Debt, especially car loans, is an always controversial and much commented subject in the WCI community. It was no surprise when we recently republished an 8-year-old post provocatively titled “Stupid Debts and Their Doctors,” I got tons of emails and comments about it.

As a blogger, I tend to write two kinds of posts. The first type is lengthy, comprehensive, nuanced, and frankly a little boring. I write these to appeal to the financial hobbyists and those looking for a real deep dive on a topic. I use links to those posts when answering questions in my email inbox or on forums. The second type is more of a “shock people into paying attention to their finances” kind of post, where I try to appeal to those who are not hobbyists. I often even try to get the post in front of people who do not yet consider themselves part of the WCI community. These posts are most effective if nuance is deliberately ignored. Even better if they’re a little offensive and have a provocative headline.

The “Stupid Debts and Their Doctors” was clearly the second kind of post. If people prefer the first type, the post on this subject that I generally recommend is “How to Think About Debt” (which has an SEO Title of “Debt: Benefits, Dangers and Guidelines to Follow“).

Provocative and maybe not sufficiently nuanced vs. boring but very nuanced. Your choice.

As I combed through the comments and emails associated with rerunning that first post, I thought it might be interesting to discuss a little more of the nuance around debt. Then, this new post just kept going and going. I hope you enjoy it.

Justification Is Real

One of the first things I notice when I get feedback on this sort of post is a bunch of lengthy diatribes from people with a fair amount of debt in their lives. You get a sense that they feel personally attacked by the post and the idea of, you know, paying off some or all of their debt. It’s as if the post is saying they’re a bad person or they’re bad with money or whatever. Their responses feel very much like a justification of their past financial decisions. They often talk about how low the interest rates are or how good the terms are or all the good things they’re doing with the money instead of using it to pay off debt or how rich they are.

The fact remains that money that is being used to service debt is money that is not going toward helping you live a rich financial life now, much less being invested to help you and others in the future. I intellectually understand the concept of borrowing money at a low rate to make money at a high rate. I just don’t see it actually happening often. When I meet wealthy people, they generally are fairly debt-averse. Yes, they pay off debt, but they also tend to invest plenty of money. They just have a much higher percentage of their income going toward net-worth-increasing activities like paying off debt and investing than is going toward consumptive spending.

Nobody invests all of the difference when carrying debt. Some don’t invest any of it. It doesn’t do you any good to borrow at 0% and not invest at all and then just go spend the difference on something else you want.

More information here:

Should You Pay Off Debt or Invest?

How Fast Can You Get Out of Debt?

Debt Is a Tool

Many people like to argue that debt is a tool. They’re right. It’s a tool. But it’s best not to think of it like a hammer or a vise or even a chainsaw. It’s more like . . . dynamite. Used properly and with careful guidelines and maybe a little bit of luck, it can reduce the amount of physical work required to do something. Used improperly, without proper safety precautions, or with a little bit of bad luck, debt is a tool that can really hurt you. In 2025, 24,000 people declared bankruptcy. Guess how many of them were using debt as a tool?

Rich People Use Debt?

There’s this idea out there that wealthy people somehow borrowed their way to wealth. I’m sure it’s possible to find some people who used debt in some way to help them build wealth. But I think it’s far less common than the relatively unwealthy debtors using this idea to justify their debt believe. I’m fairly anti-debt, but nothing like Dave Ramsey. He sees zero nuance when it comes to debt. His ongoing studies of “every day millionaires” are interesting, even if there is probably some selection bias in the data. He frequently asks these millionaires he interviews about the role that debt played in building their wealth. The most common answer is that it played no role at all, although many will admit they had a mortgage for a while. Few of them built a highly leveraged real estate empire, much less played games with 0% credit card deals.

