Up the stairs and down the elevator.

For decades, that’s been the rule of thumb when it comes to financial markets — months or even years of slow, hard-fought gains interspersed with the occasional violent unravelling that would leave investors shell-shocked.

Almost every major market crash in the century preceding the global financial crisis stuck to the script.

Iran war live updates: For the latest news on the Middle East crisis read our blog.

The Great Depression followed the 1929 crash, the 1987 Black Monday collapse left stock markets in disarray for years, and the climb back from the GFC was slow and painful.

Not any longer.

Ever since the COVID-19 crash — which lasted barely three weeks before the recovery kicked into gear — investors have been willing to pile back into high-risk stocks with the kind of force that usually is reserved for a rush to the exits.

It was on full display last April when US President Donald Trump unleashed his Liberation Day tariffs on a disbelieving world and repeated this week after spiking oil prices rattled global investors, only to reverse course overnight.

The ‘quite terrifying’ scenarios that finally spooked global markets

The recovery rally and the plunge in oil prices this week were based purely on a vague, half-baked presidential promise that the joint US and Israeli attack on Iran was nearing conclusion.

“I think the war is very complete, pretty much,” the president told CBS News.

Brent crude, which had soared 25 per cent to $US117 a barrel on Monday, suddenly went into reverse, settling at under $US90 by Tuesday morning, as though nothing had happened.

And stocks? The Australian benchmark, which plunged as much as 4.2 per cent at one point on Monday morning, had mostly retraced its steps by the close of business Tuesday.

Overvalued and under threat

It’s rare for stock markets to deliver double-digit returns two years running. A three-year double-digit winning streak is almost unheard of.

Until Trump and Israel attacked Iran a fortnight ago, we were looking at clocking up yet another big win for the financial year. That would be four on the trot.

It’s not as though the rise, particularly in the past nine months, has been without worries.

Global stocks are at nose-bleed levels, and any number of investment gurus have been sweating bullets that it all could come tumbling down with just the slightest provocation.

In the early stages, it was driven by the fabulous growth of the Magnificent Seven technology stocks that bolted out of the blocks after the COVID lockdowns.

Penguin permacrisis as economic norms go in Trump’s shredder

When that theme looked to have run its course, the tantalising thought of a world based on artificial intelligence grabbed the imagination of investors keen to cash in on a bold new vision of the future.

Suddenly, however, that vision has been soured by the prospect that it won’t be ordinary workers losing their jobs and income. It’s likely to be highly paid lawyers, bankers, accountants and even tech executives.

The AI revolution even looks like demolishing or at least diminishing the magnificence of some of the Seven’s tech giants, especially those involved in software development, further undermining the shaky foundations of the technology boom.

Late last year, attention turned to everything left behind by the tech boom. Gold soared and metals and miners suddenly came back into vogue, symbolised by the ascension of BHP reasserting itself as the nation’s biggest company.

Cash even began flowing out of the US, with American investment houses shifting their focus to under-loved markets in Asia as they scoured the globe for bargains.

Global stock values kept marching higher, even as the nerves persisted.

The US and Israel’s war on Iran sparked a surge in oil prices. Pictured here is an oil depot in Tehran, burning after an air strike. (ISNA: Alireza Sotakbar)

Creating a crisis

Nik Burns describes it as “sleepwalking into a storm”.

In a note to clients last Friday, the energy analyst with investment bank Jarden questioned why investors were underestimating what he believed was the biggest energy crisis in 50 years.

Read more about the Iran war:

“While spot LNG and European gas prices have rocketed 47 to 55 per cent higher, the equities market remains surprisingly numb, seemingly underestimating the systemic risk to global energy stability, in our opinion,” Burns wrote.

“This is not just another geopolitical tremor: with traffic through the world’s most critical chokepoint dropping to near zero, we believe investors are misinterpreting what they see as a brief delay in supply as a non-event.”

He’s not alone.

Loading

MST oil analyst Saul Kavonic thinks investors have been numbed from years of warnings about a Middle East crisis that never eventuated.

“This existential Iran war is the energy crisis scenario that has been war-gamed for 50 years, finally coming to the fore,” he told ABC’s The Business.

Kavonic said that while it was premature to be panicking over oil, this episode was far more critical than during the Russian invasion, particularly in regard to LNG, because the volumes involved were far greater.

Loading…

What followed the two oil price shocks of the 1970s was years of stagflation, a portmanteau that combines the two most dreaded terms in the economics lingo: stagnation and inflation.

It’s every central banker’s worst nightmare. No matter what you do, it’s the wrong move.

Hike rates to kill inflation? You just drive the economy deeper into recession. Cut rates to kickstart the economy? You’ll entrench a regime of ever-increasing prices.

The weight of money steamrolls logic

One possible reason is money supply and the sheer volume of cash flooding the globe.

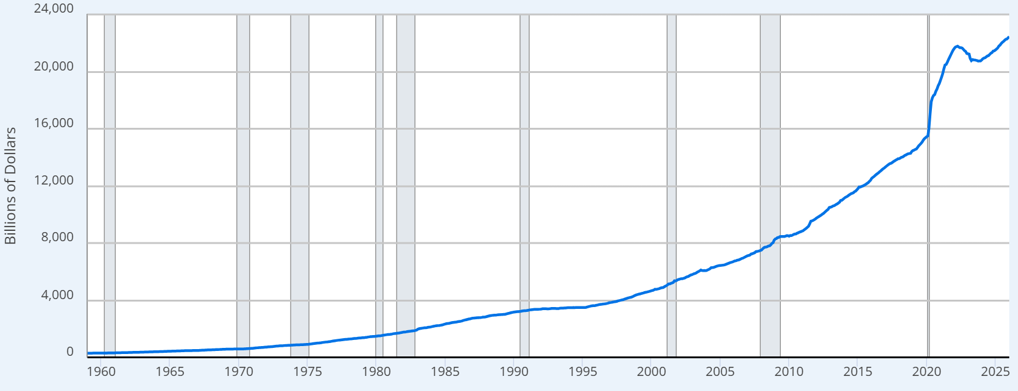

The incredible amount of stimulus provided during the GFC, which then was ramped up during the COVID lockdowns, is still washing through the system, as this graph of the US money supply shows.

Since the GFC 15 years ago the amount of cash in the US economy has trebled. (Federal Reserve Bank of St Louis)

All that cash needs to find a home and, across the developed world, it has poured into asset markets such as stocks and real estate.

Even the interest rate hikes of recent years failed to sate the appetite for property and stocks.

Investors now tend to treat any downturn as a buying opportunity rather than as a retreat to more sane levels, and quickly bid prices back to the levels at which they previously traded.

But the Iran crisis may test that.

Expert analysis on the Middle East:

If America doesn’t extricate itself from Iran within the next few weeks, the price of energy, and particularly gas, will soar.

Energy is used in every conceivable corner of the economy. Every product and service requires electricity or petrol to be built or delivered. Shortages will push prices higher, which will flow right through the economy.

That will push electricity prices higher and light a fire under inflation. For the one third of Australian households saddled with a mortgage, that again will plunge them into an era of declining living standards as inflation outpaces wages growth.

Loading…

But importantly, this will be inflation ignited by an energy shortage, not excess consumer demand. And that raises the dreaded scenario of stagflation because consumers will see their wallets sapped by price hikes and rate hikes.

Throw in a scenario where large swathes of the workforce are made redundant by artificial intelligence and the exuberance on global financial markets begins to look a little misguided.

Or maybe they’ll just ignore reality and keep heading further into the stratosphere and we’ll all live happily ever after.

Loading…