Let the pain begin.

Andrew Hauser has left no-one in any doubt about the current thinking at the Reserve Bank of Australia (RBA).

In an uncharacteristically blunt assessment, a little over a week ago, the deputy RBA governor said unless action was taken, the Iran war and the sudden surge in energy prices could lead to “toxic inflation”.

As the board members gather for the second day of meetings this morning, they already would have been peppered with dire warnings about the potential impact of the energy shock.

There’s a smorgasbord of historical examples from which to choose.

Rising oil price and inflation fears make rate hike likely

With this episode shaping up as the worst in 50 years, the obvious exhibits would be the OPEC oil embargo of 1973 and the Iranian Revolution in 1979, both of which wreaked havoc on the developed world as oil prices headed to the heavens.

Anyone who lived through that period remembers. Sky-high inflation, massive unemployment, social upheaval and a global economy that, when it wasn’t in recession, struggled to gain any traction.

It triggered the collapse of the Bretton Woods monetary system and was accompanied by America’s humiliating defeat in Vietnam. The world’s biggest military force was ejected from Saigon by a small but far more determined group of homegrown warriors.

Four years ago, another military misadventure, Russian President Vladimir Putin’s ill-fated and supposedly week-long invasion of Ukraine, lit the fuse for what then appeared to be a re-run of the 1970s, delivering the first global inflationary surge in 50 years as energy prices soared.

As it turned out, it was merely a prelude for the main act.

This time, it is again America. And, once again, it is Iran that will be the stage for what increasingly is looking like a protracted battle with no winners.

Not so great expectations

You’ll hear the phrase ad nauseam this afternoon.

When RBA governor Michele Bullock takes the stage after the board raises the cash rate, prepare for an aural assault focusing on two words: expectations and anchored.

Until now, she will say, “inflation expectations” have been “anchored”. But in recent weeks, all that has changed.

Michele Bullock will speak after the Reserve Bank’s meeting today. (AAP: Dan Himbrechts)

Expectations from households and businesses have now become unanchored. (Normally, you’d use a word like unshackled just to mix it up a bit, but hey, this is the RBA).

So, what is it with the expectations and losing the pick (anchor)?

Isn’t the RBA all about being “data driven”, looking at the most recent statistics from the past to make decisions about the future?

Now, suddenly, it’s all about gazing into the crystal ball to figure out how Australians will react to an expected jump in the price of almost everything.

It’s not exactly new territory for central banks, or economists for that matter.

Essentially, it’s a behavioural science phenomenon. If we believe something is about to happen, and en masse, we all take the same course of action, what was an expectation can turn into reality.

It’s why everyone wore flares in the 1970s. And it explains quite a lot of economic trends. If everyone believes house prices will rise, they all jump in and outbid one another, forcing house prices higher.

Conversely, most stock market crashes often occur suddenly and violently as the fear of losses builds into a tsunami and everyone heads for the lifeboats simultaneously.

The belief, or the expectations, become self-fulfilling.

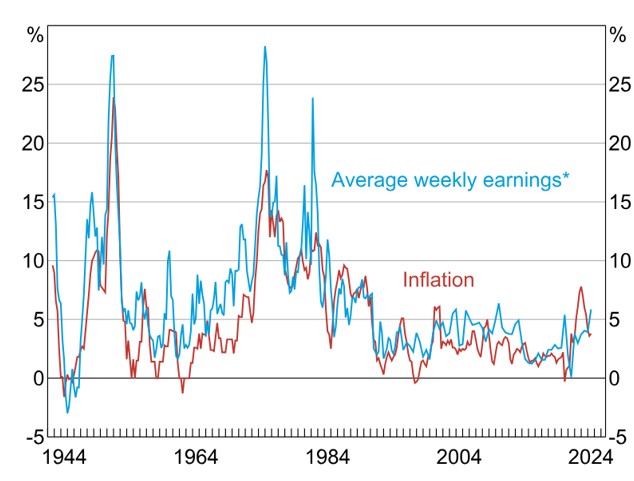

The wage price spiral that went walkabout

While it’s a fine theory, it has a couple of serious flaws, especially when it comes to inflation caused by supply shocks, which is exactly what we’re about to experience.