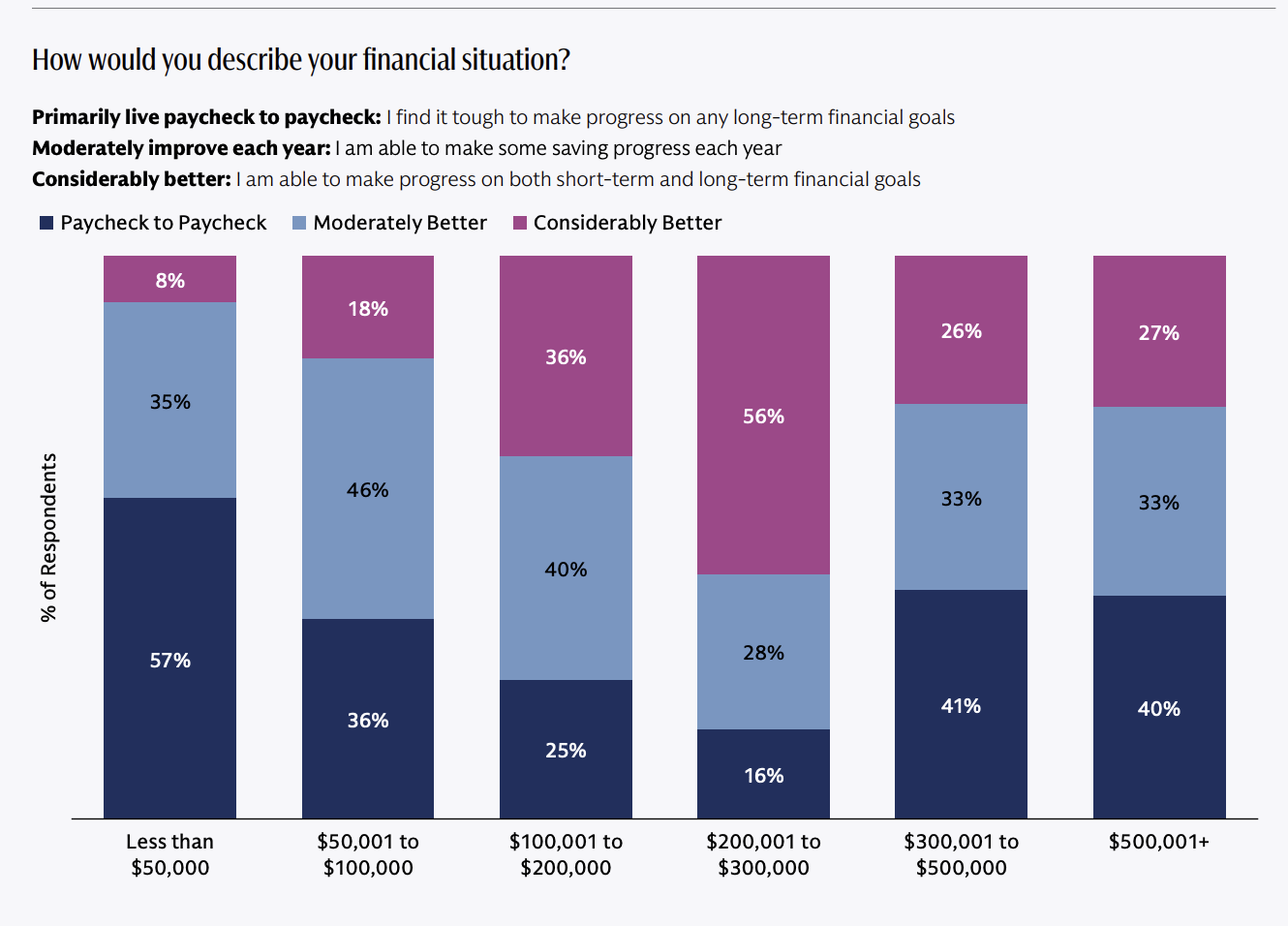

The truth is that those with a higher income (like WCIers) are not necessarily any better at building wealth than those with a lower income. Check out this chart from a 2025 study by Goldman Sachs:

That’s right. Of those making over $300,000, 40% are living paycheck to paycheck. That’s a higher percentage than those making $50,000-$300,000! How does someone live paycheck to paycheck on half a million dollars a year? It generally involves plenty of payments. House payments. Second house payments. Car payments. Boat payments. Student loan payments. Credit card payments. Whatever.

As a general rule, debt is reducing wealth for “rich people” much more than it is increasing it. It’s Behavioral Finance 101.

It’s Dumb Not to Take Loans?

I saw this comment on the Stupid Debts and Their Doctors post:

“All good points except many car loans are 0% like mine. Why would I not take free money? In that situation, it’s dumb NOT to take the loan.”

