This article first appeared in The Edge Malaysia Weekly on March 9, 2026 – March 15, 2026

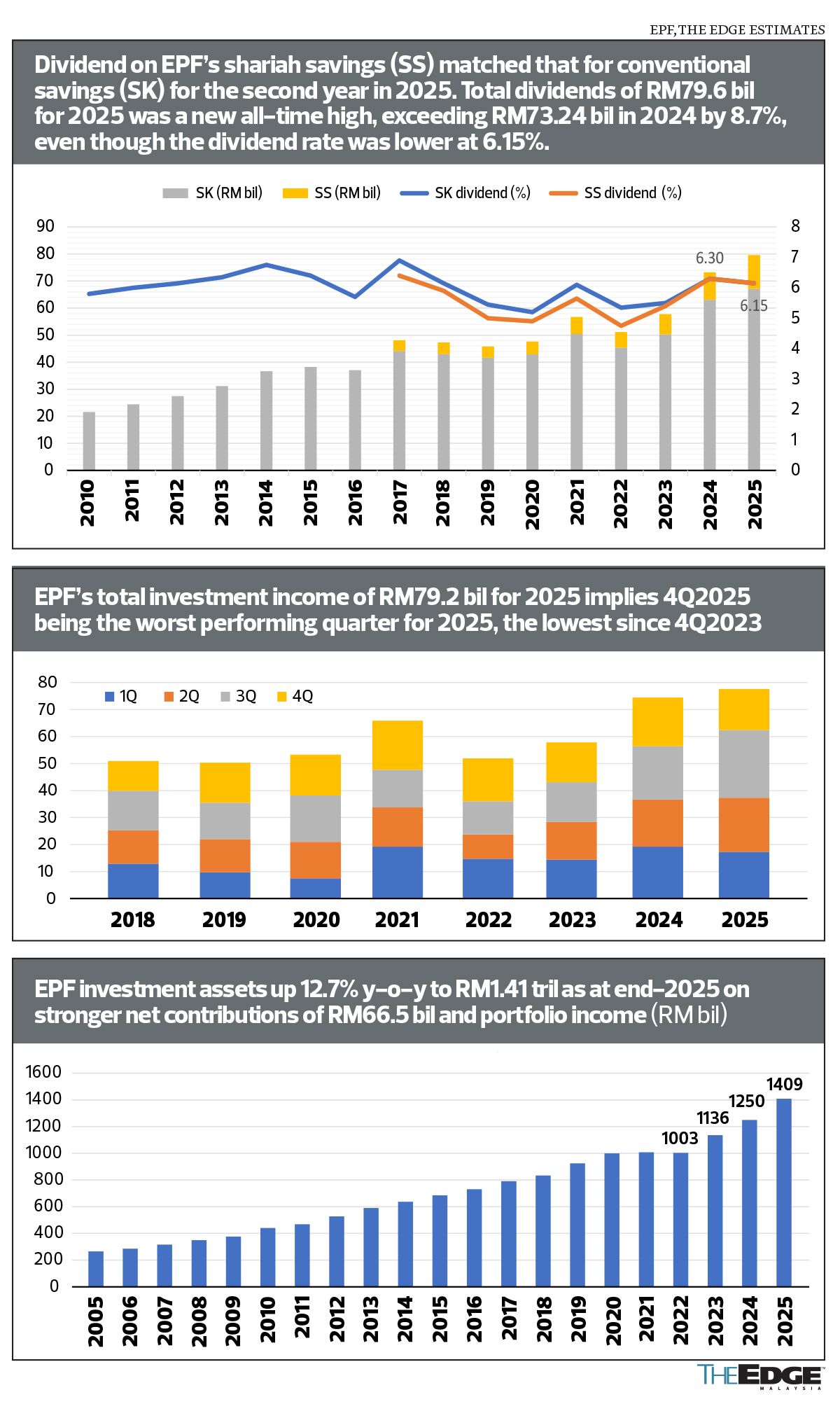

AS it turns out, investment returns for the last quarter of 2025 were the Employees Provident Fund’s (EPF) worst for nine quarters, even as inflows increased, culminating in the fund declaring a dividend of 6.15% for both Conventional Savings (SK) and Shariah Savings (SS) — below public expectations of a rate at least matching 2024’s 6.3%.

In November, The Edge had estimated that the EPF’s 2025 dividend would be at least 6%, with prospects of beating the previous year’s 6.3% if the strong momentum in the third quarter continued into the fourth quarter. It did not.

Unlike in the fourth quarter of 2024, no large profit was locked into its real estate and infrastructure portfolio in the final quarter of 2025. In addition, the EPF’s money market portfolio was likely negatively affected when the ringgit strengthened from 4.20 levels to about 4.05 against the greenback in 4Q2025, our back-of-the-envelope workings show.

