In recent weeks, Kraft Heinz held now-concluded talks with Unilever about merging parts of their food businesses, while also announcing a five-year global condiment partnership with the NFL and launching PowerMac, a higher-protein, higher-fiber version of Kraft Mac & Cheese set to reach major US retailers from April 2026.

Together, these moves highlight Kraft Heinz’s attempt to refresh its portfolio and brand relevance through health-oriented innovation, sports-led marketing, and previously explored large-scale portfolio reshaping.

We’ll now examine how the NFL partnership, in particular, might influence Kraft Heinz’s existing investment narrative around brand reinvestment.

Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

To own Kraft Heinz today, you need to believe that heavier brand and product reinvestment can offset recent volume pressure and impairments, eventually restoring earnings and validating its large brand portfolio. The key short term catalyst is whether stepped up marketing and innovation spending can stabilize North America retail volumes after weak results and a double digit stock pullback. The biggest risk remains that ongoing volume declines and margin pressure persist despite higher spending, making recent news directionally relevant but not yet clearly transformative.

Among the recent announcements, the five year NFL partnership is most directly tied to this reinvestment story. It materially amps up visibility for Heinz and other condiments around premium viewing occasions like the NFL Draft, overseas games, and the Super Bowl. For investors tracking whether higher marketing spend can translate into improved volumes and pricing power in North America retail, this agreement is a concrete, high profile test case of the reinvestment thesis at work.

Yet against all this brand activity, investors should still pay close attention to the risk that innovation and marketing may not fully offset…

Read the full narrative on Kraft Heinz (it’s free!)

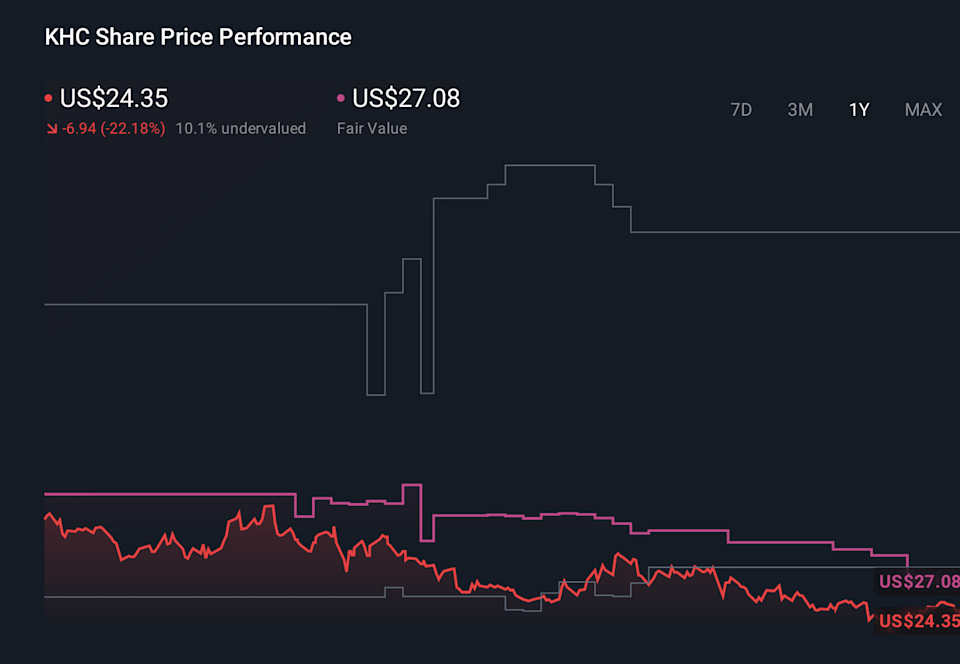

Kraft Heinz’s narrative projects $24.9 billion revenue and $2.8 billion earnings by 2029. This implies fairly flat yearly revenue growth and a $8.6 billion earnings increase from -$5.8 billion today.

Uncover how Kraft Heinz’s forecasts yield a $25.03 fair value, a 16% upside to its current price.

KHC 1-Year Stock Price Chart

KHC 1-Year Stock Price Chart

Before this news, the most optimistic analysts were assuming Kraft Heinz could swing from roughly US$5.3 billion in losses to about US$5.1 billion in earnings, but compared with concerns about North America volume declines and brand relevance, this more upbeat view might now look either too cautious or too hopeful depending on how you see these new moves playing out and it is worth comparing both sides before you decide where you stand.

Explore 18 other fair value estimates on Kraft Heinz – why the stock might be worth over 2x more than the current price!

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Early movers are already taking notice. See the stocks they’re targeting before they’ve flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include KHC.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com