📈The stock market rallied to all-time highs, with the S&P 500 setting an intraday high of 6,671.82 and a closing high of 6,664.36 on Friday. The index is now up 13.3% year-to-date. For more on the market, read: The stock market and the economy are diverging 📊

–

With almost three quarters of 2025 in the rear-view mirror, market participants are increasingly shifting their focus toward 2026.

“As we met with a variety of US equity investors last week — ranging from hedge funds to high-net-worth retail, from high-level macro investors to stock pickers, and everything in between — it became clear to us that it’s time to start talking more about 2026,” RBC Capital Markets’ Lori Calvasina said Monday.

She preliminarily sees the S&P 500 ending 2026 at 7,100 as earnings per share (EPS) grow about 10% to $297. (For more on how to think about year-end targets, read: A better way of thinking about Wall Street’s year-end price targets 🗺️)

Her projections are derived from a blend of five models that factor in almost every imaginable macro variable.

But one assumption caught my attention.

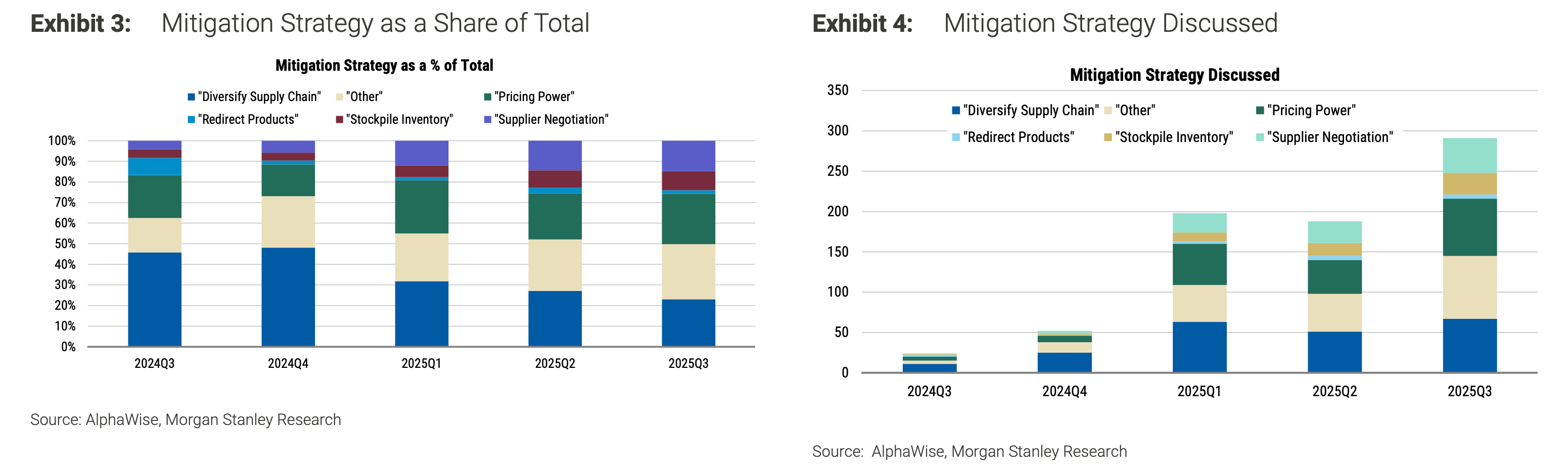

“We are baking in some margin expansion for 2026,” she wrote. On the subject of profit margins, she added, “One of our biggest takeaways from 2Q25 reporting season is that companies are laser focused on mitigation strategies around tariffs.“

This is in line with Morgan Stanley’s analysis of Q2 earnings calls: “Unsurprisingly, we saw a significant increase in the number of mentions of tariff mitigation strategies last quarter with many companies citing multiple strategies.“

Executives are focused on mitigating costs associated with new tariffs. (Source: Morgan Stanley via TKer)

Executives are focused on mitigating costs associated with new tariffs. (Source: Morgan Stanley via TKer)

And it’s not just tariff mitigation that could bolster profit margins in the quarters to come.

“Drivers for margin strength include operating leverage, continued efficiency gains (AI and others), slowing employment inflation in many labor-intensive sectors, and the potential for cost-cutting from deregulation,” BofA’s Savita Subramanian wrote Wednesday.

