If you contribute regularly to your TFSA you already know this, but it’s worth repeating. Your My CRA Account is not a live tracker of your TFSA contribution room.

In fact, it can be frustratingly slow to update.

The reason is straightforward. Financial institutions have until the end of February each year to report your prior year TFSA activity to the CRA. That includes contributions, withdrawals, and the year-end value of your account. Until that information is received and processed, your contribution room is incomplete.

So the number you see early in the year includes your new annual limit, but ignores everything you did last year.

That’s why the number comes with a warning.

Last year, Globe and Mail reporter Erica Alini highlighted just how messy this can get, noting that delayed or missing TFSA data makes it harder for Canadians to avoid costly overcontribution penalties. And, indeed, it was messy, as TFSA contribution room wasn’t updated until June last year.

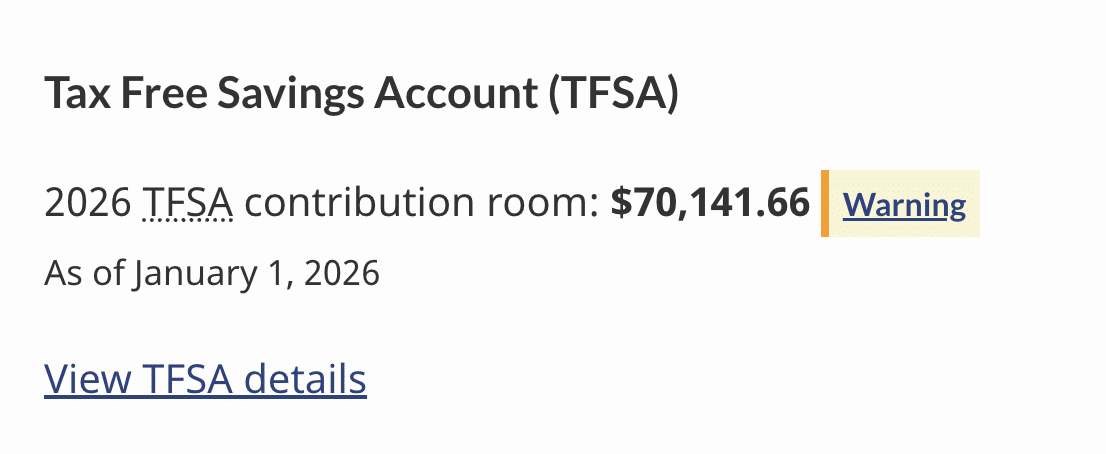

2026 TFSA Contribution Room Has Been Updated

The good news is that as of March 21, 2026, the CRA appears to have caught up. Your TFSA contribution room now reflects your 2025 activity and shows your available room as of January 1, 2026. That includes the new $7,000 limit, but still does not include anything you’ve done so far in 2026.

That’s about as current as it gets (for me).

This is also why I always suggest tracking your TFSA activity yourself, especially if you don’t max it out every year, and especially if you’ve made withdrawals (looking at myself here).

I’m now on round three of filling up my TFSA after draining it twice, once in 2011 and again in 2022, both times for home purchases.

The key thing to understand is that withdrawals are not lost room. You get that contribution room back on January 1 of the following year. But you’ll see why it’s important to keep track.

Below is my own TFSA history to show how this works in real life. You’ll see how contribution room builds over time, how it resets after withdrawals, and how that room comes back the following year.