EPF CEO Ahmad Zulqarnain Onn told reporters there were two principal reasons why the dividend rate for 2025 was lower than that for 2024 despite the total payout being at a record high. The first reason was Bursa Malaysia’s lower year-on-year growth of 2% versus 12% the year before. The second was returns on some of the EPF’s foreign assets declined thanks to the ringgit strengthening about 10.2% against the US dollar y-o-y, 10.1% against the yen, 5.5% against the renminbi and 4% against the Singapore dollar, while weakening 2.3% against the euro.

Yet, a dividend rate of above 6% is already superb for a RM1.4 trillion retirement fund that only aims to return at least 2% more than inflation on a three-year rolling basis, or a floor of 2.5%, for its 18.1 million (16.6 million Malaysians and 1.5 million migrant workers) members.

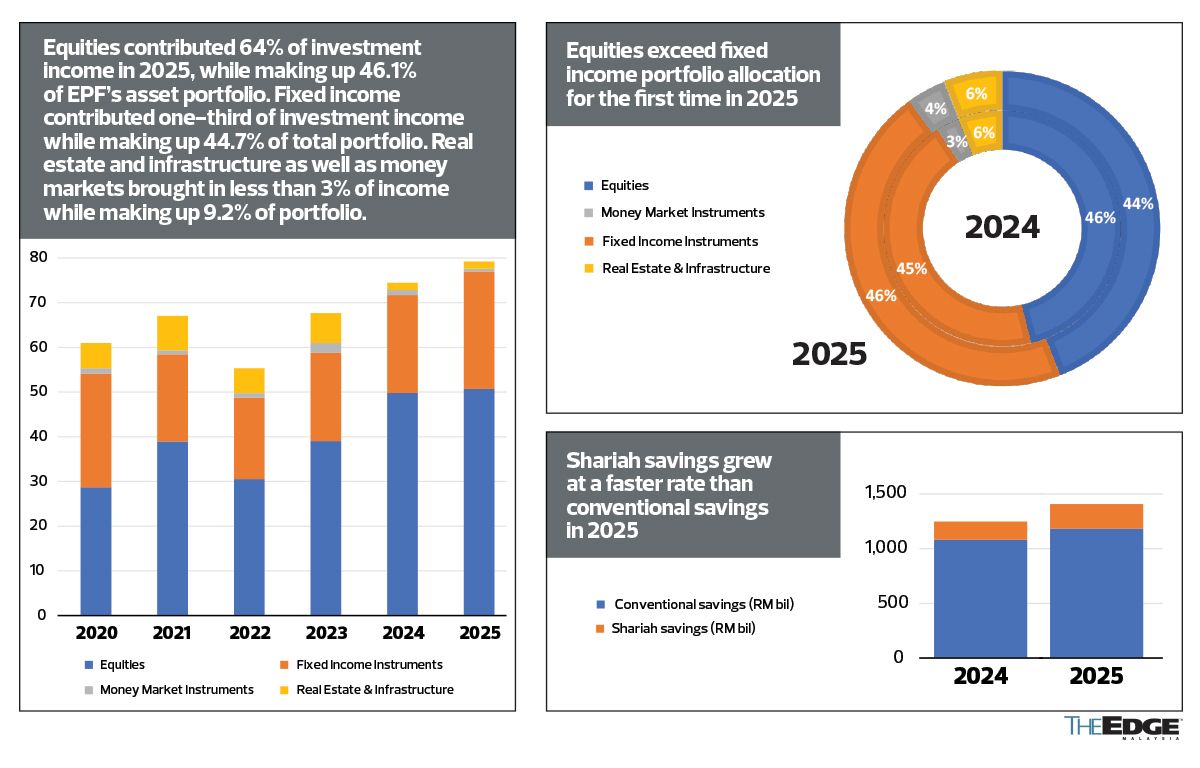

A 6% dividend is no mean feat because close to half of the EPF’s portfolio assets are invested in low-risk fixed-income assets such as government bonds for capital preservation and steady income stream. Traditionally, the EPF’s portfolio allocation for fixed income is more than that for equities, which is the primary driver of income growth or capital enhancement, contributing 64% of total investment income in 2025.

Taking on slightly more risk

In 2025, however, the EPF had 46.1% of its portfolio invested in equities — more than the 44.7% invested in fixed income for the first time. In 2024, it had 46% in fixed income and 44% in equities. Real estate and infrastructure continued to make up 6% of the asset portfolio, while money market assets fell to 3% from 4%.

