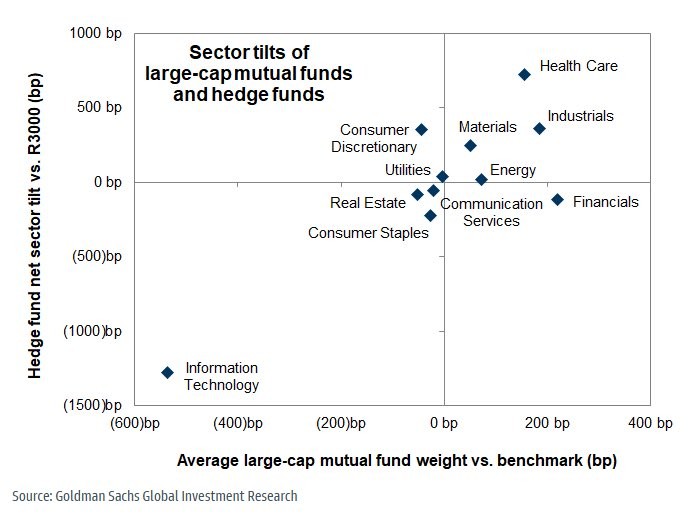

We have written a few Commentaries over the last year describing how retail, not institutional, investors are driving markets higher. To wit, there is ample evidence that with each market dip, retail investors are not selling, instead buying unrelentingly. In May, we wrote the following: Typically, institutional investors are right; however, over the last few years, retail has proven to be the smarter money. However, it’s worth considering that if retail investors are still the “dumb money” and professionals the “smart money”, the graph below has significant implications.

The scatter plot from Goldman Sachs shows the average sector weightings of large-cap mutual funds and hedge funds, i.e., institutional investors, versus how the sectors are weighted in the broad Russell 3000 index. As shown, the “smart money” is most enthusiastic about the healthcare and industrials sectors. Healthcare valuations are trading at 20-year lows versus the S&P 500, as investors have shunned some value sectors. Instead, the Magnificent Seven, high-growth technology, crypto-related companies, and power grid infrastructure stocks have garnered the most investment flows. Despite the popularity of technology stocks, both hedge funds and mutual funds are holding less than the market weights in the technology sector.

More simply, retail is exceedingly enthusiastic about technology and not biting on cheap healthcare valuations. At the same time, as we show, professionals are shunning technology in favor of healthcare. Again, we must ask – Smart Money or Dumb Money: Who Will be Right:

What To Watch Today

What To Watch Today

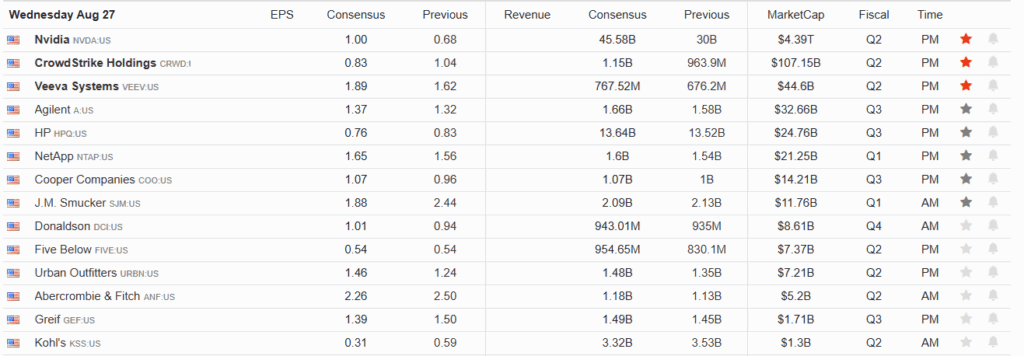

Earnings

Economy

No notable economic releases today Market Trading Update

As noted in yesterday’s commentary, everyone is awaiting Nvidia’s earnings report today, which will come after the bell. Current estimates are wildly optimistic, which leaves a substantial amount of “disappointment risk” given where Nvidia is currently trading.

