It is, by all accounts, the largest corporate transaction ever involving a single South African family, equal to an astounding 7% of the country’s GDP.

Yet Natie Kirsh’s sale of his US company, Jetro Restaurant Depot, for $29.1bn (about R500bn) does more than simply leapfrog him to the top of the list of South Africa’s billionaires. It bears remarkable testimony to the skills of local entrepreneurs on the global stage.

For older South Africans who woke up to a front-page article in The Wall Street Journal, detailing how a “reclusive 94-year-old” had sold his food empire to the US-listed wholesaler Sysco, this would have been no surprise.

Kirsh, an ace dealmaker, towered over South Africa’s business sector in the early 1980s, creating the country’s third-largest industrial group that owned many of the top consumer brands.

“He was a powerhouse in his prime in South Africa,” says David Shapiro, the veteran portfolio manager at Otto1890. “He faded from view when he went to America, but no-one understood how he’d built Jetro into this massive juggernaut. This is why the size of that deal would have been such a surprise.”

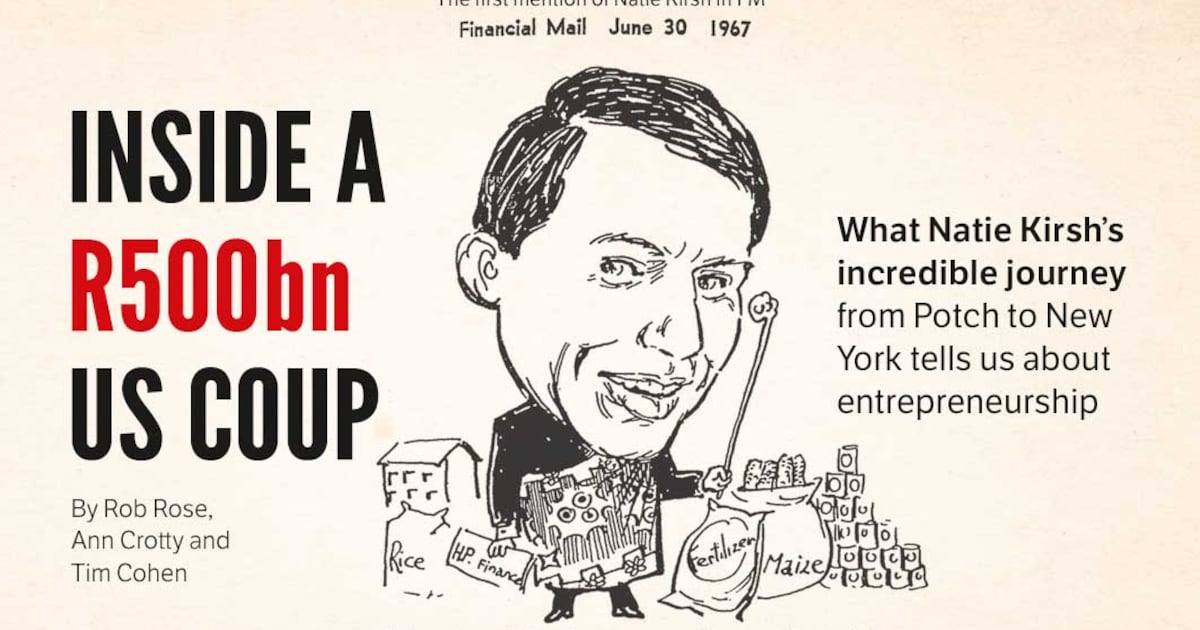

Potch-born dealmaker with an eye for detail (Robert Tshabalala)

Potch-born dealmaker with an eye for detail (Robert Tshabalala)

It’s a story that began in Potchefstroom in 1932, where Natie was born to Lithuanian immigrants who started a small malt business. But the game changed in 1958 when Natie used a £1,200 insurance payout from his father’s death and an equivalent amount from his brother Issy to buy mills in Swaziland — today Eswatini — with such success that he soon became the kingdom’s wealthiest citizen.

“Swaziland’s Paul Getty” was how the FM first introduced the lean, clean-cut Kirsh in 1967, comparing him to the flamboyant American oilman who, by that time, had been crowned the wealthiest person alive by Fortune.

