Pick a number, any number. But maybe something just a little way beyond the usual one to 10.

Trying to guess exactly where the oil price tops out is fast becoming the gamble du jour, the chocolate wheel of choice among politicians, economists and oil experts.

Iran war live updates: For the latest news on the Middle East conflict, read our blog.

If there’s any consolation, there appears to be an upper limit. The bad news, however, is that the price ceiling comes with a caveat.

It’s called demand destruction, the point at which people restrict their use of fuel either because they simply can no longer afford to buy it or because restrictions are placed upon its use.

That price is somewhere north of $US150 a barrel, possibly as high as $US180. Right now, stock and money markets are priced for a quick resolution to the war that involves a rapid return to oil shipments.

In a worst-case scenario, some pundits reckon we could see prices top out at $US200 if negotiations over ending the hostilities drag on.

According to Commonwealth Bank head of international economics Joe Capurso, even if the US withdraws, the conflict may continue and oil prices will remain elevated while more than 20 per cent of global production remains captive in the Persian Gulf.

“The war has three participants, and if the Iranians and the Israelis keep going, then the war will keep going,” he told The Business.

“What matters most for the world economy is the Strait of Hormuz and whether the oil and the gas are able to pass through it.”

The longer it remains shut, the greater the damage to Middle East oil fields, particularly in Saudi Arabia, and the more stretched supply chains become.

The conflict has affected the flow of oil to Australia. (AAP: Joel Carrett)

Muted reaction on financial markets

The International Energy Agency has described the crisis as the worst the world has faced.

But as the global economy continues to descend into chaos, financial markets have tapped a new-found well of euphoria, convinced that all will be resolved with minimal pain.

So far, oil prices have failed to breach the $US120 a barrel barrier, well short of the spike four years ago after the Russian invasion of Ukraine.

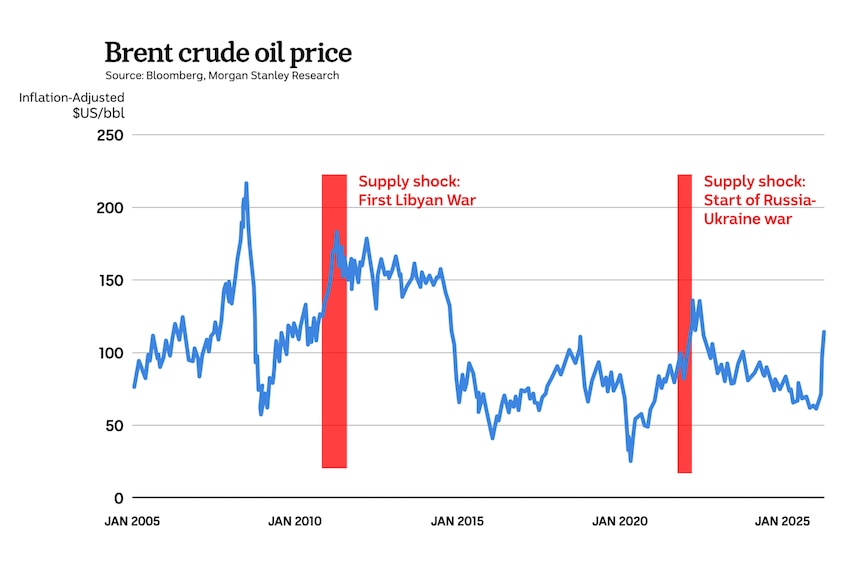

As the graph below shows, once inflation is taken into account, previous spikes during the past 20 years — including America’s war with Libya — ignited far more market panic.

(ABC Graphics)

Like the current situation, the Ukraine invasion and the Libya war involved supply shocks. But they were relatively insignificant when compared to a total shutdown of the Middle East.

Oil soared to about $US175 a barrel on an inflation-adjusted basis when the US overthrew Muammar Gaddafi, even though Libya produces less than 2 per cent of global oil output.

Oil prices have dropped significantly in the past week as Donald Trump has repeatedly indicated America is laying the groundwork for withdrawal, saying that Iran has requested a ceasefire and that the United States’s military objectives have been achieved.

The price of oil fell after Donald Trump’s comments on the Iran conflict.

(Reuters: Kevin Lamarque)

Who’s on top now?

For all Trump’s bravado, Iran’s iron-clad grip on the Strait of Hormuz remains intact, with it effectively holding 20 per cent of global oil and gas supplies hostage.

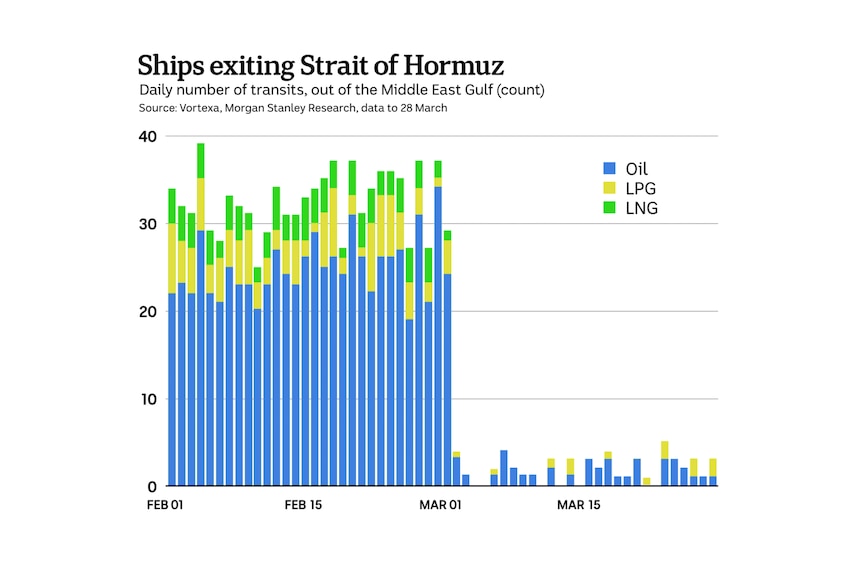

Since hostilities began at the beginning of March, traffic volumes through the strait have plunged and the only vessels transiting the choke point are those approved by Tehran.