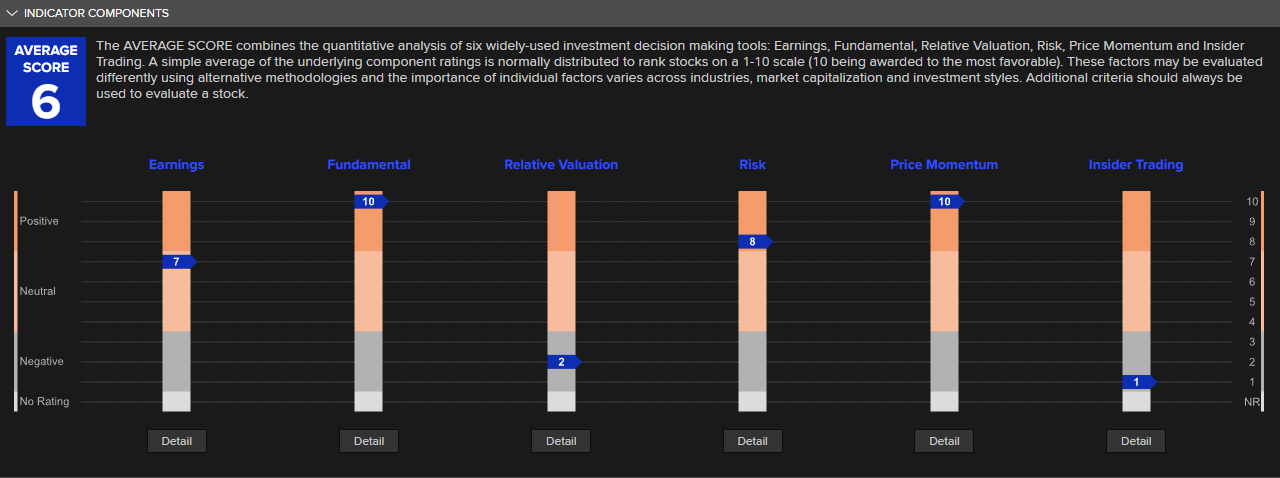

One reason we are a bit cautious heading into earnings today is that insider trading has been very muted. While not an “absolute” indication, it is worth considering that if earnings are as good as Wall Street expects, should there not have been more insider buying before the “blackout” period started?