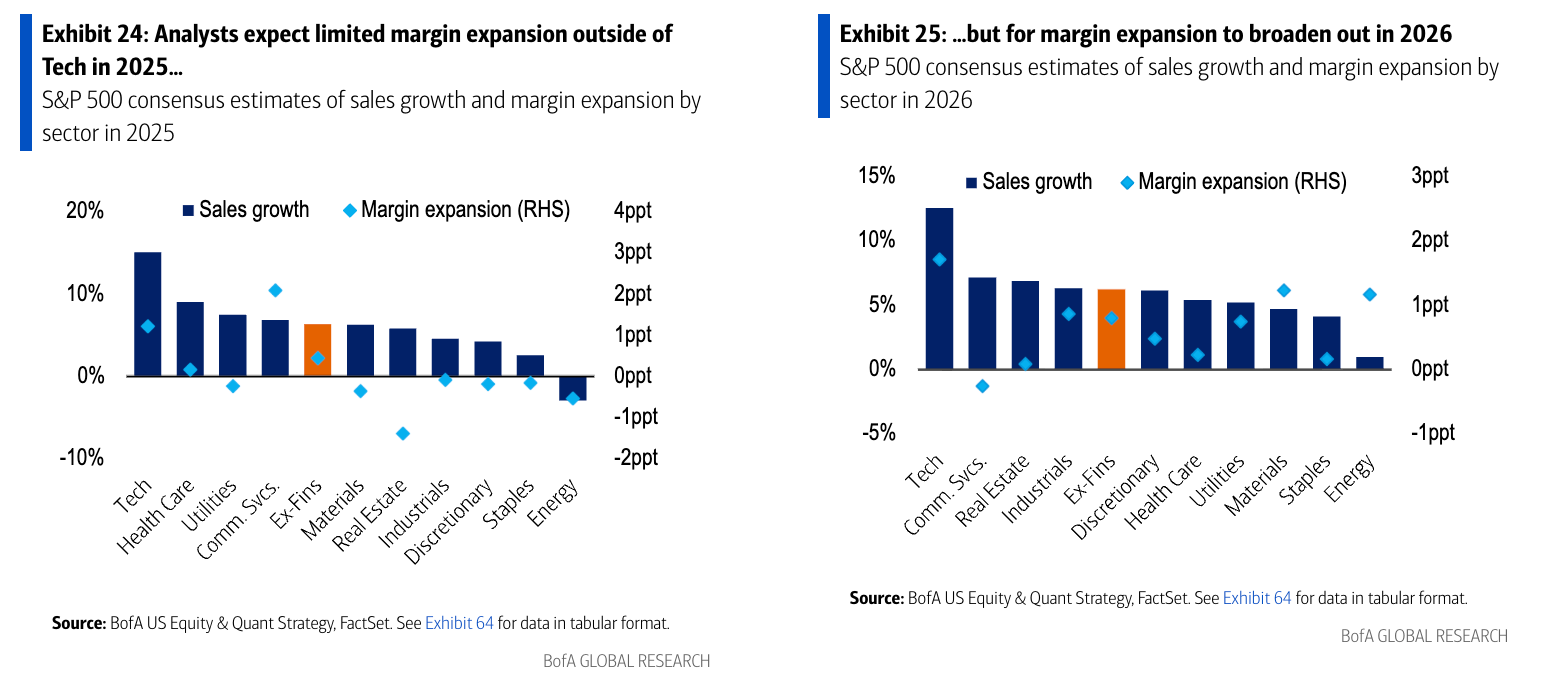

While margin expansion in 2025 has mostly been driven by big tech companies, that growth is expected to broaden out across industries in 2026.

Profit margins are expected to expand in more industries next year. (Source: BofA)

Profit margins are expected to expand in more industries next year. (Source: BofA)

Subramanian expects EPS to grow about 10% to $298 in 2026 as net margins increase by 40 basis points to 13.2%. She has yet to offer a 2026 price target for the S&P 500.

Goldman Sachs also has yet to publish forecasts for 2026. (These calls typically come later in Q4.) However, they have been discussing the prospects for growth in profit margins.

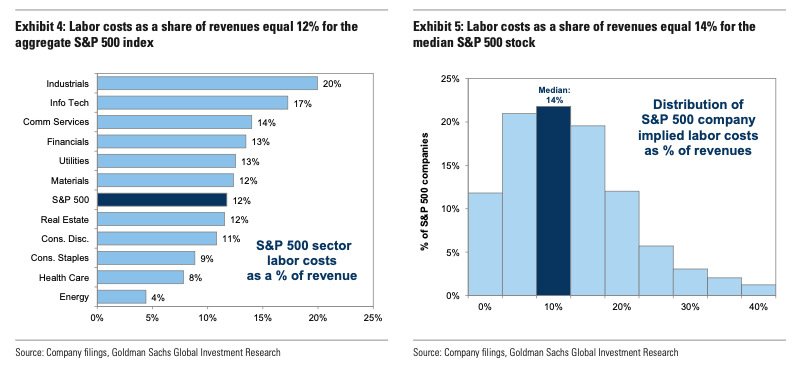

“[A] cooling labor market is a tailwind to corporate profits, all else equal,” Goldman Sachs’ David Kostin wrote in a Sept. 12 note.

Labor represents a significant cost across industries. (Source: Goldman Sachs)

Labor represents a significant cost across industries. (Source: Goldman Sachs)

“Profit margins typically expand when companies can raise prices more quickly than materials input and labor costs,” Kostin said. “Our economists expect the U.S. economy will continue to expand in 2H 2025 and 2026, but slow job growth will keep a lid on wage growth.”

Indeed, with the economy cooling, workers don’t have as much leverage as they used to to push for a raise.

