OpenAI reported $20 billion in annualised revenue for 2025. They’re targeting $125 billion by 2029. The gap between those two numbers is a bet that a company built on subscriptions can reinvent itself as a diversified commercial platform across four years while burning through $115 billion in cash to get there.

The fate of that diversified commercial platform now lies with advertising and the marketers who control advertising spend. OpenAI’s abandonment of its nascent shopping platform last week left advertising as the single remaining mechanism that can plausibly bridge the gap to its $125 billion future.

OpenAI, which once derided advertising, must become an advertising company or fail to hit its target and justify its insane valuations.

To understand why, you need to start with something that doesn’t get discussed enough: OpenAI, Anthropic, and Google are not running the same business. They are running three fundamentally different businesses with diverging unit economics — and OpenAI really drew the short straw on which one it ended up with.

ADVERTISEMENT

Three companies, three very different problems

OpenAI is a consumer company. The revenue profile makes this explicit. By mid-2024, subscriptions accounted for approximately 85% of its ARR. Individual ChatGPT Plus subscribers — people paying $20/month — represented the largest single revenue bucket, outpacing both enterprise and API revenue by a wide margin. By April 2025, the individual subscription share had climbed to roughly 68% of total revenue. OpenAI’s money comes primarily from people, not corporations, and it comes in predictable, capped, monthly increments.

Anthropic is a B2B infrastructure company. Roughly 70-75% of Anthropic’s revenue comes from API token consumption — enterprises paying per token for access to Claude. As of early 2026, Anthropic had 300,000+ business customers accounting for approximately 80% of revenue. More than 500 customers spend over $1 million annually. Eight of the Fortune 10 are Claude customers. Claude Code — launched publicly in May 2025 — hit $2.5 billion in annualised revenue by February 2026, in nine months. The business is structured around usage expansion, not subscriber growth: when a customer’s product succeeds and their token consumption grows, Anthropic’s revenue grows with it, without any additional sales motion.

Google’s Gemini is an integrated play. It doesn’t need a standalone business model because it has one by default. Google generates over $200 billion annually from advertising, and Gemini’s purpose is to protect and extend that business — keeping users inside the Google stack, making G-Suite stickier, extending Google’s reach into the AI assistant layer. Gemini’s “success” is measured by its contribution to Google’s existing P&L. The AI features ship pre-integrated into every Google Workspace seat by default.

They represent fundamentally different ceiling problems and business architectures. I think this gets missed a lot in the OpenAI / Anthropic / Gemini debate.

The consumer ceiling is OpenAI’s defining constraint. Consumers expect predictability. The population willing to pay $20-30/month for an AI assistant has a ceiling — it’s a large ceiling, but it’s a ceiling — and OpenAI is already approaching maturity in its highest-income markets. Roughly 5% of ChatGPT’s 800 million weekly active users are paying subscribers. Getting the next 5% to convert requires either dramatic price cuts (which hurt margins) or demonstrating enough incremental value to overcome payment friction. Basically: they need to make GPT much better than it is today (which is hard without causing the unit economics to fail). Neither is a clean path to $125 billion.

Anthropic doesn’t have this problem in the same form. Token consumption compounds naturally as enterprises build more workflows on Claude. The product doesn’t need to convince a consumer to upgrade a tier — it just needs the enterprise’s applications to succeed, and usage follows. Structurally superior unit economics at scale.

This divergence reflects founding DNA, not just strategy. Dario and Daniela Amodei left OpenAI to build a different kind of company. Sam Altman’s background pulled in the opposite direction. He spent five years as president of Y Combinator — the world’s most prolific startup accelerator — and before that built Loopt, a consumer location-sharing app that raised over $30 million and sold for $43 million in 2012, widely considered a disappointing outcome. His entire professional framework was built around one philosophy: fund a lot of things, see what gets traction, double down on the ones that work.

OpenAI’s product strategy looks like that philosophy applied to a company with a $300 billion valuation. The volume of surface area is remarkable. Since 2023: Browse with Bing launched and disabled within weeks, relaunched in a different form. ChatGPT Plugins launched as the ecosystem play — hundreds of integrations — killed entirely by April 2024 and replaced with Custom GPTs. The GPT Store, promised in November 2023, delayed by the board coup, launched January 2024, never achieved meaningful commercial or creator revenue traction. SearchGPT launched as a standalone search product in July 2024, folded into ChatGPT rather than standing alone. Pulse is questionable. And now, Instant Checkout — direct commerce inside ChatGPT, launched September 2025, pivoted six months later.

Back to the future: Claude Code does not have an elaborate interface

Compare that to Anthropic. Claude Code: launched May 2025. One product. One use case. Zero to $2.5 billion ARR in nine months. No deprecations, no abandoned protocols, no pivots.