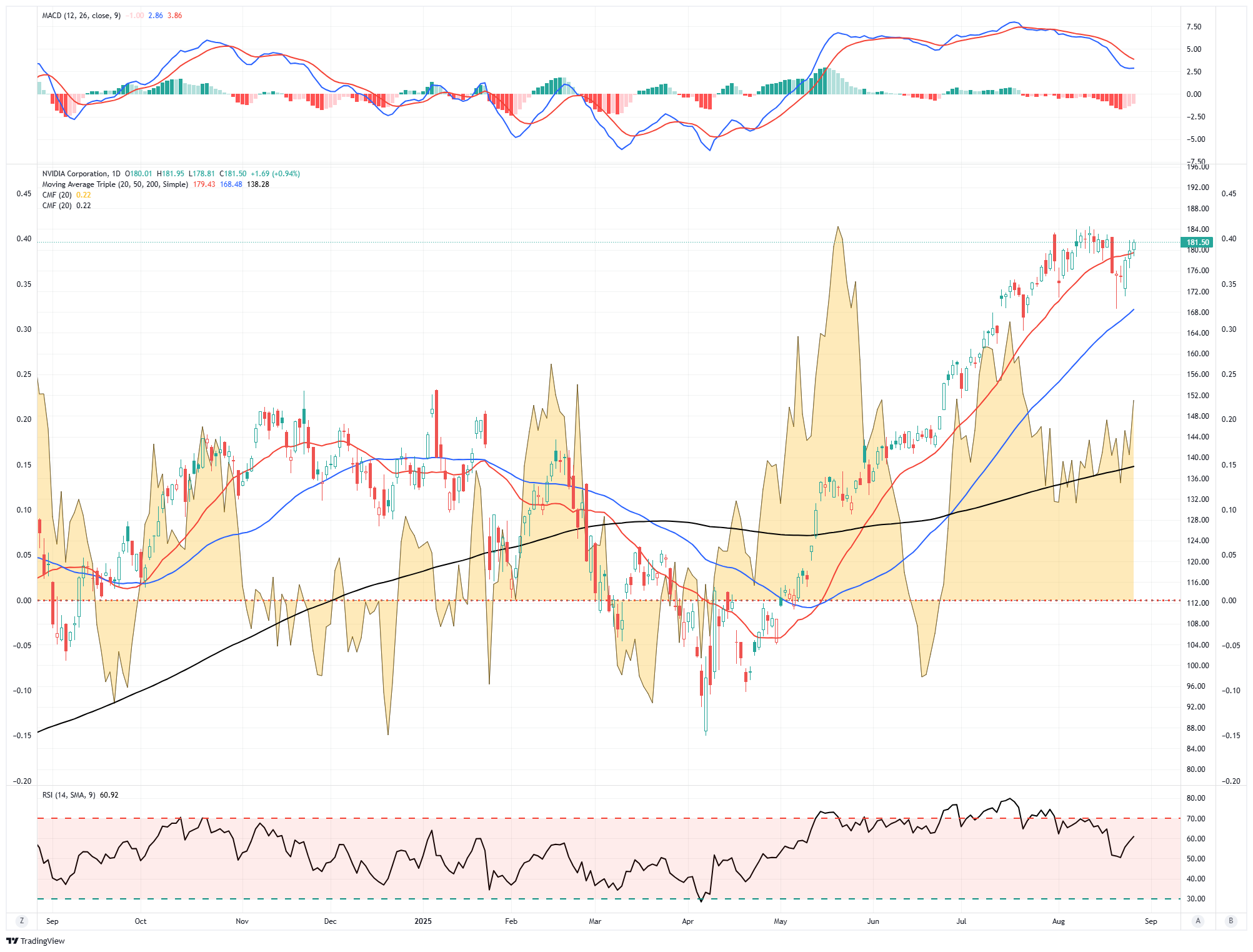

Technically, there are also a couple of warning signs. Money flows are neutral, and momentum and relative strength are declining. Again, these are not flashing a major warning, but are concerning heading into such a critical report, given the market’s dependence on “all things Nvidia” relative to the artificial intelligence chase.

Heading into today’s earnings report, we recommend hedging your position somewhat. Take some profits and rebalance to target weights, raise some additional cash, and potentially reduce exposure to highly correlated pair trades like Broadcom (AVGO).

Nonetheless, I am anxious to see their report and how the market reacts after the announcement.