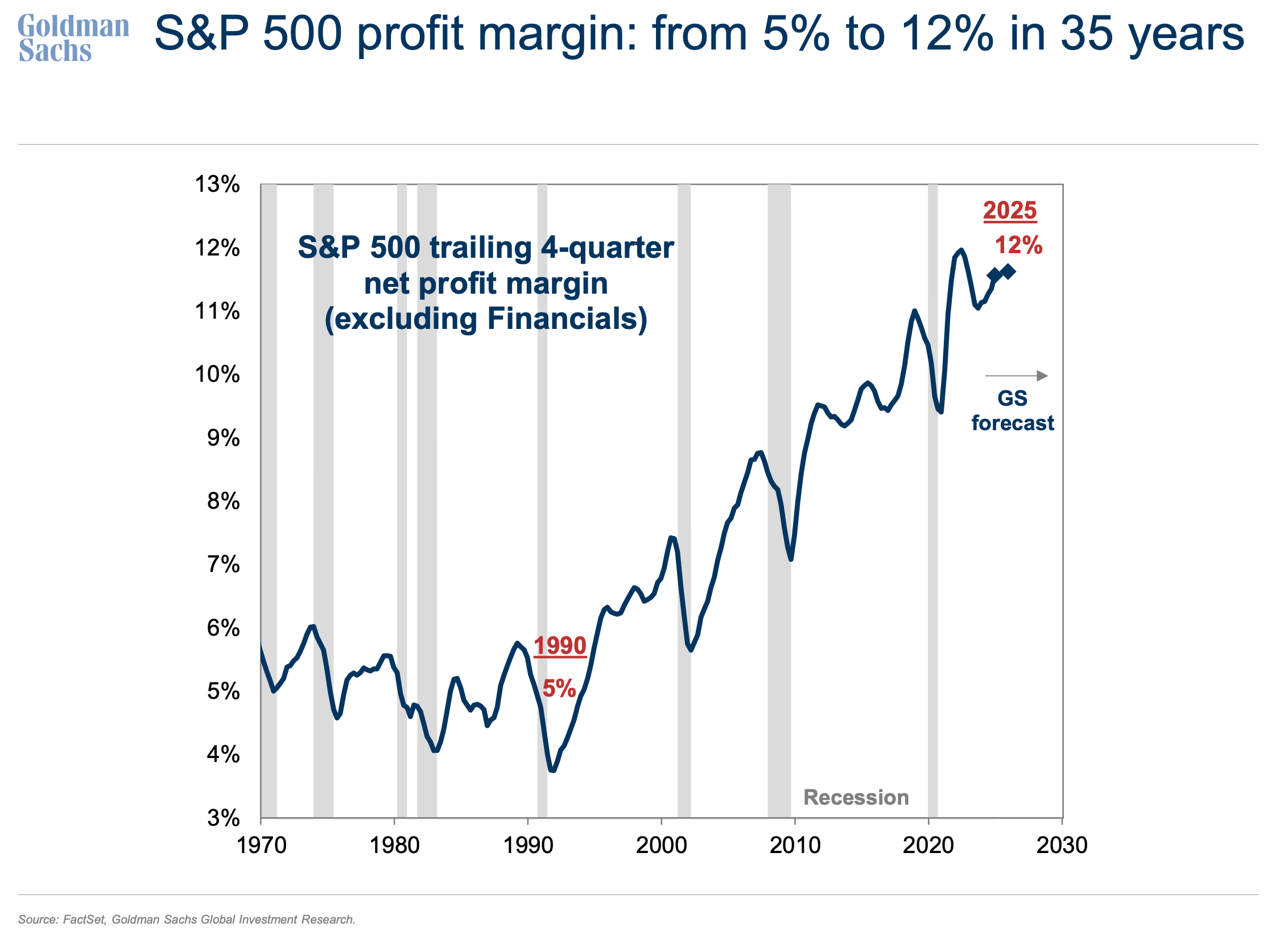

In what’s arguably been the most surprising business development of the current economic cycle, profit margins remained historically high throughout 2021, 2022, 2023, 2024, and, so far, 2025. And now analysts expect margins to expand in 2026 (and 2027!).

Profit margins remain historically high. (Source: Goldman Sachs)

Profit margins remain historically high. (Source: Goldman Sachs)

Whether it was supply chain disruptions, hot inflation, tight monetary policy, or the threat of higher tariffs, Corporate America has successfully navigated the treacherous cost environment to maintain historically high profit margins and generate record-high earnings.

Can this trend really persist? We’ll see.

But for now, the case for high profit margins looks strong, supported by recent years of success.

–

Related from TKer:

I was on the Excess Returns podcast with Matt Zeigler and Kai Wu. We discussed TKer’s 10 Truths About the Stock Market and how investors can apply them to make sense of the markets today. Check it out on Apple Podcasts, Spotify, or YouTube!

There were several notable data points and macroeconomic developments since our last review:

✂️ Fed cuts rates. The Federal Reserve announced its first interest rate cut since December 2024. On Wednesday, the Fed lowered its benchmark interest rate target range to 4% to 4.25%, down from 4.25% to 4.5%.

From the Fed’s policy statement: “Recent indicators suggest that growth of economic activity moderated in the first half of the year. Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated. The Committee seeks to achieve maximum employment and inflation at the rate of 2% over the longer run. Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate and judges that downside risks to employment have risen.“

The committee raised its projections for GDP growth while lowering them for unemployment. It also signaled that more rate cuts would come this year and next.