But if Getty was a notorious playboy who loved the public eye, Kirsh was anything but. “He is so publicity shy, he won’t thank me for introducing him,” the FM writer said of the 35-year-old Kirsh in 1967, when he was interviewed puffing on an expensive cigar at the Swazi Spa.

“Only nine years ago [in 1958],” the FM report continued, “he was still in the family malt business at Potchefstroom, but then came the Swazi government call for someone to establish a local maize marketing set-up and, shrewdly aware of what it could lead to, Kirsh took his chance with both hands.”

He diversified his Swazi business into chemicals, farming and food wholesale. In 1970, the roots of his future trajectory were planted when he bought Moshal Gevisser, a JSE-listed retailer with a small cash-and-carry business in Newcastle.

At the time, white businesses weren’t allowed to operate in black townships, but Kirsh saw an opportunity to use Moshal to supply black businesses. This idea “transformed distribution in South Africa,” Kirsh later told the FM.

Doubling down on that vision, he merged Moshal Gevisser with another JSE-listed company, Metro Cash & Carry (Metcash). He would own 30% of the combined business. Tiger Brands’ Rudi Frankel held another 30%; Metcash’s founder, Lionel Katz, had 20%; and the rest was owned by the public.

Unhappy with sharing control, Kirsh executed a series of sharp manoeuvres to edge out Frankel, building a pyramid structure called Kimet (Kirsh and Metro) with his brother Issy.

Kimet, listed on the JSE in 1978, was hugely successful, despite a patchy record of not always picking the best investments. Still, Kirsh’s purchases of brands including Dion, Greatermans, Russells Furniture and Checkers, meant that by 1979 Kimet handled 12% of all consumer goods in South Africa. Nobody paid attention to Jetro, the small wholesaler he’d bought in New York in 1976.

A supreme dealmaker, Kirsh had indeed become Joburg’s Paul Getty. In 1981, the Rand Daily Mail memorably described him as the “smash-and-grab artist of the year” for his audacious raid on Dion, Russells and Union Wine. The Kirsh group had rapidly become South Africa’s third-largest industrial company, after Barlows and South African Breweries.

Then the tide went out, spectacularly. Interest rates had already hit 25% by mid-1984, and in August 1985, hardliner president PW Botha dashed expectations of meaningful political reform to end apartheid, triggering a flight of foreign capital. For a fledgling retail empire premised on debt, this was a catastrophe.

Syd Vianello, a veteran retail analyst, says Kimet’s businesses began to lose their mojo. “The entrepreneurial energy that had driven them was gone, and it seemed nothing could replace it. Greatermans was a disaster, and a very vibrant Pick n Pay was eating up Checkers’ market share.”

By 1985, with Checkers labouring under expensive long-term leases and with interest rates at record levels, Kirsh needed a R200m capital injection. He reckoned he’d found a white knight in Sanlam, the cash-flush insurer. He formed a new holding company for the consumer businesses called Sanki (Sanlam and Kirsh), with Kirsh holding 51% and Sanlam 49%.

It was a blunder. One Afrikaans businessman told him, “Natie, you chose the wrong partner. You know that Sanlam logo, the two hands holding a globe of the world? Those hands are around your balls now, and when they get the chance, they’re going to squeeze them.”

And so it turned out. Sanlam’s CEO agreed to inject that R200m into the company — but only if Kirsh relinquished control. As Vianello tells it, after much heated discussion Kirsh accepted the inevitable — on condition he could keep Jetro, the small US-based business he’d set up. Sanlam agreed.

At the time, it seemed like a huge capitulation. In retrospect, it was the luckiest deal Kirsh ever did. It is probably a bittersweet irony that the R500bn price tag for Jetro dwarfs Sanlam’s current R192bn market value.

Tentacles of influence

After that, Kirsh stepped back from South Africa’s corporate mainstream to build Jetro into what became a wholesale supplier serving 725,000 smaller US restaurants and food service operators.

By the mid-1980s he was ready to leave South Africa, believing apartheid to be unsustainable. “When I had this fight with Sanlam, I already had very negative views on South Africa. I didn’t really think it was worth fighting for. And I knew that I’d started a fledgling little business in America,” he told the London Business School in 2013.

