Gas exporters will be one of Australia’s only domestic industries to benefit from the global fuel crunch caused by the Middle East conflict, and all Australians should share in their windfall.

The crisis is a pivotal moment for the federal government as it weighs changes to Australia’s resources tax and royalty regimes, and the options available are wide-ranging and mostly positive. Ensuring Australians receive a fair return from the nation’s gas resources could help fund cost-relief and fuel-shift measures.

Rising LNG prices are likely to massively boost Australian LNG export earnings, as happened after Russia’s expanded invasion of Ukraine, when oil and gas sector profits increased from AU$13 billion in FY2020-21 to a staggering AU$62 billion in FY2022-23.

However, Australia’s taxation of LNG exports suggests that higher international prices will not fully translate into higher tax receipts. Oil and gas royalties as a share of export earnings were lower in that period when LNG prices peaked, than in years of more normal pricing.

Figure 1: Oil/gas and coal exports (AU$ billion, left) vs royalties as a share of revenue (right) vs royalties as a share of revenue (%, right)@2x (3) V5.jpeg)

Sources: Australian Energy Producers, Queensland Government, NSW Government and Australian Government

The fuel crisis highlights a glaring disparity between the royalties imposed on gas and coal exports. In contrast, coal royalties as a share of revenue doubled in FY2022-23 compared with FY2020-21 as prices rose and Queensland reformed its coal royalty regime. In total, coal royalties were four times higher than oil and gas royalties in times of elevated prices. The relatively low tax rate during a period of windfall profits partly reflects low payments under the Petroleum Resources Rent Tax (PRRT) framework.

For example, from FY2018-19 to FY2023-24, PRRT payments per gigajoule (GJ) of sale gas ranged from AU$0.21-0.41 per gigajoule (GJ), well below Queensland’s royalties of AU$0.19-1.57/GJ over the same period.

Queensland’s royalty revenues increased materially in years where LNG exporters earned windfall profits. IEEFA estimates that, in absolute terms, Queensland’s royalty revenue was higher than PRRT revenues when prices spiked in in FY2022-23 and FY2023-24. This is despite gas production in Commonwealth waters (i.e. subject to the PRRT) being three times higher than Queensland’s production in FY2022-23, and 2.75 times higher in FY2023-24.

Figure 2: Oil and gas sector royalty payments (left) and LNG prices (right), $/GJ and LNG prices (right), $_GJ@2x (4)_0.png)

Sources: Australian Energy Producers (AEP); Queensland Government; Australian Government; IEEFA.

As a profit-based tax, the PRRT allows LNG exporters to carry losses forward, which effectively minimises tax obligations in the early years of LNG projects, with payments increasing once exporters recover their costs.

While this framework is intended to incentivise investment, effectively it partly transfers construction risk to the Australian public, who have no ability to manage this risk. Most Australian LNG projects experienced construction delays and cost blowouts, which have delayed and decreased PRRT payments.