For more on what Fed policy could mean for markets, read: About Fed rate cuts and stocks ⚖️

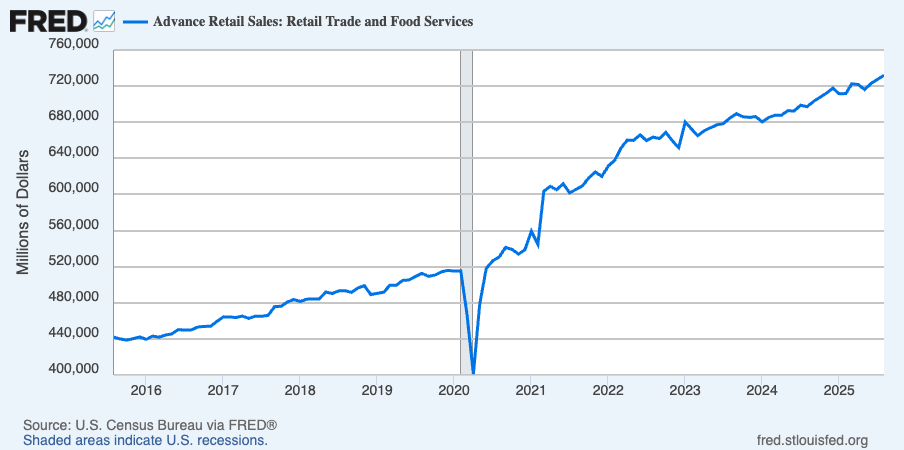

🛍️ Shopping ticks higher. Retail sales increased 0.6% in August to a record $732 billion.

(Source: Census via FRED)

(Source: Census via FRED)

Most categories saw growth.

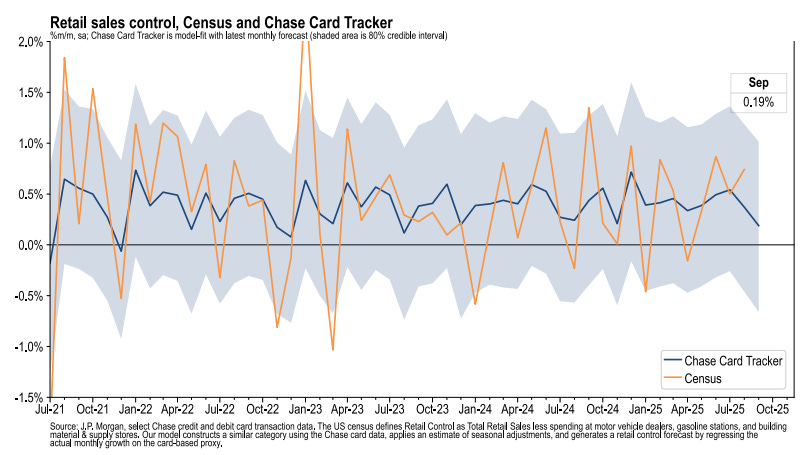

💳 Card spending data is holding up. From JPMorgan: “As of 12 Sep 2025, our Chase Consumer Card spending data (unadjusted) was 3.4% above the same day last year. Based on the Chase Consumer Card data through 12 Sep 2025, our estimate of the US Census September control measure of retail sales m/m is 0.19%.”

(Source: JPMorgan)

(Source: JPMorgan)