Seems smart at first glance, right? Surely you can outinvest 0%. But let’s stop to think for a second about why a dealership would offer you 0% financing. The reason is to make it more likely that you will buy the car or spend more on the car. We spend more when we spend with debt. You’re not immune to this. Doctors think they’re immune to the effects of drug reps peddling their wares, too. They’re not. Big Pharma execs aren’t stupid, and neither are car dealership owners. They wouldn’t keep doing this if it didn’t work at least most of the time. Plus, it’s awfully easy to just increase the cost of the car a little and then make it look like the 0% financing is a great deal when the overall deal is actually worse than it would be if everyone paid cash.

30-Year vs. 15-Year Mortgages

The length of mortgages gets debated all the time. Here’s an example:

“I don’t agree with your 30-year mortgage argument with a caveat. I could have done a 15-year mortgage and been fine. I chose a 30-year. I make extra payments so it’ll be a significantly less than [a] 30-year payoff, but [it] still gives me the flexibility should something happen to my income. In addition, it allows me to save much more for other events where I’ll be able to earn a higher return (the caveat). If you aren’t investing the saved money, then maybe stick to the 15-year.”

The 15-year gets you a lower interest rate and gets you out of debt more than a decade earlier. The 30-year mortgage provides a lower required payment and more flexibility. People REALLY don’t like to be told they made the wrong choice here, and so they will argue for longer than they should about their choice. But the truth is that most of the 30-year folks aren’t out of debt after 15 years, and many of the 15-year folks have the debt paid off long before the 15th year.

Anti-debt folks get 15-year mortgages. And they get rich. Probably not because of the 15-year mortgage but because they’re focused on building wealth. They buy cheaper houses. They put more money toward building wealth. They pay off debt faster. It’s more important to them. Classic Think and Grow Rich and The Millionaire Next Door mentality. Remember, personal finance is 90% personal (behavior) and 10% finance (math). People aren’t poor because they can’t do math.

More information here:

The Best Ways to Use Debt to Your Advantage

How to Use Leverage and the Differences Between Good and Bad Debt

Emergency Funds and Debt

I explained in the post that the point of an emergency fund is so that if there is an emergency, you can spend cash instead of borrowing money at 30%. But if you already have credit card debt at 30%, you already had the emergency. So, why do you still have the emergency fund? That wasn’t a popular thing to say. The WCI Forum responded this way:

“#1 Wait a second, you’re recommending not having an emergency fund until you are completely out of debt? I don’t know if I agree with that, nor do I think most financial people do. Doctors can lose jobs, doctors can still have unexpected large expenses, and disasters befall them. Even if you have insurance, it sometimes takes some time before they pay out.”

“#2 Sure you don’t have survivor bias? I didn’t have an emergency where I needed to tap my fund early in my career, but [I] know people who did. I really wouldn’t classify an e-fund as stupid.”

Somehow saying that to carry 30% credit card debt and have an emergency fund at the same time is illogical became “Jim Dahle hates emergency funds.” Not everybody had this reaction to that point in the post, though. One WCIer emailed me this:

“I want to thank you for everything you and your team have done for so many of us. I read yesterday’s email at the gym and realized it didn’t make sense to continue carrying student loans while holding a large emergency fund. I sent a $30,000 payment to my loan servicer and fully paid them off. We went out for a nice dinner afterward to celebrate—$300,000 in student loans gone in 4.5 years. I feel like a new man.”

I guess the post was worth rerunning, even with all the flak I took for it. And I’m sure this doc will rebuild that emergency fund within a few months, as he should.

5-Figure Car Loans Are Stupid

Perhaps my most controversial teaching about debt is that nobody should ever have a five-figure car loan. Since you can get reliable transportation for less than $10,000, it seems silly to buy something you can’t afford (and thus have to finance) when basic, reliable transportation is available for less. Here’s an example comment:

“For the car loan I’m not the best advocate for this since I haven’t had a car loan for several years, but I know some high-income people that have become multimillionaires and have really nice cars. And yes, they are on track to be able to retire in their late 40s [or] early 50s. That’s the benefit of high income. As long as you’re meeting your saving goals then I’m not going to say their loan is stupid.”

The truth is that if you make half a million dollars, you can make plenty of financial mistakes and still be fine. Most doctors can buy brand new cars with a car loan and still retire as financially independent multimillionaires. But that doesn’t change the fact that it’s still a dumb way to buy a car. If you can save up for a brand new car in 3-6 months, why not just do that? I mean, you make $20,000-$60,000 A FREAKING MONTH. How long should it take you to save up $50,000 for a car?

