(Bloomberg) — The next four weeks will determine whether Europe’s economy is facing a fresh crisis or simply a speed bump in its recovery.

Most Read from Bloomberg

That’s how long Donald Trump says his strikes on Iran — which have already killed Ayatollah Ali Khamenei, triggered a wave of counter attacks across the Middle East and sent energy costs surging — will last.

A lengthier campaign risks sabotaging the euro zone’s fledgling revival while reawakening inflationary forces that the European Central Bank has fought hard to contain. A reliance on oil and gas from the region makes the bloc the “most exposed major economy” to Iran spillovers, ING’s Carsten Brzeski reckons.

“If the conflict is short-lived and energy prices rise only briefly, the damage will be contained,” Bloomberg Economics’s Antonio Barroso and Simona Delle Chiaie said. “A prolonged war, however, that keeps oil and gas prices elevated could force governments to spend more to shield voters from rising costs — and put incumbent leaders under pressure.”

Things had been looking up for Europe this year, with higher government spending in Germany and beyond set to underpin further modest economic expansion and inflation broadly in line with the ECB’s 2% goal.

But the Iran escalation follows renewed confusion over US tariffs after the Supreme Court struck down Trump’s initial levies.

There’s little panic just yet that the euro zone is being thrown off course. Holger Schmieding, chief economist at Berenberg, says he’ll continue to base his outlook on Brent prices averaging $65-$70 a barrel, even after they broke through $80 on Monday in what he described as probably a “near-term spike.”

“I’d expect Trump to go to great lengths to prevent a lasting surge in energy prices that could hurt him at home,” Schmieding said. “US voters already blamed him for high consumer prices before the strikes against Iran.”

Iran, too, has strong incentives to avoid excessive tensions in the Strait of Hormuz — the conduit for about a fifth of the world’s seaborne oil and gas.

“China – which, along with Russia, is the only major power supporting Iran – depends heavily on that sea route for its oil imports and will put pressure on Tehran not to jeopardize it,” UniCredit economist Edoardo Campanella said.

Story Continues

What Bloomberg Economics Says…

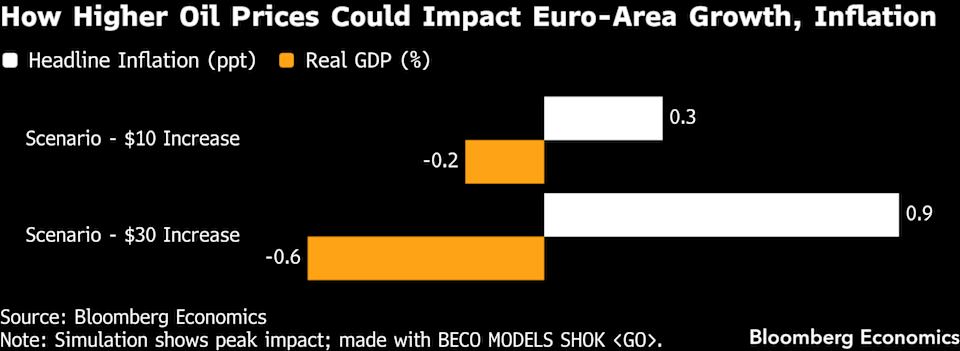

“The US-Israeli strike on Iran and Tehran’s retaliation have already sent oil toward $80 a barrel, from a pre-escalation average of $65. It could top $100 if supply through the Strait of Hormuz is shut off. European gas prices have also moved higher, with risks to the upside if the conflict intensifies. Running these scenarios through our in-house economic model shows that CPI will be up and GDP down across major advanced economies, triggering conflicting impulses for central banks.”

—Jamie Rush, Björn van Roye and Ziad Daoud. Click here for full INSIGHT

But while ECB policymakers Gabriel Makhlouf and Martin Kocher said it’s premature to pass judgment on what this weekend’s attacks mean for the economy, Belgium’s Pierre Wunsch laid out what a prolonged war could mean.

“I would certainly not rush to react to any movements to energy prices,” he said. But “if it lasts longer, if the increase in energy prices is higher, then we will have to run our models and see what happens.”

Despite the likely hit to Europe’s economy, the jump in commodity costs would still turn out to be net inflationary, Wunsch said. Indeed, traders now see a 25% chance that the ECB will hike rates by a quarter point this year.

Chief Economist Philip Lane said that the ECB “will be closely monitoring developments.” In an interview with the Financial Times he cited a prior scenario gamed out by central bank staff that showed “a substantial spike in energy-driven inflation and a sharp drop in output” caused by disruption to energy supplies stemming from a Middle East war.

France’s Francois Villeroy de Galhau called for cool heads.

“It would be a mistake to rush into predicting a possible change in interest rates today,” he said in Paris on Tuesday. “I would remind you that we will not be making our decision based solely on current energy prices.”

Policymakers will still have a close eye on European gas prices, which is up more than 60% since Friday’s close after Qatar halted production at the world’s largest export facility due to Iranian attacks.

The timing is particularly unfortunate for Europe, where inventories are already unusually low, meaning the region will need to import large volumes of LNG this summer to refill its tanks before next winter.

As a rule of thumb, a permanent shock to oil of $10 a barrel would lift euro-area inflation by 0.4 percentage points, Morgan Stanley estimates. Economic growth, meanwhile, would be 0.15 percentage points lower.

The ECB’s latest projections envisage consumer prices undershooting the target until 2028, with growth picking up to 1.4% next year from 1.2% in 2026.

For now, most don’t see the upswing in oil as a permanent adjustment.

“Investors are acting cautiously and are betting on a relatively short conflict,” said Tobias Basse of NordLB. He highlighted that Germany’s benchmark DAX index — currently at about 24,100 — “remains focused on the psychologically important 25,000-point mark.”

Investment manager BlackRock has a similar view.

“Markets and clients that we’re speaking with are looking at this as a volatility shock and not as a supply shock, and there’s an important distinction between the two,” Karim Chedid, head of EMEA investment strategy, told Bloomberg Television. “Largely speaking, it’s not this seismic shock to inflation.”

–With assistance from Craig Stirling, Alexander Weber, Mark Schroers, Francine Lacqua, Samy Adghirni and James Regan.

(Updates with Villeroy starting in 15th paragrapha)

Most Read from Bloomberg Businessweek

©2026 Bloomberg L.P.