Callaway Golf stock in focus after name change

Callaway Golf (CALY) is back in the spotlight after reverting to its historic name in January 2026, following a period as Topgolf Callaway Brands Corp. The move is drawing fresh attention to its core golf equipment and apparel business.

See our latest analysis for Callaway Golf.

The recent name change headlines arrive as momentum rebuilds, with a 16.9% year to date share price return and a 107.3% 1 year total shareholder return contrasting with weaker 3 and 5 year total shareholder returns.

If this kind of turnaround story has your attention, it could be a good moment to broaden your search and check out 20 top founder-led companies

With Callaway delivering a 107.3% 1 year total return yet still trading below an average analyst price target, the key question is simple: is this rebound only catching up to fundamentals, or already pricing in future growth?

Most Popular Narrative: 16.2% Undervalued

Callaway Golf’s most followed narrative pegs fair value at $16.35 per share versus the last close at $13.70, putting the current rebound against a richer long term story.

Ongoing international expansion and new venue openings are adding to the recurring and predictable revenue base. This plays directly into the global trend of rising participation in experiential leisure activities and underpins longer-term earnings and cash flow growth.

Curious what kind of revenue path and profit profile are baked into that fair value, and how a higher earnings base feeds into the long term multiple story.

On the numbers, the narrative ties its $16.35 estimate to a model that leans on higher earnings over time, using an 8.27% discount rate to bring future cash flows back to today. That framework also assumes Callaway Golf can support a valuation multiple consistent with a healthier profit margin than it currently earns, helped by its mix of golf equipment, apparel and entertainment exposure.

Result: Fair Value of $16.35 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this upbeat story still runs into real friction, including pressure from discounting at Topgolf venues and questions about whether softer regions and segments can stabilize.

Find out about the key risks to this Callaway Golf narrative.

Another Angle On Valuation

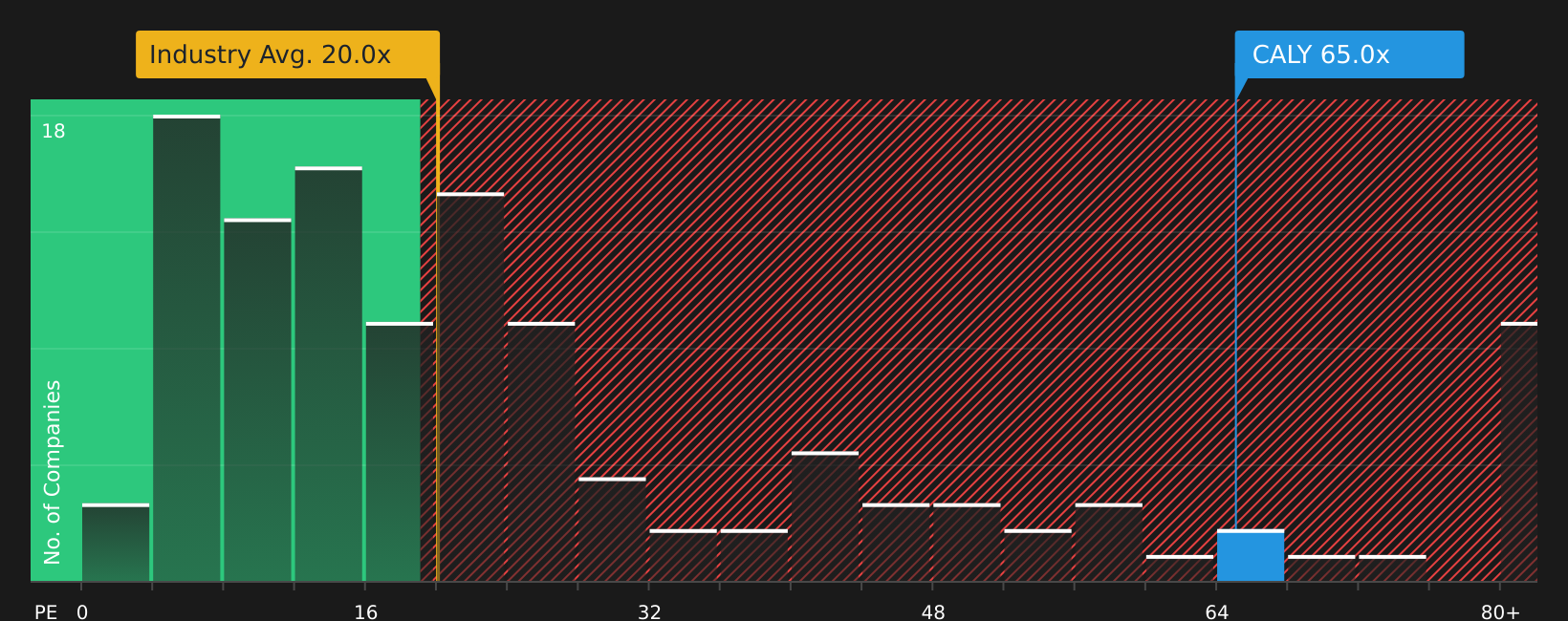

That $16.35 fair value from the narrative contrasts sharply with what the current earnings multiple suggests. At $13.70, Callaway Golf trades on a P/E of 65x, versus 28.5x for peers and 20.4x for the wider Leisure group, and above an estimated fair ratio of 35x. This points to a richer price tag than the story implies, raising the question of which signal to trust more right now.

To see how this earnings based view stacks up against a fuller breakdown of assumptions and risks, take a close look at See what the numbers say about this price — find out in our valuation breakdown.

NYSE:CALY P/E Ratio as at Mar 2026Next Steps

NYSE:CALY P/E Ratio as at Mar 2026Next Steps

With a mix of optimism and concern running through this story, it makes sense to move quickly, review the numbers yourself, and weigh both sides using 1 key reward and 1 important warning sign.

Looking for more investment ideas?

If you stop at one stock, you risk missing opportunities that better fit your goals, so keep your options open and let data rich tools do the heavy lifting.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com