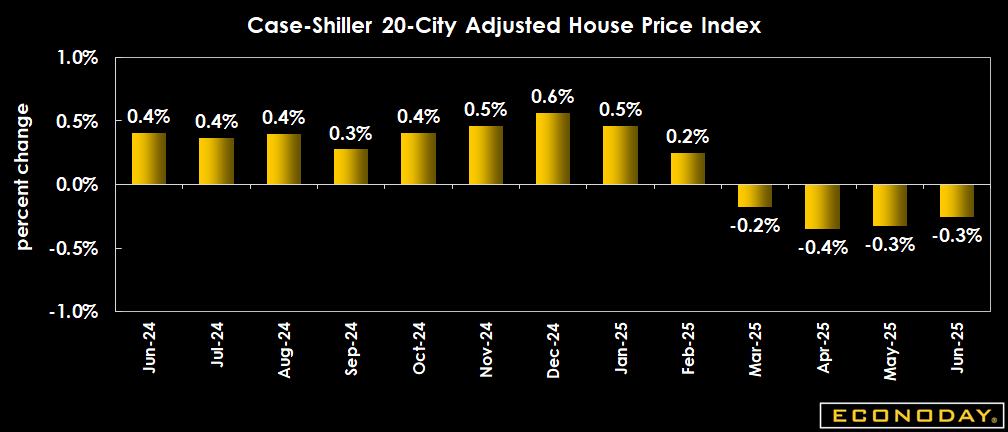

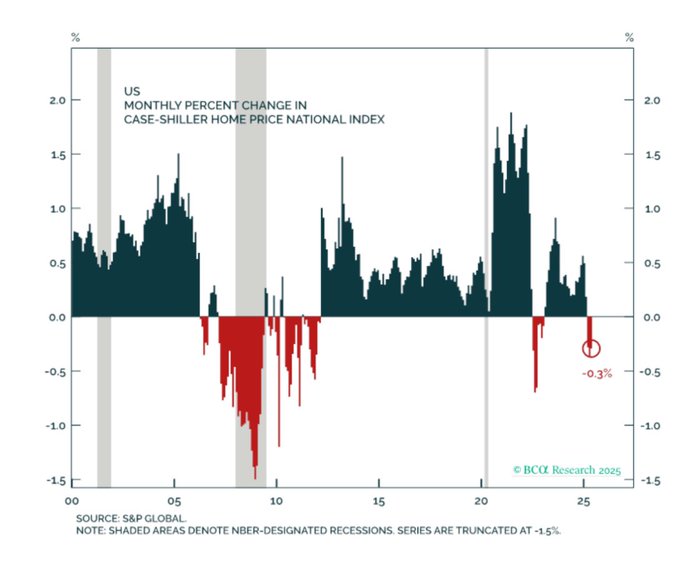

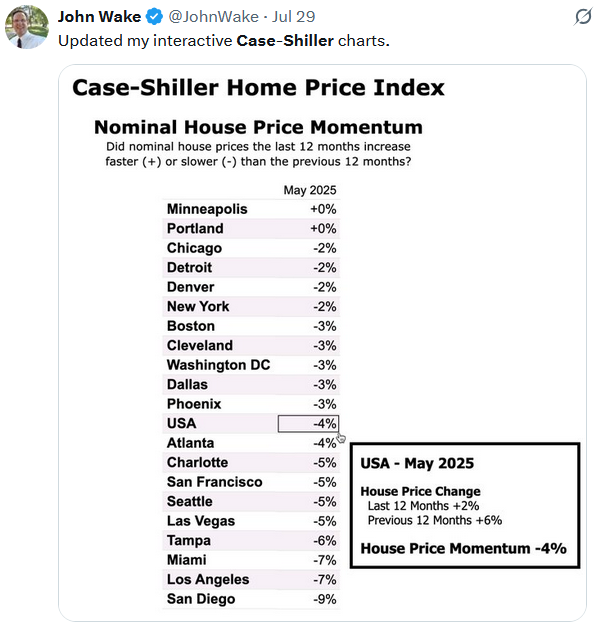

Home Prices Weaken Furthering Arguments For A Rate Cut

Home Prices Weaken Furthering Arguments For A Rate Cut

The well-followed Case-Shiller 20-city house price index fell for the fourth month in a row. With the latest data, national home prices are up a mere 2.14% on a year-over-year basis. Interestingly, those cities that have been lagging in home price increases, like Chicago and New York, saw gains of 6% and 7%, year over year, respectively. Conversely, the “hot” markets like Tampa, Phoenix, Denver, and Dallas are all reporting negative price changes over the last year. As the second graph below shows, price declines are somewhat rare. The only two prior instances were before and during the 2008 Financial Crisis and shortly after the steep run during the pandemic.

The data is very important for Fed policy for two reasons. First, home prices contribute to shelter prices, which account for about 40% of CPI. Given that CPI still shows shelter prices rising by about 4% annually, while rental prices are flat to falling and home prices are declining, this will exert negative pressure on CPI to counter tariffs. Second, housing-related activity contributes about 15% to GDP. Given that housing is weakening inflation and dampening the economy, the recent Case-Shiller home price data should provide further rationale for the Fed to cut rates.

How To Build A Wealth Management Plan

How To Build A Wealth Management Plan

Most of us start financial planning with a basic idea: save, invest, and retire comfortably. But what happens when life throws something big your way, good or bad?

Maybe you will sell your business sooner than expected. Maybe you receive an inheritance. Perhaps life takes a sharp left turn through divorce, or you decide to retire early to chase a lifelong dream.

Moments like these are emotional financial pivots. And when they happen, your wealth management plan needs to evolve with you.

At RIA Advisors, we believe your financial strategy should never be static. It should grow, flex, and respond to your life. Here’s how you can build an adaptable financial plan that stays aligned with your goals. No matter what life brings next.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.