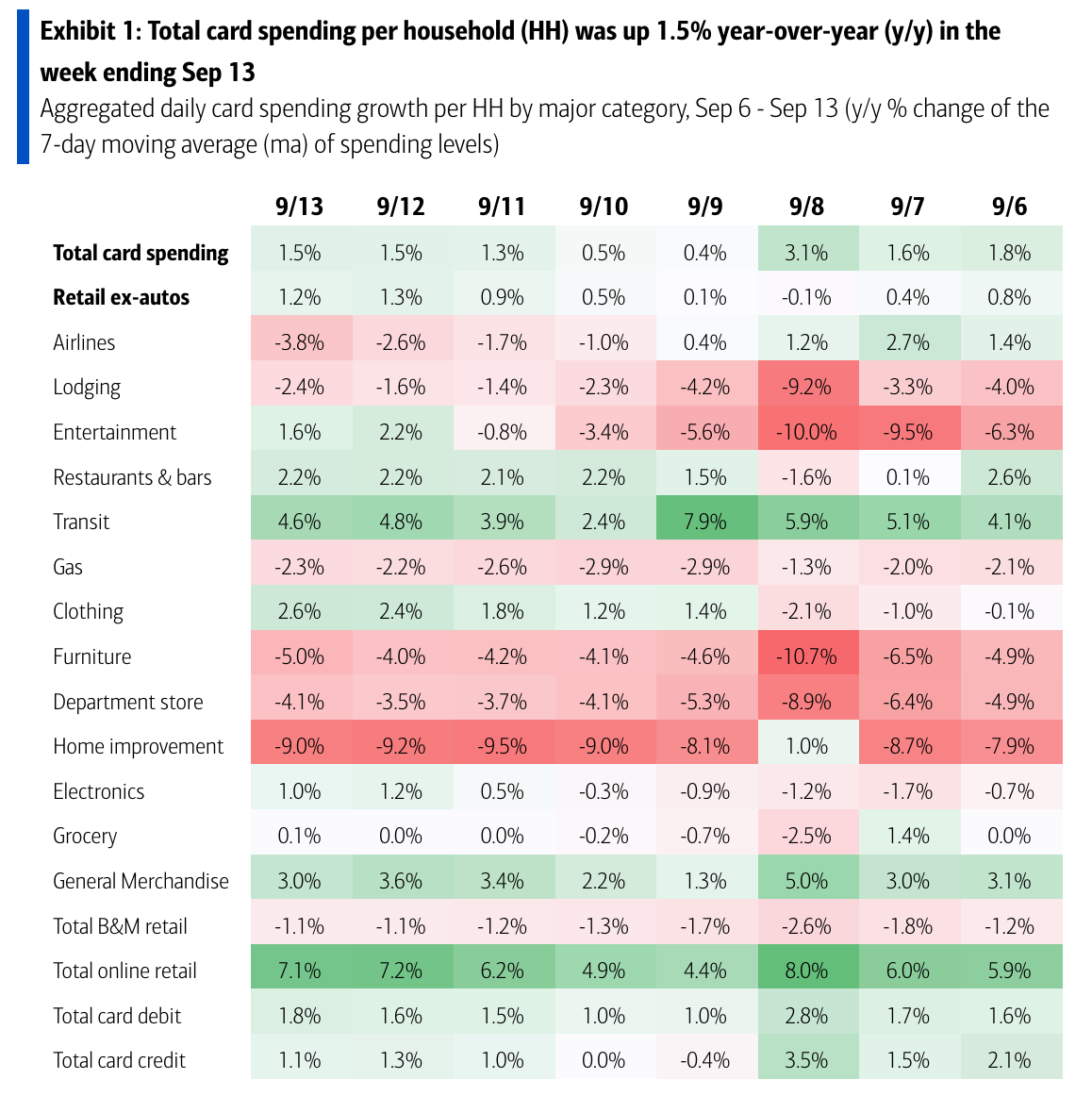

From BofA: “Total card spending per HH was up 1.5% y/y in the week ending Sep 13, according to BAC aggregated credit & debit card data. In our sectors, y/y spending growth in entertainment saw the biggest rise since last week & airlines saw the biggest decline. After strong Aug retail sales, BAC card data on spending looks stable in Sep, in line with our call for a consumer rebound.“

For discussion on how sales may be inflated due to tariffs, read: A BIG economic question right now 🤔

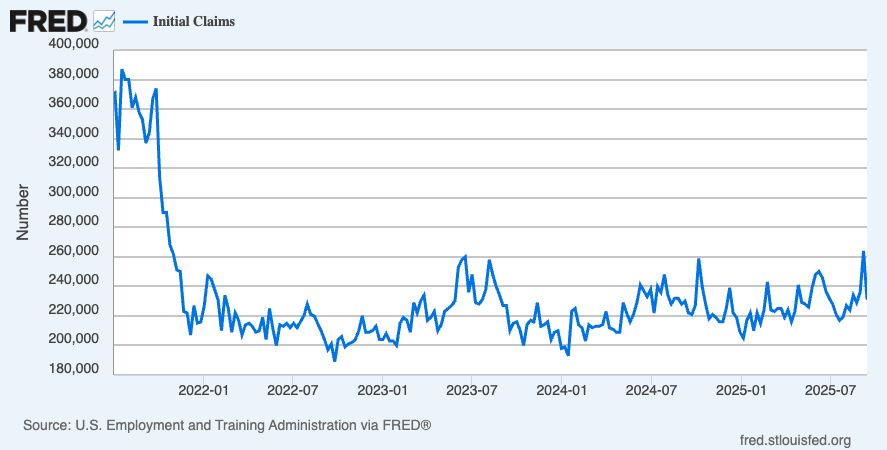

💼 New unemployment claims fall, total ongoing claims remain elevated. Initial claims for unemployment benefits declined to 231,000 during the week ending Sept. 13, down from 264,000 the week prior. This metric remains at levels historically associated with economic growth.

(Source: DOL via FRED)

(Source: DOL via FRED)

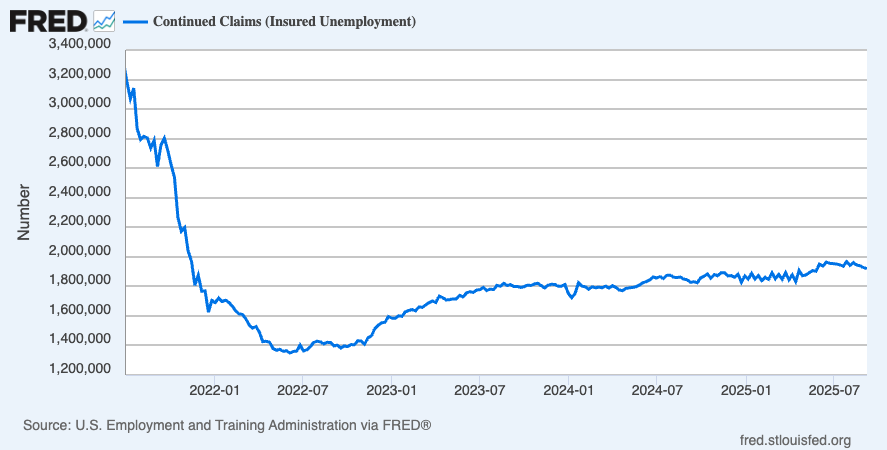

Insured unemployment, which captures those who continue to claim unemployment benefits, declined to 1.92 million during the week ending September 6. This metric is near its highest level since November 2021.