Y Combinator’s spray-and-pray approach creates value at the portfolio level because the fund doesn’t need every company to work. But a single company operating on $115 billion in planned cash burn doesn’t have portfolio mathematics. When OpenAI launches a product, gets merchants to build integrations, runs public announcements, and then retreats — the cost isn’t just the engineering time. It’s the trust tax on every future launch. And the shopping failure is the most expensive version of that pattern so far. Every single time this happens, OpenAI signals that it is less reliable as a development partner.

What the forecast actually requires

Start with the math OpenAI has shared with investors. Their internal projections, reported by The Information, show roughly $125 billion in 2029 revenue broken into three buckets: just over 50% from ChatGPT subscriptions (~$62B), roughly 20% from API developer sales (~$25B), and approximately 20% from what the documents call “other products” — a category that includes video generation, search, advertising, and commerce (~$25B).

That third bucket is the one doing the heaviest lifting in terms of narrative. Subscriptions and API revenue are relatively legible. You can model them from current ARR trajectories, pricing dynamics, and competitive pressure. The “other products” bucket is where OpenAI needed to demonstrate it could build new monetisation models from scratch. Commerce was the clearest articulation of what that category was supposed to look like.

The author Henry Innis

To understand why, consider the subscription math alone. OpenAI has approximately 800 million weekly active users. Roughly 5% are paying subscribers — around 40 million people at an average of $20-30 per month. That gets you to $10-14 billion in annualised consumer subscription revenue. Add enterprise contracts, team plans, and API revenue and you get to the $20 billion ARR figure they hit in 2025. But to reach $62 billion from subscriptions by 2029, you’d need either six times more paying users at current ARPU, or dramatically higher prices, or both. That’s a ceiling problem, and it’s why the “other products” bucket wasn’t optional. Commerce, advertising, and agents were the diversification play that made $125 billion even theoretically reachable.