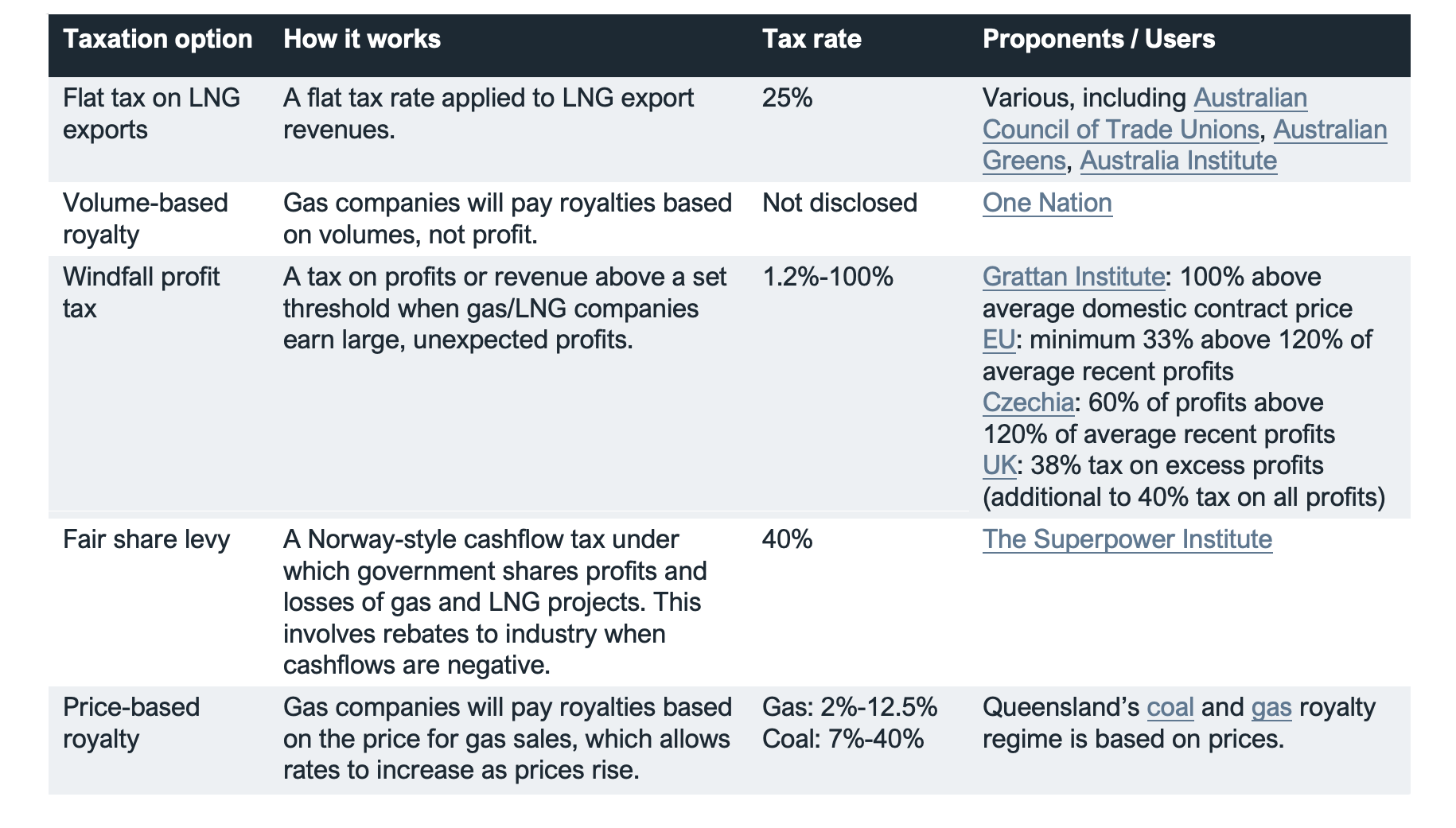

Several taxation frameworks have been proposed in the debate over Australia’s gas and LNG taxation settings, including a flat tax on LNG exports, windfall profit taxes, a fair share levy and price-based royalties.

Table 1: Gas and LNG taxation reform options

Following the start of the Ukraine war, several European countries implemented windfall taxes, while others benefited from existing taxation arrangements. The options listed in Table 1 would likely complement existing tax arrangements, particularly corporate and state-based taxes (such as payroll tax).