It is not immediately known if this is temporary or reflects a shift in the EPF’s asset allocation strategy to take on slightly more risk to grow members’ retirement savings faster.

A higher dividend rate shortens the time required to double one’s savings. It takes 12 years to double one’s savings at a rate of 6% per annum compared with 14.4 years at 5% per annum, 18 years at 4% and 28.8 years at 2.5%. EPF savings can double within 10 to 11 years if returns are consistently between 6.5% and 7%.

By asset class, return on investment (ROI) in private equity was the highest in 2025, at 10.47%, followed by 7.73% in public equity and 5.8% in infrastructure. Fixed income ROI was 4.32% in 2025, beating the 4.05% ROI in real estate and 1.61% in the money market. Except for fixed income, ROI was lower across all other asset classes y-o-y.

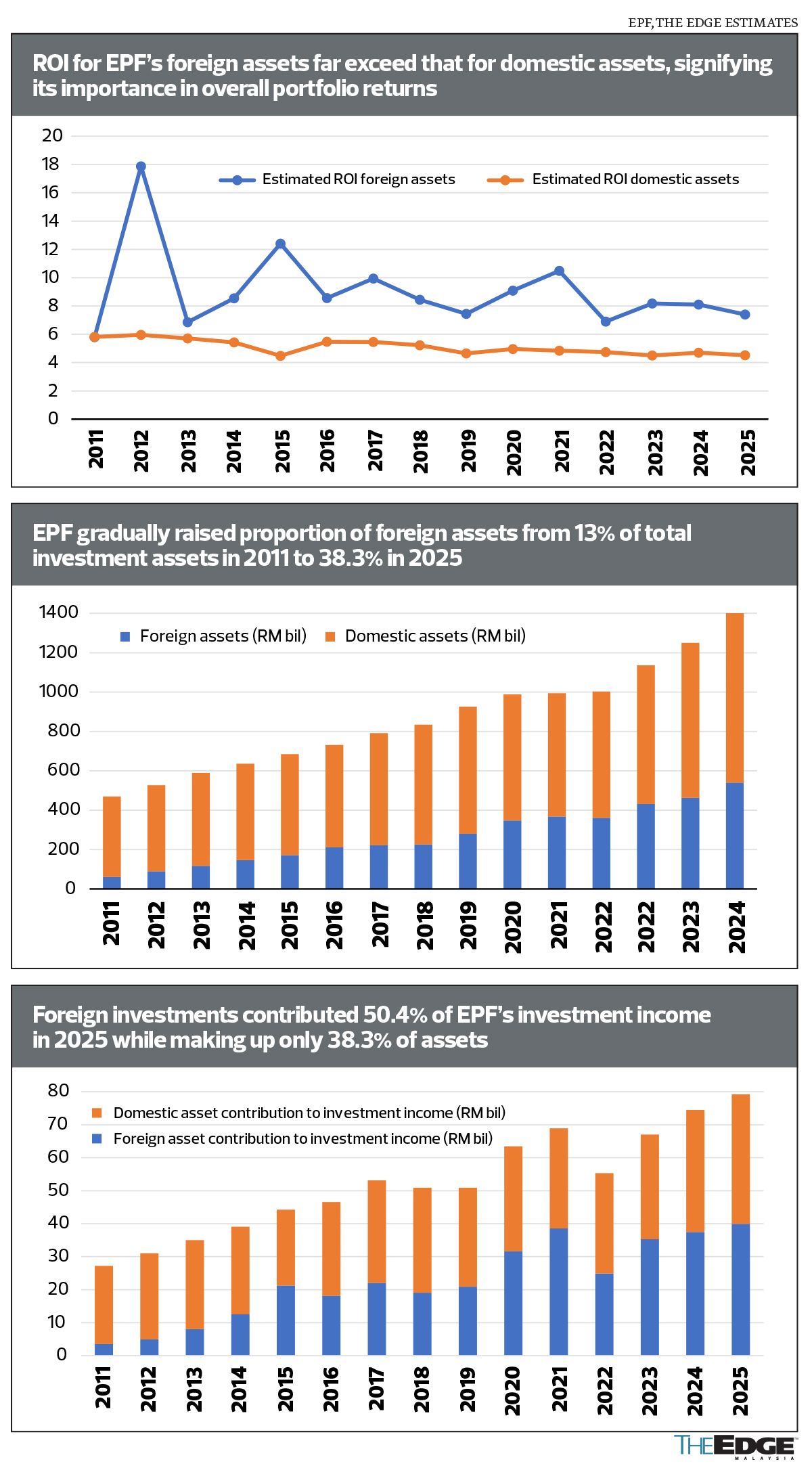

ROI in foreign investments, which account for 38% of total assets, continued to be higher than that in domestic assets.

