way to know the right time to buy, sell or hold TKO Group Holdings. Head to the Simply Wall St

company report for the latest analysis of TKO Group Holdings’s Fair Value.

Key Considerations 📊 Multi billion dollar UFC and WWE rights deals plus Zuffa Boxing mean more exposure to live combat sports content, which can influence how stable investors see future cash flows. 📊 With a P/E of about 89.3 versus an industry average of 37.0 and a forward P/E of 35.5, valuation multiples and execution on new ventures are key things to watch. ⚠️ The Zuffa Boxing legal dispute and a dividend that is flagged as not well covered by earnings both point to risk around how new projects and cash returns are managed. Dig Deeper

For the full picture including more risks and rewards, check out the

complete TKO Group Holdings analysis. Alternatively, you can visit the

community page for TKO Group Holdings to see how other investors believe this latest news will impact the company’s narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if TKO Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com