(Source: DOL via FRED)

(Source: DOL via FRED)

Low initial claims confirm that layoff activity remains low. Elevated continued claims confirm hiring activity is weakening. This dynamic warrants close attention, as it reflects a deteriorating labor market.

For more context, read: The hiring situation 🧩 and The labor market is cooling 💼

🛠️ Industrial activity ticks higher. Industrial production activity in August increased 0.1% from the prior month’s levels. Manufacturing output rose 0.2%. From the Federal Reserve: “Within manufacturing, the production of motor vehicles and parts increased 2.6% in August, while factory output elsewhere edged up 0.1%. The index for mining moved up 0.9%, and the index for utilities decreased 2.0%.“

⛽️ Gas prices tick higher. From AAA: “Pacific Northwest drivers, who already pay some of the highest gas prices in the country, saw their state averages surge this past week. A pipeline outage caused a spike in fuel prices in Oregon and Washington. Up until today, Washington was the state with the most expensive gas for several days, surpassing California, which is bracing for hikes of its own. Refinery maintenance this fall is expected to lead to decreased production and higher gas prices in the Golden State. Meanwhile, the national average for a gallon of regular went up a penny since last week to $3.20. Even though West Coast drivers are feeling pain at the pump, prices remain relatively low in the Plains and the South.”

For more on energy prices, read: Higher oil prices meant something different in the past 🛢️

🏠 Mortgage rates tick lower. According to Freddie Mac, the average 30-year fixed-rate mortgage stood at 6.26%, down from 6.35% last week: “Mortgage rates decreased yet again this week, prompting many homeowners to refinance. In fact, the share of mortgage applications that were refinances reached nearly 60%, the highest since January 2022.”

There are 147.9 million housing units in the U.S., of which 86.1 million are owner-occupied and about 39% are mortgage-free. Of those carrying mortgage debt, almost all have fixed-rate mortgages, and most of those mortgages have rates that were locked in before rates surged from 2021 lows. All of this is to say: Most homeowners are not particularly sensitive to the small weekly movements in home prices or mortgage rates.

For more on mortgages and home prices, read: Why home prices and rents are creating all sorts of confusion about inflation 😖

🏠 Homebuilder sentiment remains in the dumps. From the NAHB: “NAHB expects the Fed to cut the federal funds rate at their meeting this week, which will help lower interest rates for builder and developer loans. Moreover, the 30-year fixed rate mortgage average is down 23 basis points over the past four weeks to 6.35%, per Freddie Mac. This is the lowest level since mid-October of last year and a positive sign for future housing demand.”

🔨 New home construction starts fall. Housing starts declined 8.5% in August to an annualized rate of 1.31 million units, according to the Census Bureau. Building permits ticked down 3.7% to an annualized rate of 1.31 million units.