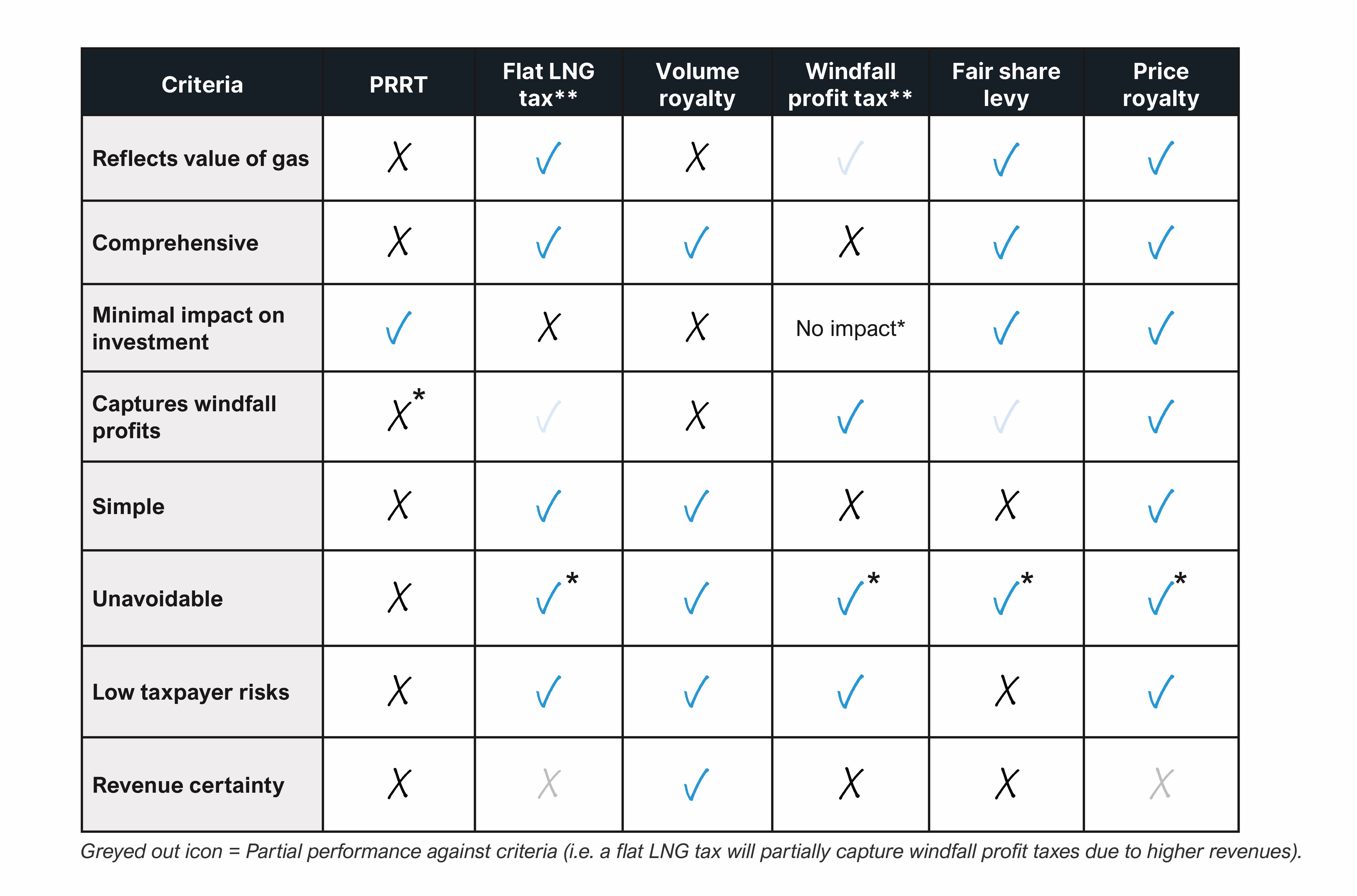

The note compares the PRRT with the proposed reforms across a range of criteria.

Table 2: Performance of possible taxation models under key criteria

Source: IEEFA. Notes: * Assumes risks of transfer pricing and profit shifting risks for multinational gas companies are addressed in the design of a new taxation regime. * Windfall profits may be captured, to an extent, if LNG projects have recovered previous costs and are eligible for PRRT obligations. No impact* Assumes access to debt financing is not affected, which may not be the case in practice if banks and financiers perceive there is a risk of governments not providing rebates during negative cash flow periods. ** Likely to create stronger incentives for domestic gas supply.

IEEFA’s assessment shows the many drawbacks of the PRRT regime, with multiple proposed options representing an improvement. Several models are promising, with a majority of positives against the selected criteria. In particular, the flat LNG tax and price-based royalty perform the best. However, we note that different criteria might support other options.

The conditions are right to reform royalties on Australian LNG exports. The current system does not appear to be working, and prices are expected to be elevated for an extended period.

With Australian LNG exporters set to earn windfall profits for the second time in five years, the broader public is increasingly questioning the value to them. Reforming taxation would allow some of these windfall benefits to flow to all Australians.