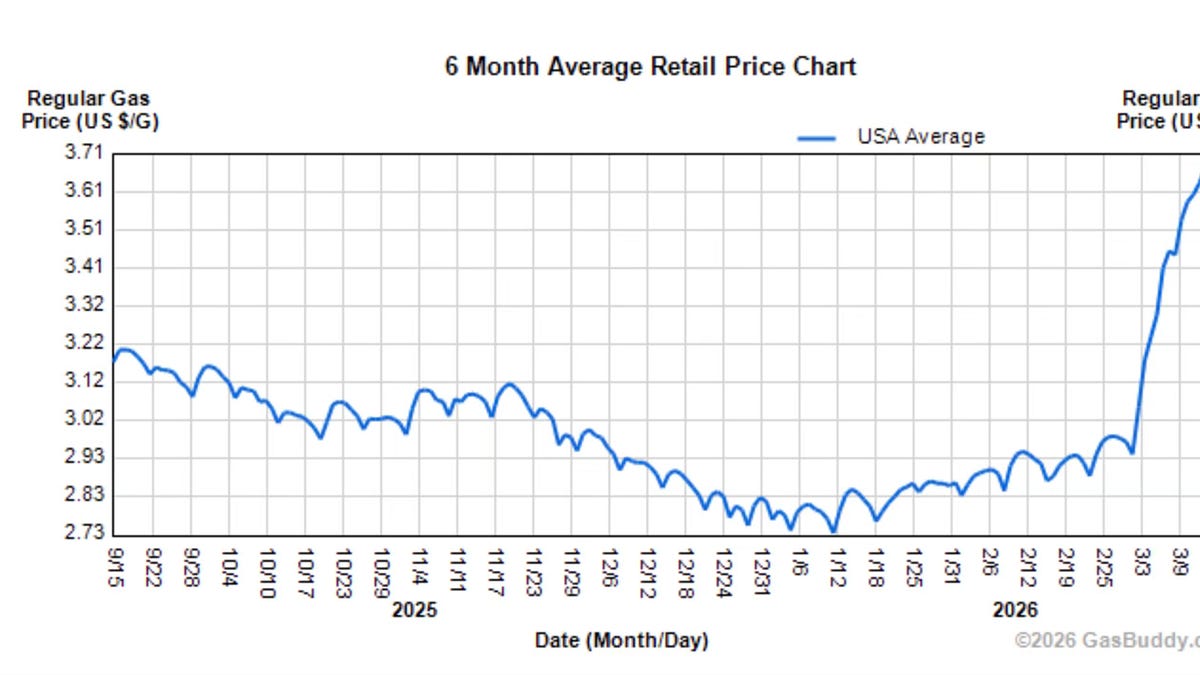

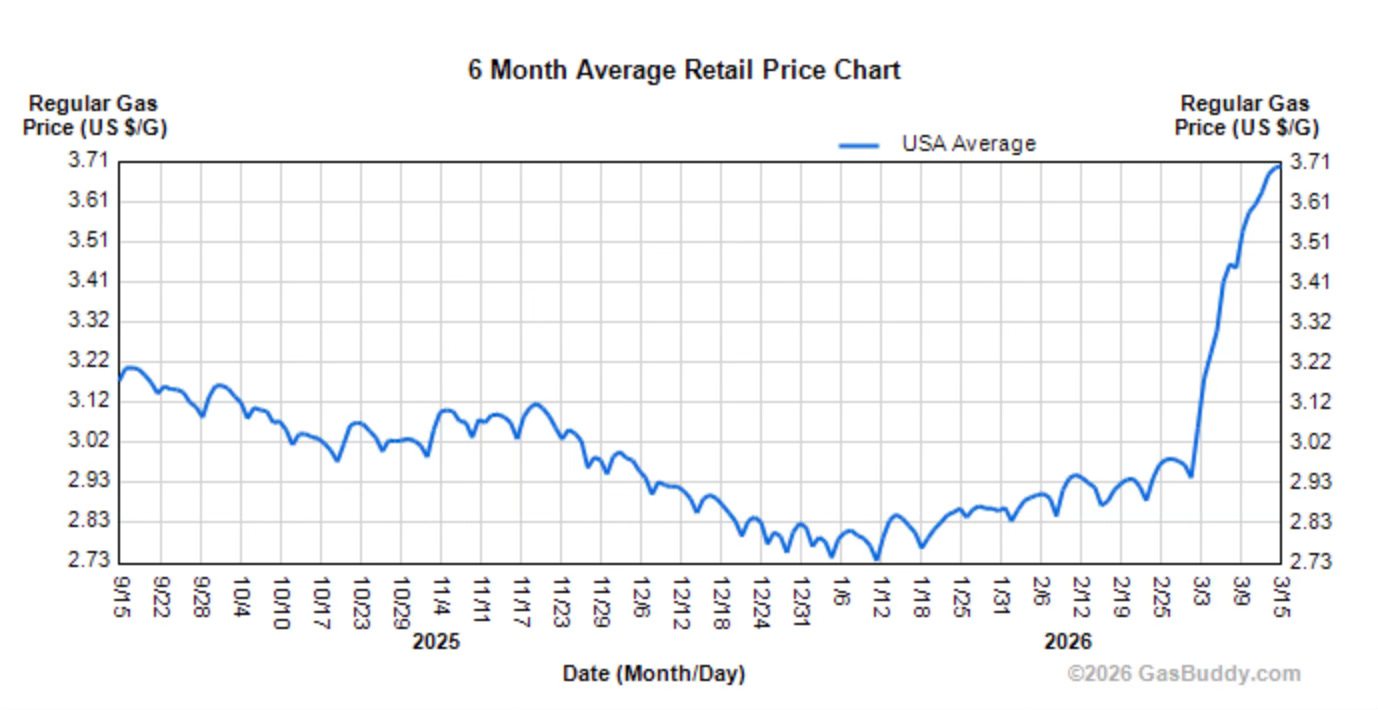

Operation Epic Fury, the U.S.-Israeli bombing campaign against Iran, began on Feb. 28. At first, the reaction of energy markets was muted. As the days passed, however, it became clear that the air strike that killed much of the Iranian regime’s top leadership had not broken that regime’s grip on power. It also became clear that despite heavy bombing the regime retained the ability to launch drones and missiles at energy facilities and shipping in the Persian Gulf. More than two weeks after the war began, the Strait of Hormuz, a crucial choke point for world energy supplies, remains effectively closed, and nobody knows when it will reopen.

Inevitably, given these events, the prices of oil, liquefied natural gas, and fertilizer produced from natural gas have soared.

I wrote about the possible economic consequences of such price shocks last week. It has become clear to me, however, that it would be useful to provide a sort of prequel to that discussion: a review of how global energy markets work, the factors determining energy prices, and the distribution of losses and gains — for there are some winners even from bad news — as oil prices soar.

Some of the winners are obvious: Russia and oil producers everywhere except in the Persian Gulf. The losers may come as a surprise: American consumers are being hit hard even though the US produces more oil and natural gas than it consumes, while China, despite its dependence on imported hydrocarbons, is relatively insulated from this shock.

Beyond the paywall I will address the following

1. Tankers, pipelines and the geography of energy

2. How high can energy prices go?

3. Why domestic oil production doesn’t protect consumers

4. The importance of oil intensity