You really can’t wait that long for your next car? Fine, get the car loan. But when you pay it off (in 3-6 months), keep making payments into a side fund for your next car so you can pay cash next time. Even a doctor who uses a five-figure car loan shouldn’t have to do it twice. But what do I know? It’s not like I’ve been driving cars for 37 years, ranging from a literal Flintstones mobile with a wooden floor to a brand-new fancy Super Duty truck.

I’ve had one car loan in my life. As a senior college student. To my parents. At 0%. With no payments due until my first intern paychecks. For $3,000. Which I paid off in September of my intern year with one check. But if you want a car loan, knock yourself out. Just recognize that there are a whole bunch of us out here in WCI land who roll our eyes at you every time we walk through the doctor’s parking lot.

Die with Zero? Consumption Smoothing?

WCI columnist Rikki Racela asked this:

“Has Die with Zero changed your mind regarding keeping long-term debt especially at low interest rates? For example, I keep a 30-year mortgage at 2.9% fixed, even though, yes behaviorally, I don’t invest the money that I would’ve paid into a 15-year mortgage, I am using that money to buy experiences in my current season of life. Just came off of a Disney Cruise with the fam that [we] probably would not have been able to go on if I was doing a 15-year mortgage. My 15-year mortgage would’ve been paid off when my youngest would be going to college. Instead of investing in life experiences in that season of life, it would’ve gone to the bank just so I could say I am mortgage debt-free at the start of being an empty nester.

I’m a big fan of the Die with Zero philosophy. But I still think it’s wise to get rich before adopting it. Be rich before you start acting rich. Don’t forget what Bill Perkins said in the intro to the book:

“Just to be up front: if you’re struggling to make ends meet, you might get some value out of this book, but not nearly as much as someone with enough money, health, and free time to make real choices about how to put those resources to the greatest use.”

Yes, moderation in all things. But if you can’t skip a few years of work without any financial consequences, it’s probably not yet time to adopt the Die with Zero philosophy. You cannot justify all use of debt by saying “Die with Zero!” When it comes to a mortgage or whatever other financial goal, set a timeline for when you want to be done with it. Then, put the money toward what is required to meet that goal and spend the rest guilt-free.

Some People Don’t Understand How Cars Work

Some of the justifications for debt get kind of loony. Check out these three (from the same person):

“On car loans, I don’t necessarily agree that they’re a bad idea across the board. In certain situations, financing can actually be the more logical choice. For vehicles that depreciate quickly, using a low-interest, manufacturer-subsidized loan often makes more sense than tying up personal capital. I’d rather keep that money working elsewhere—something relatively conservative like first-position mortgage lending that can generate around 10% annually.

#1 The rate at which the vehicle depreciates has nothing to do with whether you should finance it.

#2 Paying off debt is risk-free. If you’re convinced you can successfully arbitrage low-interest-rate debt, you should compare the after-tax interest rate on the debt to the after-tax return on a risk-free investment, like a money market fund—not stocks or real estate (including debt real estate investments). There’s a reason debt real estate investments historically enjoy 10% long-term returns instead of 4% returns. It’s because risk exists there. As a general rule, higher yield means higher risk, even if you can’t identify the risk.

“There’s also the insurance angle. In a total-loss situation, insurance typically covers the value of the car or the remaining loan balance—not the cash you originally put down. From that standpoint, large down payments don’t always reduce risk and can sometimes increase it. For business owners, there’s also the added benefit of Section 179 expensing when the vehicle qualifies, which can materially change the math.”

Maybe this person has never totaled a paid-off car. I’ve done that three times in my life. Each time, the insurance company paid me THE PRE-COLLISION VALUE OF THE CAR, not the value of the non-existent loan or the down payment. If they didn’t, they’d be taken to court. And your business certainly doesn’t have to finance a car to deduct it as a business expense.

“Exotic or high-end cars are a separate category altogether. Many physicians enjoy driving special vehicles, and there is a financially responsible way to do it. Pulling $300,000 out of savings to buy a 911 Turbo S outright probably isn’t it. When financed properly, and when the car holds its value reasonably well, the true cost of ownership can be surprisingly modest—sometimes not very different from an ordinary car. Meanwhile, the capital stays invested and productive. This obviously doesn’t apply to every vehicle, but for the right ones, the strategy works.”