Why commerce didn’t work

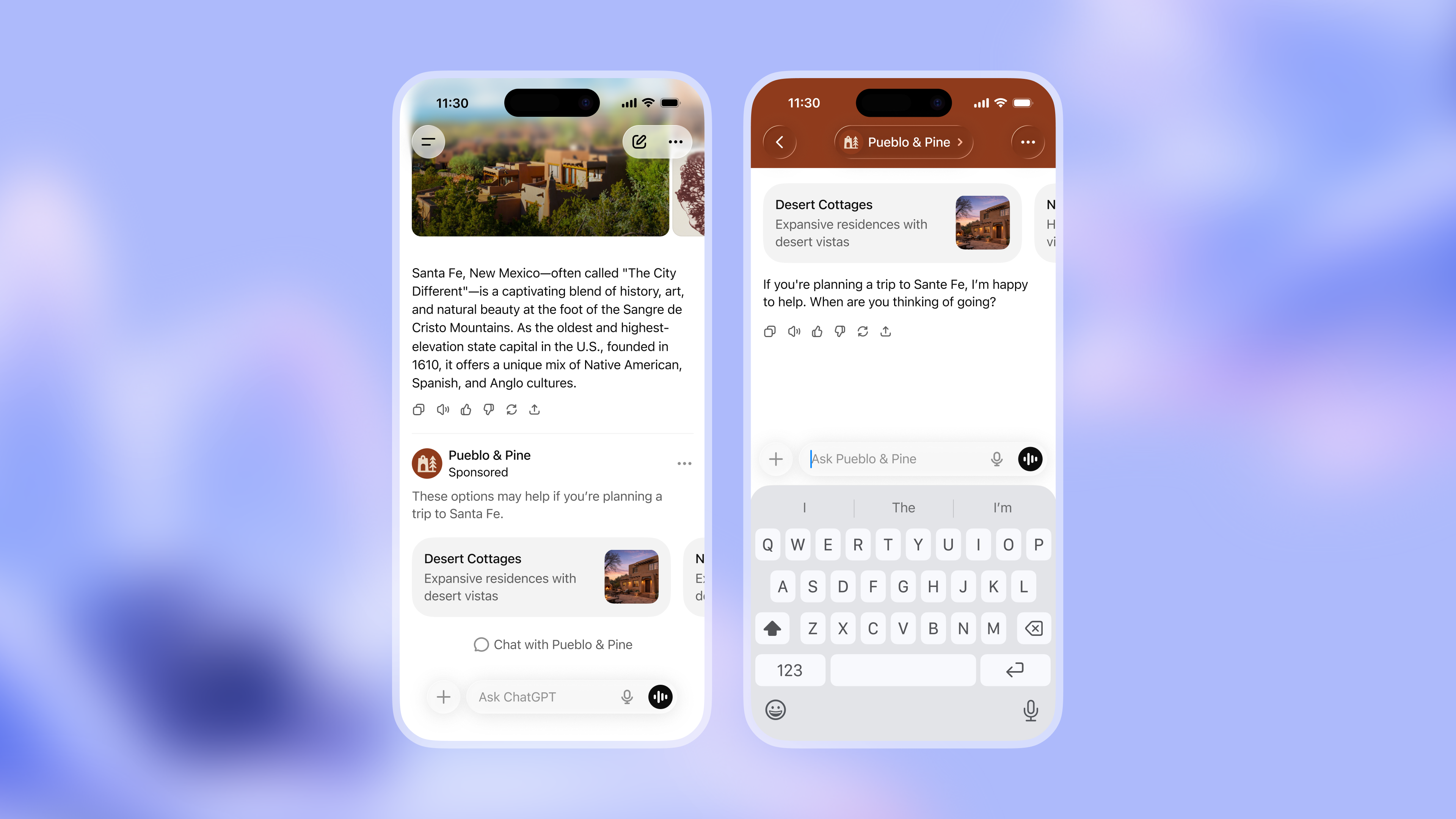

The September 2025 launch of ChatGPT Instant Checkout was supposed to begin building towards the 2029 $25b “other products” number (with advertising). Shopify, Etsy, and a handful of other platforms were signed as launch partners. Etsy went as far as subsidising merchants’ commissions to accelerate adoption. In OpenAI’s telling, this was the beginning of an entirely new commerce channel.

The actual results were devastating in their specificity. Of Shopify’s millions of merchants, roughly a dozen were actively transacting through AI tools at the point of pullback. Not a slow ramp — a dozen. Shopify’s president, Harley Finkelstein, put the failure squarely on the AI companies, not the merchants, saying the constraint was “waiting for agent applications to continue opening up.”

The user behaviour data told a similar story. People used ChatGPT extensively for product research and comparison, but went back to Amazon, Shopify, or brand sites to actually buy. The conversion funnel broke at the transaction step. OpenAI had successfully replicated the discovery phase of shopping. They had not replicated the trust infrastructure — saved payment methods, purchase history, return policies, loyalty programmes — that makes people complete the transaction.

There were also structural failures that go beyond user behaviour. OpenAI had not built state sales tax compliance infrastructure across US jurisdictions as of February 2026. This isn’t a trivial gap — sales tax collection and remittance across thousands of US local jurisdictions is a foundational requirement for any checkout platform at scale. Amazon, Shopify, and eBay have spent years building this. OpenAI launched a checkout product without it. The real-time inventory sync problem was similar: pulling live price, availability, and shipping data from potentially millions of merchants simultaneously requires infrastructure that takes years to build, not months.

These weren’t surprising post-launch discoveries. They were requirements that should have gated the launch. The fact that they didn’t is exactly the YC pattern: ship it, see what happens, figure out the infrastructure later. That philosophy works when you’re a six-person company with $500k from an accelerator. It has a different cost profile when you’ve announced the product to millions of users and signed merchant partners who’ve restructured their go-to-market around it.

OpenAI confirmed the strategic retreat this week: Instant Checkout is “transitioning to apps,” meaning Instacart, Target, Expedia, and Booking.com will handle the transaction layer while ChatGPT provides the discovery layer. Etsy subsidised merchant commissions and got nothing. The Agentic Commerce Protocol, positioned as OpenAI’s answer to Google’s Universal Commerce Protocol, is now described as infrastructure for app-based purchases — a significantly less valuable position in the value chain.

The Instant Checkout retreat and move to partners like Instacart means OpenAI has lost its direct commerce take-rate — a reported 2% commission model largely disappears – and any serious commerce revenue is now delayed by at least 2-3 years.

On my maths, this blows a $5-10b hole in the 2029 revenue forecast.

The problem of valuation credibility

OpenAI CEO Sam Altman has a big challenge ahead to justify valuation

This is the more damaging part of the equation.

OpenAI is working toward an IPO, reportedly targeting a filing in H2 2026 at a valuation somewhere between $730 billion and $830 billion based on recent secondary transactions. A business valued at $830 billion on ~$20 billion of current revenue is trading at roughly 40x forward revenue. That multiple is only justifiable if investors believe in the diversification story — that OpenAI is not a subscription software company but a platform that will monetise across commerce, advertising, agents, and API infrastructure simultaneously.

Every product retreat makes that story harder to tell. The shopping pullback is not an isolated event — it sits alongside a pattern that includes the April 2025 shopping launch (product recommendations without monetisation), the September 2025 Instant Checkout launch (only a dozen merchants), and the March 2026 retreat (back to third-party apps, no transaction revenue). Three distinct announcements, one net outcome: no commerce revenue.