In 2024, equities accounted for 74% of the foreign investment portfolio, compared with 25% of the domestic investment portfolio while fixed income accounted for 12% of the foreign portfolio versus 67% for the domestic portfolio.

More money looking for good returns

Taking on more risk may well be inevitable if the EPF wants to maintain a high dividend rate as the retirement fund sees higher net inflow.

Net contributions in 2025 amounted to RM66.5 billion, up 33.8% from RM49.7 billion in 2024, as contributions rose 10.4% y-o-y to RM130.2 billion and withdrawals fell 6.6% to RM63.8 billion.

Not only are more wage earners saving more than the statutory required rate but self-employed Malaysians are also voluntarily saving more money, given that savings with the EPF are government-guaranteed and pay higher dividends than fixed deposit interest rates.

Since 2019, the EPF’s annual dividend has consistently exceeded that paid by Amanah Saham Bumiputera (ASB) and Amanah Saham Malaysia (ASM) managed by Permodalan Nasional Bhd’s (PNB) Amanah Saham Nasional Bhd (ASNB).

The EPF also saw a spike in membership late last year as 1.5 million migrant workers and their employers began to contribute 2% of salaries each from October 2025.

While 8.2 million or 77.4% of the EPF’s 10.6 million active members in 2025 were formal-sector Malaysian wage earners, 928,000 were voluntary contributors while half a million wage earners or employers began contributing more than what is required by law, EPF data shows. Voluntary contributions from the 1.4 million voluntary contributors totalled RM19.2 billion or 16% of gross contributions in 2025, up from RM12.3 billion or 13% of total contributions in 2024.

Malaysians can open an account with the EPF from the age of 14 and contribute savings until age 75, after which the EPF will continue to grow and provide dividends on money saved with it until the age of 100 or demise. Those aged 55 and above are free to withdraw savings (except for savings deposited between the ages of 55 and 60) while those aged below 55 can withdraw from Account Flexible 3 and any amount above RM1.1 million in 2026, amounts above RM1.2 million in 2027 and amounts above RM1.3 million in 2028 in line with the EPF’s recommended enhanced savings threshold. The EPF’s basic savings threshold was revised to RM390,000 from RM240,000 previously, with the recommended adequate savings threshold at RM650,000.

Tougher to pay every 1% of dividend

With the EPF’s total investment assets having grown 12.7% y-o-y to RM1.409 trillion at end-2025 from RM1.25 trillion at end-2024 and its total members having grown 11.5% to 18.09 million in 2025 from 16.2 million in 2024 (of whom active members grew 20.6% y-o-y to 10.59 million in 2025), it gets tougher to earn and pay every 1% of dividend to members.

The total dividend payout of RM79.6 billion (RM67.1 billion for SK and RM12.5 billion for SS) in 2025 was the highest on record — exceeding RM73.24 billion (RM63.05 billion for SK and RM10.19 billion for SS) in 2024, even though the rate was lower at 6.15% in 2025 compared with 6.3% in 2024.

Yet, the payout in 2024 would only have been enough to pay a dividend of 5% for SS and 5.8% for SK in 2025, our back-of-the-envelope calculations show. That is because the amount necessary to pay 1% of dividend to each EPF member has grown to nearly RM13 billion and will continue to grow as long as there is more inflow than outflow.

Shariah versus conventional

The difference in the illustrated dividend rate is because SS grew at a faster rate than SK in 2025, which is easier to achieve even as SS grew to RM224 billion or about 16% of total investment assets in 2025 compared with RM167 billion or about 13% of the EPF’s total assets in 2024.

The dividend for SS matched that for SK for the first time in 2024 and continued in 2025, after the EPF separated the management of the funds. For example, fixed income made up 45% of SK but only 42% of SS while public equity made up 41% of SK but 49% of SS, EPF data shows. Both portfolios had 38% invested abroad.

To illustrate, a smaller pool of funds means that RM1 billion of investment income is enough to pay a 0.5% dividend for SS but less than 0.1% for SK, back-of-the-envelope calculations show.

In its earnings release, EPF chairman Tan Sri Mohd Zuki Ali says, “[The] EPF remains cautious in its outlook as global uncertainties persist. Our investment approach remains anchored on discipline, diversification and strong governance. As a long-term retirement fund, EPF operates with a multi-year investment horizon, recognising that returns may vary from year to year while remaining focused on sustainable returns over time, enabling members to benefit from compounding [power] to grow their savings.”

The EPF is expected to release its first-quarter income performance report by the middle of June or as early as late May.

Save by subscribing to us for

your print and/or

digital copy.

P/S: The Edge is also available on

Apple’s App Store and

Android’s Google Play.