First, this person advocates for borrowing to buy a car when the car depreciates quickly. Then, this person turns around and advocates for borrowing to buy a car when the car doesn’t depreciate quickly. Basically, I think this person is in the car loan business. But the bottom line is this person is advocating to invest on margin. Fine, as discussed in our very nuanced “pillar post” on debt, a case can be made for doing that with an amount equal to 15%-35% of your assets if you need to take that risk to reach your goals. But don’t kid yourself that you’re going to buy that ’66 Corvette with a note and actually invest the money that would have gone toward it. You’re probably going to use that to buy a McLaren. And a larger garage to store them both. Or maybe just a bunch of diapers to rub them with.

I actually do agree that there is a financially responsible way to enjoy an exotic car. Rent it.

More information here:

I’m Leveraged to the Gills at Nearly $2 Million! Watch Me Swim

10 Reasons You’re Not Stupid for Paying Off Your Debt

Debt and Asset Protection

As much as I made fun of the person in the last section, this same person made some great comments about debt and asset protection worth discussing in this nuanced post.

“On home mortgages, I actually believe that maintaining a mortgage—especially for physicians—can be beneficial and, in some cases, protective. A fully paid-off home is one of the easiest assets to target in litigation. While insurance and umbrella policies are essential, they don’t eliminate risk, and real estate is immobile and easy to identify.”

Two comments about this. First, “hiding” assets isn’t a particularly useful asset protection technique. When you’re in a REAL asset protection situation, you get put on the stand, put under oath, and asked about your assets. Lying in this situation is a VERY bad idea. You go from having to worry about keeping all of your money to having to worry about how much time you will be spending in prison. In that respect, a paid-off home is hardly an asset protection mistake.

Second, this sort of thing is VERY state-dependent. In states with great homestead laws (think Texas and Florida), paying off a home is an EXCELLENT asset protection move. Even in states without great homestead laws, using Tenants by the Entirety (TBE) titling or placing the home in a Domestic Asset Protection Trust (DAPT) can also make paying off the mortgage a good asset protection move.

No surprise that this commenter who loves car loans also seems to love mortgages, I guess.

If you are somehow in one of the very few states that do not have a strong homestead law or TBE titling (or you’re not married) or DAPTs AND you’re really worried about asset protection, you can do what is called “equity-stripping.” Basically, every time you have more equity in your home than the homestead limit for your state, you refinance the home, take out that equity, and reinvest it in something that your state does protect in bankruptcy, like retirement accounts and possibly cash value life insurance or annuities.

But before doing this, you’ve really got to get your anxiety treated (above policy limits judgments are VERY rare) and make sure you’re in a state where this sort of technique will actually work/matter. Asset protection techniques often have a cost, but carrying an unnecessary mortgage might be one of the highest. An $800,000 mortgage at 6% costs $48,000 per year in interest. Sure, that’s reduced by whatever you can earn on that money, but considering you can get plenty of nice trusts for a one-time $15,000 payment, it seems silly to spend $48,000 EVERY FRIGGIN’ YEAR on asset protection.

But wait, there’s more.

“Regarding personal and business lines of credit, I think these are especially important for physicians in higher-risk specialties like surgery. Accounts receivable are among the easiest assets for creditors to go after. When those receivables are already pledged against a secured line of credit, they’re significantly better protected. This may not matter much for employed physicians, but for practice owners with large receivables, it’s an important consideration.”

Now, not only are we talking about equity-stripping for your home, but also for your practice. I used to worry a lot about asset protection. I thought I’d write about it plenty on the blog. Then, I learned more about it. I even wrote a book about it. Now, I don’t spend any time at all worrying about it. In fact, I still practice medicine despite having more assets exposed to creditors than I will earn the rest of my career practicing medicine. Yes, I’ve done a few things that boosted our asset protection that usually also made sense for other reasons. But I’m certainly not going to go into debt again in hopes of getting more asset protection.

This was a long post, as any post that includes a lot of nuance is going to be. And frankly, it’s your money and your life and your debt, so do what you want with it. You don’t have to answer to me or anybody else. But don’t be surprised when you hear people snickering as you try to justify your auto loans, 30-year mortgage, business debt, 0% credit cards, 20-year student loans, etc. They’re just thinking, “Oh, you have debt? How quaint. Bless your heart!”

What do you think? Should I be more pro-debt? Has debt been the best thing ever in your life? Let me have it in the comments section!