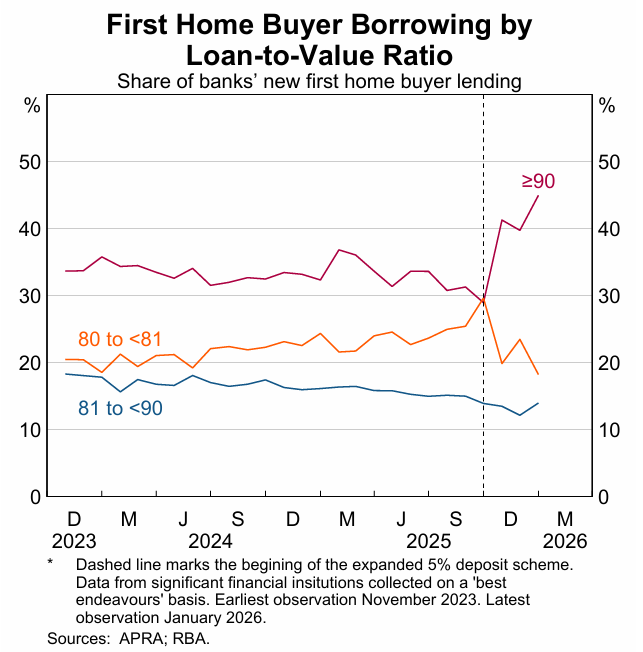

The Reserve Bank of Australia’s (RBA) latest Financial Stability Review reported a sharp increase in high-loan-to-value-ratio (LVR) mortgage lending to first home buyers following the introduction of the expanded 5% deposit scheme on 1 October 2025.

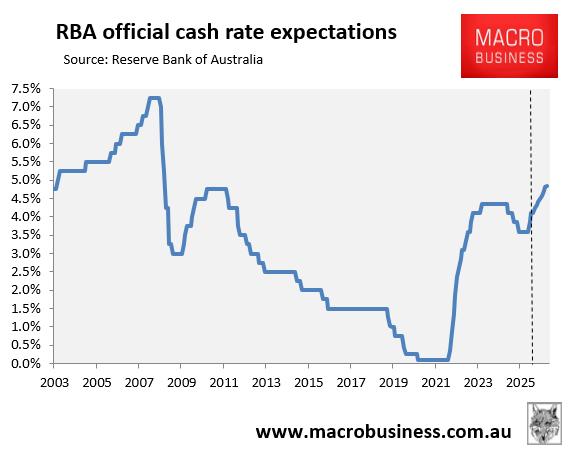

The latest pricing from financial markets suggests that the RBA will raise the official cash rate a further three times this year, bringing it to a 16-year high of 4.85%.

Advertisement

Recent first home buyers will be hoping that the market pricing of the RBA cash rate has overshot.

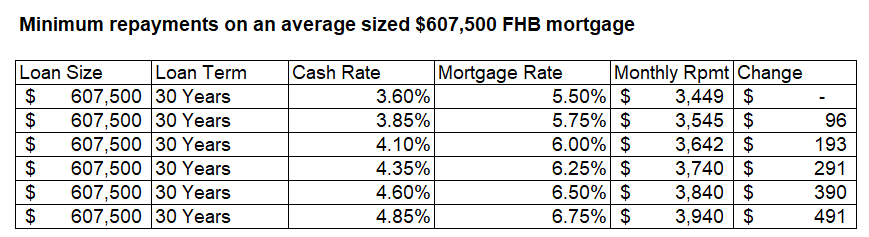

The average size of a new first home buyer mortgage was $607,500 in the December quarter of 2025.

Five 0.25% interest rate hikes over 2026 imply an increase in the discount variable mortgage rate from 5.50% to 6.75% and an increase in average monthly first home buyer mortgage repayments of $491:

Advertisement

For those borrowing at 95% LVR under the 5% deposit scheme, the impact on monthly repayments is likely to be even greater.

The bigger risk is that the impact of the RBA’s monetary tightening coincides with a jump in the unemployment rate amid a recession driven by the global energy shock and tightening financial conditions.

Advertisement

Unfortunately, the Albanese government’s expanded 5% deposit scheme arrived just prior to the RBA’s tightening cycle and the war in the Middle East. Neither scenario was envisioned when the policy took effect in October 2025.

Now, recent Australian first home buyers are facing the real prospect of severe rises in mortgage repayments, unemployment, mortgage stress, and potential negative equity as house prices fall.

Federal government policy has literally pulled vulnerable first home buyers into the market at the worst possible time.

Advertisement