Jetro wasn’t thriving, but it was “somewhere to go,” he said. And it grew steadily. “Today in the major cities, we own that small-store market. There is no competition because the small wholesalers who used to deliver disappeared, and the big wholesalers deal with the big supermarkets,” he said.

As a private company, Jetro was off the radar. But some influential people noticed. In 2003, Berkshire Hathaway chair Warren Buffett agreed to buy 27% of Jetro, but the deal ultimately fell apart when Buffett and Kirsh couldn’t agree on the price.

Kirsh would still spend half the year in South Africa while remaining resolutely hands-on. He wouldn’t finish an interview with the FM at his Dunkeld office until he had proudly shown journalists his line-by-line tracking of Jetro’s turnover and margins.

Because he had been such a formidable presence in South Africa, it is no surprise that his influence is still keenly felt. One person who credits Kirsh with much of his own success is Chris Seabrooke*, CEO of investment company Sabvest.

“I had finished at Durban High School,” Seabrooke tells the FM, “and I’d completed one year of full-time studying in the early 1970s when I applied for a job as an assistant accountant at Natie’s Commonwealth Shippers”. Kirsh invited him to his sprawling office at the top of the Glencairn building in Joburg’s CBD. “So you’re this new kid from Durban I’ve heard so much about,” Seabrooke recalls Kirsh saying.

Evidently impressed, Kirsh appointed Seabrooke to the board of Commonwealth Shippers at the age of 21, assigning him to lead the Natal business by the age of 23, and had him chairing the company’s credit committee at 24. This underscores how Kirsh leapt decisively, backing the talent he saw. Seabrooke worked with Kirsh’s company for eight years, and the skills he learnt there enabled him to launch Merchant Trade Finance, which later became Sabvest.

“Natie has that rare combination where he is totally on top of the granular detail, but he also sees the big picture,” says Seabrooke. “When you walked into his office, he didn’t begin with pleasantries. It was, ‘I see on page 8, there is an account we need to get on top of’. He managed every facet and every line of the business.”

Mervyn King, the former judge who later gave his name to South Africa’s corporate governance codes, is another individual partly shaped by Kirsh. The story of how they came together offers more insight into Kirsh’s business style.

21st Annual Southern African Internal Auditors Conference.

21st Annual Southern African Internal Auditors Conference.

Professor Mervyn King, is seen on stage (Alon Skuy)

When King was a judge, he happened to adjudicate on Kirsh’s Supreme Court tussle with Rudi Frankel over shareholdings in Metcash. It was a complex case that was expected to last four days. King hurried the advocates along and closed argument after one day — and handed down his judgment the next morning. King says that before the case he “did not know of Kirsh’s existence” — but Kirsh was deeply impressed by the speed and precision of the judgment.

When King resigned from the bench in 1980, Kirsh was quick to invite him to join him as his deputy. “Natie said that together, we could build the biggest trading group in South Africa,” King said in David Williams’ biography of him. “This proposition was more exciting than the other approaches I’d had, and so I decided not to return to the Bar.”

They formed a new company, Kirsh Trading. By March 1982 the group, with annual sales of R2.3bn, was South Africa’s third-largest industrial company after Barlows and SA Breweries.

When his subordinates stand up to him with good reason, he listens and changes

— Clive Weil

The late Clive Weil, the former MD of Checkers, described Kirsh as a “superb risk taker” and “when his subordinates stand up to him with good reason, he listens and changes”.

Size or suitability?

So what does Kirsh’s $29.1bn deal say about South Africa, and the fact that one of the country’s brightest talents secured his biggest coup overseas? Is this an indictment of South Africa’s business climate, or simply a question of size?

Adrian Saville, founder of Boundless World and a professor at the Gordon Institute of Business Science, says this is foremost about market depth. “Jetro is an American business, built by someone over many decades who happens to be South African, exploiting a specific opportunity which he saw in a fragmented and inefficient market to sell wholesale goods to small restaurants and grocers.”

This, says Saville, is the definition of entrepreneurship: providing a solution to a specific problem. “He still had to execute with precision, in an environment that was conducive to that strategy, and which had deep markets — that was his success.”