DateContribution Room ($)ContributionsWithdrawals

1-Jan-26$70,141.66

1-Jan-25$113,132.43 $50,000 $9.23

1-Jan-24$130,132.43 $24,000 $0

1-Jan-23$123,132.43 $0 $0

1-Jan-22$6,000.00 $6,000 $116,632

1-Jan-21$6,000.00 $6,000 $0

1-Jan-20$38,500.00 $38,500 $0

1-Jan-19$44,500.00 $12,000 $0

1-Jan-18$50,500.00 $12,000 $0

1-Jan-17$56,000.00 $11,000 $0

1-Jan-16$50,500.00 $0 $0

1-Jan-15$45,000.00 $0 $0

1-Jan-14$35,000.00 $0 $0

1-Jan-13$29,500.00 $0 $0

1-Jan-12$24,000.00 $0 $0

1-Jan-11$5,000.00 $0 $14,000

1-Jan-10$5,000.00 $5,000 $0

1-Jan-09$5,000.00 $5,000 $0

If all goes according to plan, I’ll have my TFSA fully maxed again by the end of 2026 using what I like to call the TFSA snowball method. After that, it’s just a matter of coming up with the new annual limit each year.

A few quick takeaways:

Don’t rely on your TFSA contribution room in My CRA Account early in the year

It does not include the previous year’s activity until the CRA processes it

It does not include current year contributions or withdrawals (not a live tracker)

Withdrawals get added back as new room the following January

If you want to avoid penalties, and avoid waiting for CRA to update, keep your own records

Bottom line, My CRA Account is a helpful reference point once everything is updated, but it is not something you should rely on in real time.

And for now, it looks like it’s finally up to date.

This Week’s Recap:

Global equities are down about 8% off of their end of February highs. It’s a reminder that markets don’t move up in a straight line.

In fact, it was this time last year when I started getting panicky emails from readers and clients about the liberation day tariffs that were about to take effect.

Well, after a week of sharp market declines (~12% or so), markets rebounded and soared to new all-time highs. Another reminder – “nobody knows anything”.

Meanwhile, how were you feeling about your portfolio in September or October of last year? Pretty good, I imagine. That’s where we are sitting today, with global markets back to prices last seen in the fall. Not too bad, considering we’ve had three years in a row of outstanding returns. Patience.

On that note, last weekend I explained why we’re investors and not speculators.

Promo of the Week:

Just over a week left in Wealthsimple’s Unreal Deal promotion.

You have until March 31st to register for the promotion, and then 30 days after that to initiate the transfer(s).

Here’s the straightforward version of the offer:

New customers open a new Wealthsimple account (here, use my referral link and get an extra $25).

New and existing customers: Register for the Unreal Deal promo before March 31st.

Transfer $25,000 or more from another financial institution.

Choose your match:

– 1% paid over 1 year

– 2% paid over 3 years

– 3% paid over 5 years

The bonus is paid monthly into your Wealthsimple chequing account.

Weekend Reading:

Tim Kiladze reports that another private equity fund has halted redemptions (G&M subs), joining a lengthy list of private funds that have gated redemptions due to a mix of high interest rates, lower property valuations, and investors wanting their money out.

Meanwhile, investors are still stuck paying the management fees. High fees, poor returns, little-to-no liquidity. Why are advisors pushing these alternatives so hard? Hmm…

“the Class E units sold through financial advisers, cost 2.65 per cent annually – with one percentage point of that going to the adviser.”

Thanks to Lisa Jackson for including my thoughts in her latest Tangerine article on how to live well on a budget.

How converting your RRSP to a RRIF can help avoid a huge tax hit.

The magician’s trick of dividend safety – or why income investing feels safer than it really is:

“A dividend is not a reward handed down from the market, and it is not a sign that risk has disappeared from your portfolio. It is a transfer. Cash leaves the company and enters your account, and the value of the company adjusts accordingly. Nothing new is created. Wealth is simply rearranged. “

Ben Felix on why 2026 has been a wakeup call for everyone who was convinced that private assets were special:

Housing affordability has been improving, but it’s not enough and may not last much longer.

John Stapleton critiques the Globe & Mail’s Financial Facelift series as unrealistic “champagne wishes and caviar dreams” where nothing ever goes wrong.

Finally, Maclean’s shares a terrific piece on the flight of the Snowbirds, featuring a couple who spent 13 winters in Palm Desert and who won’t be going back any time soon.

Have a great weekend, everyone!