It assumes that workers will go on strike, demanding higher wages to cover the extra living costs, which then will force businesses to charge more to cover their costs, and on and on we go.

But just imagine for a second that you lived in a country that didn’t allow you to just charge more for your labour.

What if you lived in a country where you couldn’t take industrial action unless you first asked permission from the courts? Or, if your pay negotiations were limited to every three or so years when your agreement was up for renegotiation?

That sounds a lot like Australia.

Back in the 1970s, when the oil shocks sent seismic waves through the global economy, Australian workers held the whip hand during pay negotiations and there was industrial turmoil.

Strikes were rampant and businesses had little option but to cave when it came to pay demands.

That’s no longer the case.

During the first oil shock, inflation spiked at about 17 per cent and wages ran riot, shooting 27 per cent. During the second shock, the Iran Revolution, inflation touched 12 per cent as wages surged 24 per cent.

Australian workers demanded wage increases during the 1970s to cope with cost-of-living increases. (Source: RBA/ABS)

Compare that to the most recent oil price shock in 2022 when Russia invaded Ukraine.

During the Ukraine invasion, wage growth peaked at 4.3 per cent and never caught up with inflation, in stark contrast to the situation in the 1970s when wage growth far outstripped inflation.

Loading

Until 2024, workers suffered a huge erosion in living standards as our modern industrial relations system steamrolled the wages price spiral into a flatbread.

Still, economists cling to the anchor and the expectations theory.

Raising interest rates today won’t solve the energy crisis and it won’t push oil prices lower.

Running on empty — how we were caught short of oil

It will merely add to the pain inflicted on households by removing even more cash from their budgets.

It’s really the only weapon in the RBA arsenal, so it doesn’t have a great deal of choice.

Rate hikes are good at curbing runaway demand. But that’s not the problem here. Instead, the RBA will attempt to grind economic growth down to match up with constrained supply.

It is a brutal strategy that involves deliberately putting large numbers of Australians out of work.

If there’s one thing the RBA needs to realise, it is that while Australians’ inflation expectations may be unanchored, their ability to do anything about it remains firmly tethered.

Expectations, great or otherwise, don’t reflect actions.

Gas exporters to the rescue?

US President Donald Trump’s Iranian debacle hasn’t displeased everyone.

With oil and gas prices soaring, the stock prices of energy giants have been soaring in recent weeks.

Santos and Woodside have both jumped about 30 per cent since mid-January as they look to capitalise on the global shortages. While many of their export contracts are longer term, there is still ample scope to increase shipments of uncontracted gas into the global market.

Gas is a vital ingredient in our energy mix. Southern states like Victoria are heavily reliant upon it as a household fuel, and it has increasingly played a bigger role in electricity generation as coal-fired generators have retired.

Stock prices for gas giants Santos and Woodside have jumped about 30 per cent since mid-January. (ABC News: Pete Garnish)

It was the spike in gas prices from 2022 on that was a major contributor to soaring electricity bills. That, in turn, fuelled inflation and forced the RBA into one of the toughest rate hiking cycles in history.

The federal government responded with electricity rebates, which are still working their way through the system.

If there is a repeat in the wholesale gas market this time around, perhaps it would be a wiser option to charge a tax on any windfall profits, to ensure the gas exporters insulate domestic users from the worst of the crisis. Or, at least, pay for the support.

No-one has any idea how long the war will last, but the longer it goes on, the more dire the situation threatens to become.

America began this conflict in 1953 when the CIA toppled an elected Iranian prime minister in an orchestrated coup and then installed the Shah.

It wanted control of the country’s oil. They’re still fighting over it.