(ABC Graphics)

As the graph above shows, a bare minimum of oil and liquid petroleum gas cargoes have run the gauntlet, mostly en route to China and a small number to India.

The flow of liquefied natural gas shipments has stopped altogether and since the Iranian attacks on Qatar’s massive processing and shipping facilities, Qatari leaders believe it could take years before the world’s second-largest LNG exporter returns to full capacity.

Supply chain backlash

It’s not just oil prices that are soaring.

As we learned in the aftermath of the COVID-19 pandemic, it took months for trading links and stretched supply chains to return to normal.

Those same effects are already playing out across the globe.

Loading

According to the United Nations, between 2,000 and 3,000 vessels are trapped in the Persian Gulf, an unprecedented event in the post-World War II era.

Among them are an estimated 350 oil and gas tankers.

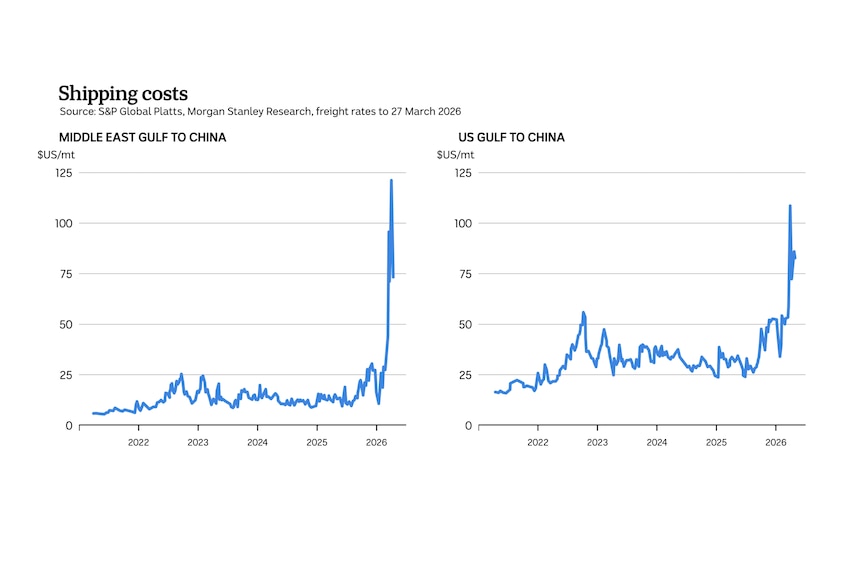

Unsurprisingly, with so many of the world’s largest energy transport vessels out of action, the cost of shipping oil and gas has gone into orbit.

(ABC Graphics)

Shipping oil from the Middle East to China is now four times more expensive than before Israel and America began pounding Iran.

And those price rises have been replicated around the globe. Shipping energy from anywhere is now hugely more expensive. Shipping energy from the Gulf of Mexico to China is now three times dearer than just a month ago, as this graph shows.

Then there’s refining.

With countries across the globe scrambling to shore up fuel supplies, refiners have found themselves in an unprecedented position of power.

This time last year, refiners were earning a $US20-a-barrel premium for refining a barrel of North Sea Brent oil into petrol and diesel. That’s now soared to $US60 a barrel.

Thousands of vessels are reportedly trapped in the Persian Gulf. (Supplied: Sentinel Hub)

When it comes to jet fuel, the situation is even worse, or better if you are in the refining business.

Aviation fuel now attracts a $US100-a-barrel premium over the cost of North Sea oil, a situation which, if it continues, will strain the finances of most of the world’s airlines and inevitably result in massive hikes in the cost of travel.

A possible way out

Global stock investors appear to be setting themselves up for disappointment.

According to Capurso, investors have taken a glass-half-full approach to the unfolding crisis, convinced that the situation will resolve itself if the US retreats.

“I think they’re going to be disappointed again, even if the president does announce that he is going to withdraw, at least in some way, from the war,” he told ABC’s The Business.

He reiterates that markets will be vulnerable to heavy falls for as long as the Strait of Hormuz is closed or even restricted.

That was on full display on Thursday after Trump’s disappointing national address, in which he failed to articulate any clear strategy to end the conflict.

Asian markets, which had opened in positive territory, turned south as oil prices strengthened.

But in the past week, an avenue for resolving the impasse has opened, with Tehran indicating that it wants to charge ships to pass through the Strait of Hormuz.

“Well, there certainly have been some reports of that and some, what Iran calls friendly nations, they’re allowing their ships to go through the straits,” he said.

“You could get a widening of what is defined as friendly.

“If it were to be all accepted to the US, then that would be a significant breakthrough in the oil market.”

Loading…