Saville says this underscores that, measured by its GDP, South Africa remains one of the most prolific producers of multinational corporations. But he concedes that it’s unlikely Kirsh could have done the same thing at home. “Adjusted for the size of its economy, would you have been able to build as effective, as efficient and as profitable in the same amount of time? The answer is ‘no’, because you’d have had a huge number of constraints holding you back.”

While it is possible to build strong businesses in South Africa, managerial bandwidth is often choked by onerous compliance, red tape and regulatory obstacles. And when you overlay infrastructure problems — municipalities failing to provide water, for example — this further reduces the odds of success. “This is a level of friction you just don’t have in places like the US,” says Saville.

Seabrooke agrees that this story is primarily about the larger size of the US market. But he says Kirsh wouldn’t have been able to do what he did at Jetro, had it not been for the experience (and scars) he got in South Africa. “Natie bought one horse in a stable, and he built a battalion of horses around it. But if he hadn’t had the experience to recognise what a good horse is, and a good course, this wouldn’t have happened.”

This is a similar story to that of Koos Bekker and Hans Hawinkels. In 2001 they spotted a small internet business in China called Tencent. Naspers paid $32m (R233m at the time) for 46.5% of the company; by 2021, when Tencent’s share price hit a record high, Naspers’s remaining 31% was worth $280bn (R5-trillion).

But if so much of this story is about spotting the opportunity, it’s also about implementing the plan. Does South Africa have the new breed of hungry entrepreneurs capable of doing this, locally and abroad?

“Absolutely,” says Seabrooke. “We see what South African entrepreneurs can build when they have a larger playing field overseas. They’ve become resilient, building companies in an environment operating under false constraints, so in a more open environment, they fly.”

These “false constraints,” he says, include needless regulations around running businesses and rules around BEE. “You try telling a Frenchman buying a business locally that he is going to pay 100% of the price for it, but he’ll only get 70% of that business. It makes everything more complicated for foreign capital,” says Seabrooke.

Exported talent

For Tony Leon, the former leader of the DA, Kirsh’s success carries profound lessons — particularly in a week in which President Cyril Ramaphosa has lauded R898bn in “investment pledges” to South Africa.

“The lesson for South Africa is that economic success and investment attraction happen when the home market encourages innovation, enterprise, flexibility and rewards entrepreneurs who add value, not just pigment, and not those who simply extract from value already created by others,” Leon wrote on News24.

Leon says it’s not just BEE that needs to be revamped. The government should also look to narrow the remit of the Competition Commission, and ensure a more functional department of trade, industry & competition.

Shapiro says this Kirsh transaction underscores how successful South Africa’s expat men and women have become. “You won’t even have read of many of them, but South Africans have been phenomenally successful in the professions, from accountants to surgeons to dentists. Natie stands out but he’s far from unique.”

Shapiro cites several South Africans who became billionaires overseas. This includes Ivan Glasenberg, the former CEO of Glencore (estimated wealth: $13.8bn); Hilton Schlosberg and Rodney Sacks, the co-CEOs of energy drinks company Monster ($5.3bn each); and Roelof Botha, the former managing partner of venture capital firm Sequoia Capital ($530m).

“What drives them? They all grew up in South Africa, went to fairly average government schools, but all were colossally successful overseas. They grew their businesses, displayed resilience, and the American market opened up for them.”

Is this an indictment of how hostile South Africa is for entrepreneurs, or is it simply that the US provides a much larger canvas?

It’s a bit of both, says Shapiro. “The truth is, if you try to raise money from one of our big banks for a great idea, chances are you’ll get turned down. But in the US, venture capitalists have a real thirst for this kind of thing, and they’ve got money for it.”

In America, Shapiro says, wealth is seen as something to aspire to, and achievable. In South Africa, he says, wealth is viewed with deep suspicion, which mitigates against people learning business skills. “What Natie’s deal shows, yet again, is that we have the talent in South Africa. But we haven’t had an environment that makes it easy for entrepreneurs to succeed, and which rewards them appropriately when they do.”

* Seabrooke is the CEO of Sabvest, which owns 40% of the FM’s holding company, Apex Partners.