When a company trading at 40x forward revenue loses $5-10 billion of that revenue from a category that was publicly articulated as a strategic priority, the multiple contraction is not linear. The question investors start asking is not “how much does this change the 2029 number?” but “how much of the rest of the forecast should we haircut for the same reason?” Agents at $200-$20,000 per month. Advertising as a $25 billion business. API revenue in a market where open-source models are compressing margins. Each of these carries meaningful execution risk. The shopping retreat doesn’t prove those will fail — but it provides evidence that OpenAI’s track record of launching revenue streams and seeing them through is not yet established.

The ads division inherits the problem

When commerce failed, the pressure didn’t disappear. I think the revenue responsibility shifted — and it shifted to advertising, which is now the single remaining mechanism that can plausibly fill the “other products” bucket. That will make marketing chiefs front and center to the survival of OpenAI in the coming months.

The timeline of Sam Altman’s public position on advertising pretty neatly dovetails with when he would have been getting early signals commerce wasn’t working out.. October 2024: Altman told a Harvard fireside chat he “hated” ads and called combining AI with advertising “uniquely unsettling,” describing advertising as a “last resort” business model. July 2025: on The OpenAI Podcast, he said he wasn’t “totally against” advertising and referenced Instagram. October 2025: he publicly described a 2% affiliate fee model on purchases made through Deep Research. December 2025: ad-related code surfaces in the ChatGPT Android beta and is quickly pulled. January 2026: OpenAI announces it will begin testing ads for free and Go tier US users. February 2026: ads go live.

From “last resort” to live testing in sixteen months. That is not a considered product strategy. That is a company responding to financial pressure in real time — and the commerce failure is what accelerated the timeline.

Heavy lifting: How ads appear in ChatGPT

The structural case for advertising is real. 800 million weekly active users, 95% of them not paying, with rich conversational intent data that no other advertising platform has access to. Internal projections forecast $1 billion in 2026 from “free user monetisation,” scaling toward $25 billion by 2029. Fidji Simo — hired as CEO of Applications in May 2025, who spent over a decade at Meta building Facebook’s advertising business — was not a subtle hire.

The structural problem is equally serious, and it comes in three parts.

First: OpenAI built its brand on being the anti-Google — the AI that gives you useful answers rather than optimised-for-advertiser answers. When a user asks ChatGPT “what should I buy for X” and a sponsored result appears below the answer, the implicit question is: would the answer have been different without the advertiser? That is a genuine trust tax on the core product. Altman has been careful to frame ads as clearly separated from answers, never influencing recommendations. But the early test format — bottom-of-response placement, labelled as sponsored, contextually targeted to the conversation — creates exactly the kind of tension that erodes the “ad-free intelligence” positioning that drove adoption in the first place.

Second: the revenue math at the required scale is unproven in this format. The current early-test CPM is reportedly around $60, with a minimum $200,000 advertiser commitment that limits buyer supply. Perplexity’s advertising experiment — the closest comparable — has not demonstrated that AI chatbot ads are reliable at scale. The 2026 forecast of $1 billion requires a product that doesn’t yet exist at the quality, reach, and advertiser sophistication that number demands.

Third: OpenAI is competing for advertising budgets with Google, which has a 25-year head start on advertiser relationships, targeting infrastructure, measurement, and attribution. Google is simultaneously integrating ads into Gemini and AI Overviews. The new AI advertising channel won’t belong to OpenAI by default, and the incumbents have structural advantages that are very hard to overcome on the timeline the forecast requires.

The advertising business needs to work. Not eventually — the $1 billion figure is a 2026 number, and the fiscal year is already underway.

The $125 billion problem

The $125 billion forecast is not at immediate risk. OpenAI hit $20 billion in 2025 ARR and is growing fast. Subscriptions are real. API revenue is real. The enterprise business is accelerating. There is a credible path to $50-60 billion by 2029 on the strength of what they already have.

But $125 billion requires a company that has figured out how to monetise its non-paying users, how to extract transaction value from the commerce intent flowing through 800 million weekly users, and how to build advertising and agent revenue that meaningfully supplements subscriptions. The shopping retreat is evidence that the first two of those are harder than OpenAI publicly claimed. The “other products” bucket is now materially less certain, and advertising is carrying the weight of a thesis that commerce was supposed to share.

For a company going public at a valuation implying they will match Nvidia’s revenue within four years, that uncertainty is not a footnote. It’s the central question. And at the moment, the answer they’ve given is: we’re sending the users to Instacart, and we’re testing $60 CPMs at the bottom of chat responses.

Advertising has become very central to OpenAI achieving it’s $125bn forecast as a result. And it follows that the next few years may be the most exciting time in advertising in a very long time.