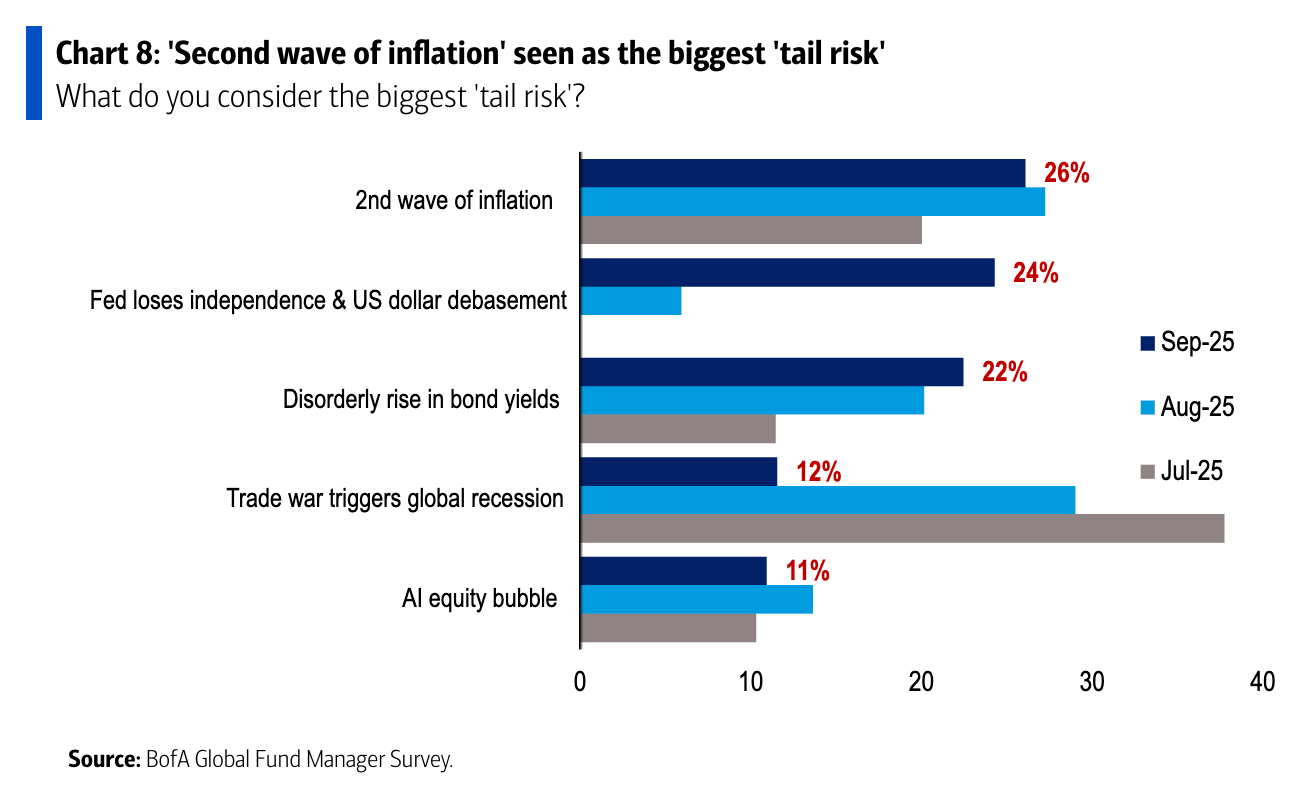

😬 This is the stuff pros are worried about. From BofA’s September Global Fund Manager Survey: “26% of FMS investors view a 2nd wave of inflation as the biggest tail risk, followed by 24% saying ‘Fed loses independence & US dollar debasement’ is the biggest tail risk. Trade war risk is fading with just 12% of investors saying ‘trade war triggering global recession’ is the biggest tail risk (down from #1 spot at 29% in August).”

(Source: BofA)

(Source: BofA) (Source: BofA)

(Source: BofA)

For more on risks, read: Three observations about uncertainty in the markets 😟 and Two times when uncertainty seemed low and confidence was high 🌈

🏢 Offices remain relatively empty. From Kastle Systems: “Peak day office occupancy was 65.3% on Tuesday last week, up 5.6 points from the previous week, as workers returned to the office in record numbers in the first full week after the Labor Day holiday weekend. New York City and Washington, D.C. experienced post-pandemic record-high Tuesday occupancy, rising 10.7 points to 71.8% and 5.1 points to 64.1%, respectively. Occupancy increased every day in nearly every city, which is a similar pattern to previous years as the summer travel season ends. The average low was on Friday at 36.9%, up more than six points from last week.”

For more on office occupancy, read: This stat about offices reminds us things are far from normal 🏢

📈 Near-term GDP growth estimates are tracking positively. The Atlanta Fed’s GDPNow model sees real GDP growth rising at a 3.3% rate in Q3.

For more on GDP and the economy, read: 9 once-hot economic charts that cooled 📉 and We’re at an economic tipping point ⚖️

💰 Stock buybacks are high, but the level is close to average. From S&P Dow Jones Indices’ Howard Silverblatt: “Q2 2025 share repurchases were $234.6 billion, down 20.1% from Q1 2025’s record $293.5 billion expenditure, and down 0.6% from Q2 2024’s $235.9 billion. For the 12-month June 2025 period buybacks were $997.8 billion, up from $877.5 billion from the prior 12-month period; the 12-month peak was in June 2022 with $1.005 trillion.”

“Buybacks as a percentage of market value decreased to 0.447% from 0.575% in Q1 2025; the historical average (from Q1 1998) is 0.635%,” Silverblatt said.

For more on stock buybacks, read: Companies are waiting longer before going public 👴🏼 and Eye-popping, headline-grabbing market stats often aren’t as extreme as they seem 🤦🏻♂️

🚨 The Trump administration’s pursuit of tariffs is disrupting global trade, with significant implications for the U.S. economy, corporate earnings, and the stock market. Until we get more clarity, here’s where things stand:

Earnings look bullish: The long-term outlook for the stock market remains favorable, bolstered by expectations for years of earnings growth. And earnings are the most important driver of stock prices.

Demand is positive: Demand for goods and services remains positive, supported by healthy consumer and business balance sheets. Job creation, although cooling, also remains positive, and the Federal Reserve — having resolved the inflation crisis — shifted its focus toward supporting the labor market.

But growth is cooling: While the economy remains healthy, growth has normalized from much hotter levels earlier in the cycle. The economy is less “coiled” these days as major tailwinds like excess job openings and core capex orders have faded. It has become harder to argue that growth is destiny.

Actions speak louder than words: We are in an odd period, given that the hard economic data decoupled from the soft sentiment-oriented data. Consumer and business sentiment has been relatively poor, even as tangible consumer and business activity continues to grow and trend at record levels. From an investor’s perspective, what matters is that the hard economic data continues to hold up.

