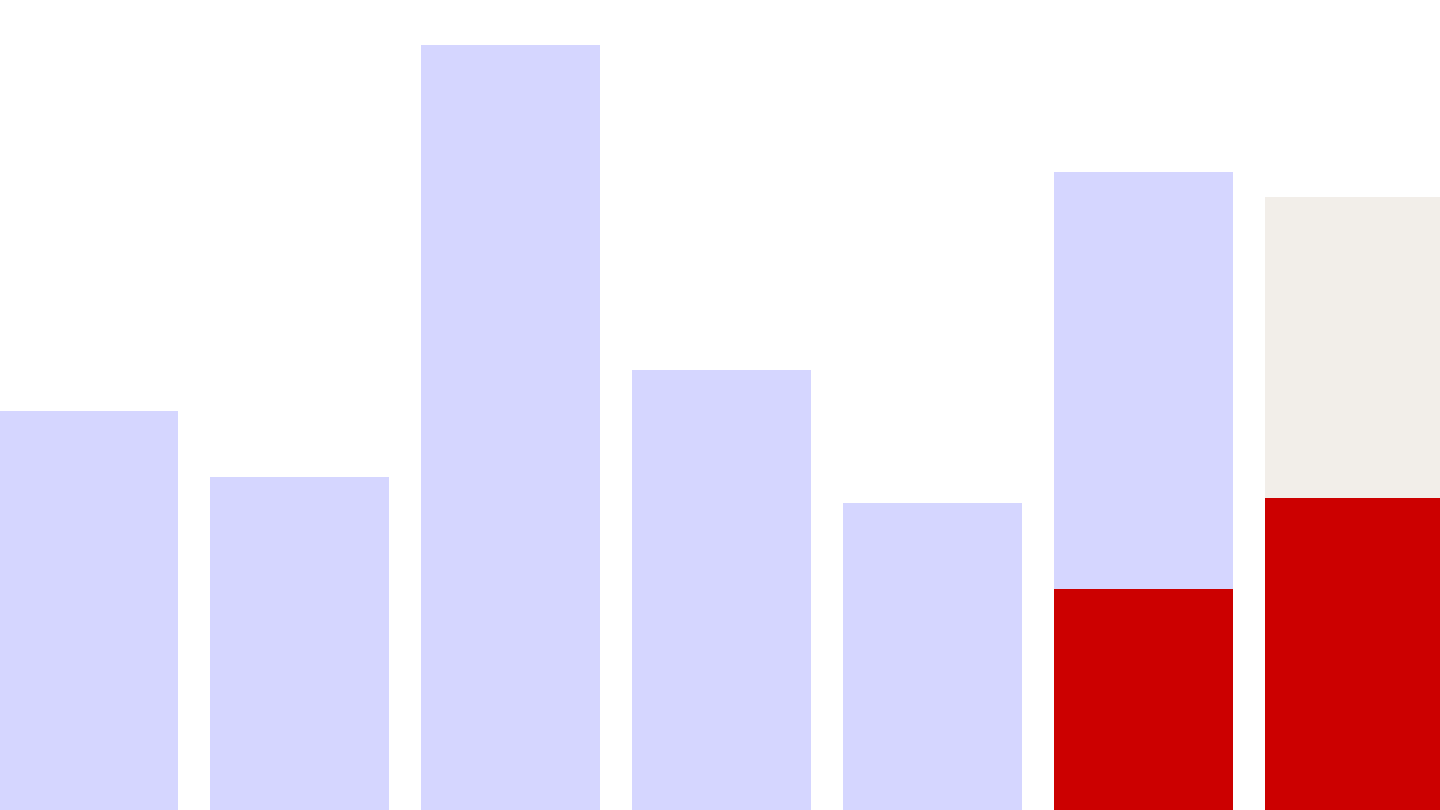

In the first half of 2025, global healthcare buyout deal value fell slightly below 2024 on an annualized basis. The second quarter in particular saw a drop in value, which was most pronounced in medical technology and biopharma. Still, deal value was higher compared with the first half of 2024.

Regionally, North America was weaker than during the same period a year earlier. In Asia-Pacific, deal volume in India was buoyed by major provider deals, and Japan hosted large carve-outs. Growth slowed in many other Asia-Pacific countries. By contrast, dealmaking in Europe has more or less held steady throughout the past six quarters.

Turning to healthcare IT companies, the recent surge in deals stems from three factors: several gem asset processes commanding high multiples, a flight to assets insulated from public policy, and the applicability of artificial intelligence.

We see a strong case for optimism in the third quarter, based first on the fact that large deals are already transacting. In addition, several delayed transactions could return to the market. Finally, many long-dated assets and ample dry powder remain in play.