Stocks are not the economy: There’s a case to be made that the U.S. stock market could outperform the U.S. economy in the near term, thanks largely to positive operating leverage. Since the pandemic, companies have aggressively adjusted their cost structures. This came with strategic layoffs and investment in new equipment, including hardware powered by AI. These moves are resulting in positive operating leverage, which means a modest amount of sales growth — in the cooling economy — is translating to robust earnings growth.

Mind the ever-present risks: Of course, we should not get complacent. There will always be risks to worry about, such as U.S. political uncertainty, geopolitical turmoil, energy price volatility, and cyber attacks. There are also the dreaded unknowns. Any of these risks can flare up and spark short-term volatility in the markets.

Investing is never a smooth ride: There’s also the harsh reality that economic recessions and bear markets are developments that all long-term investors should expect as they build wealth in the markets. Always keep your stock market seat belts fastened.

Think long-term: For now, there’s no reason to believe there’ll be a challenge that the economy and the markets won’t be able to overcome over time. The long game remains undefeated, and it’s a streak that long-term investors can expect to continue.

For more on how the macro story is evolving, check out the previous review of the macro crosscurrents. »

Here’s a roundup of some of TKer’s most talked-about paid and free newsletters about the stock market. All of the headlines are hyperlinked to the archived pieces.

The stock market can be an intimidating place: It’s real money on the line, there’s an overwhelming amount of information, and people have lost fortunes in it very quickly. But it’s also a place where thoughtful investors have long accumulated a lot of wealth. The primary difference between those two outlooks is related to misconceptions about the stock market that can lead people to make poor investment decisions.

Passive investing is a concept usually associated with buying and holding a fund that tracks an index. And no passive investment strategy has attracted as much attention as buying an S&P 500 index fund. However, the S&P 500 — an index of 500 of the largest U.S. companies — is anything but a static set of 500 stocks.

(Source: S&P Dow Jones indices via TKer)

(Source: S&P Dow Jones indices via TKer)

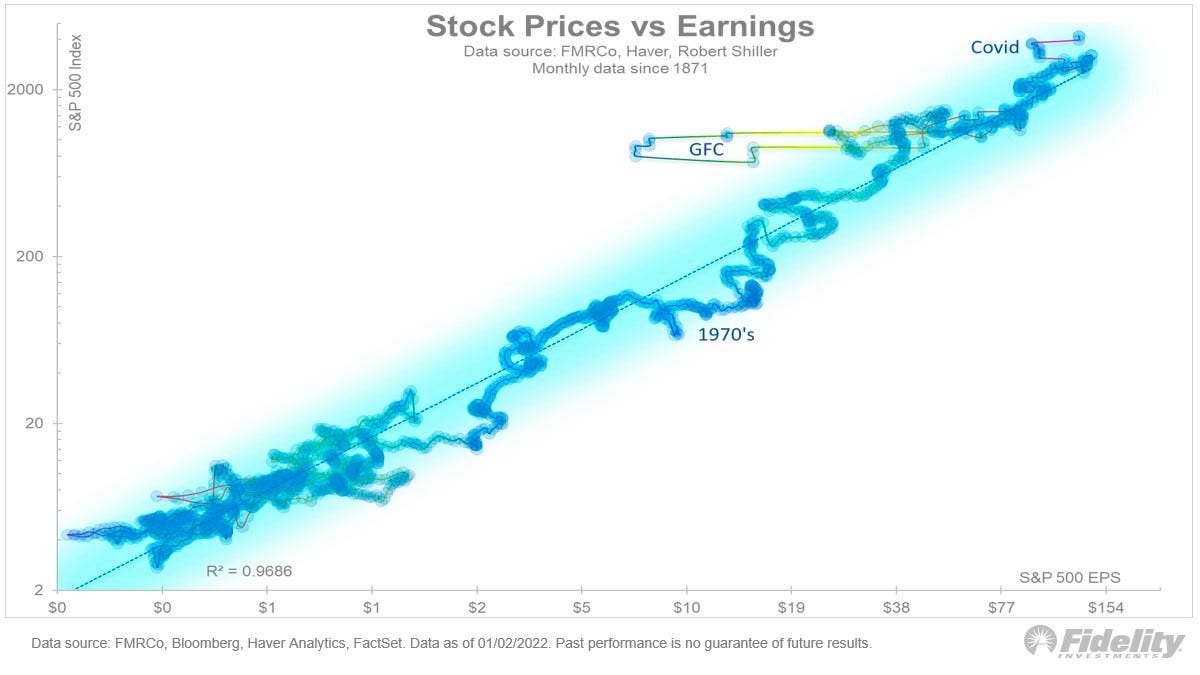

For investors, anything you can ever learn about a company matters only if it also tells you something about earnings. That’s because long-term moves in a stock can ultimately be explained by the underlying company’s earnings, expectations for earnings, and uncertainty about those expectations for earnings. Over time, the relationship between stock prices and earnings has a very tight statistical relationship.

(Source: Fidelity via TKer)

(Source: Fidelity via TKer)

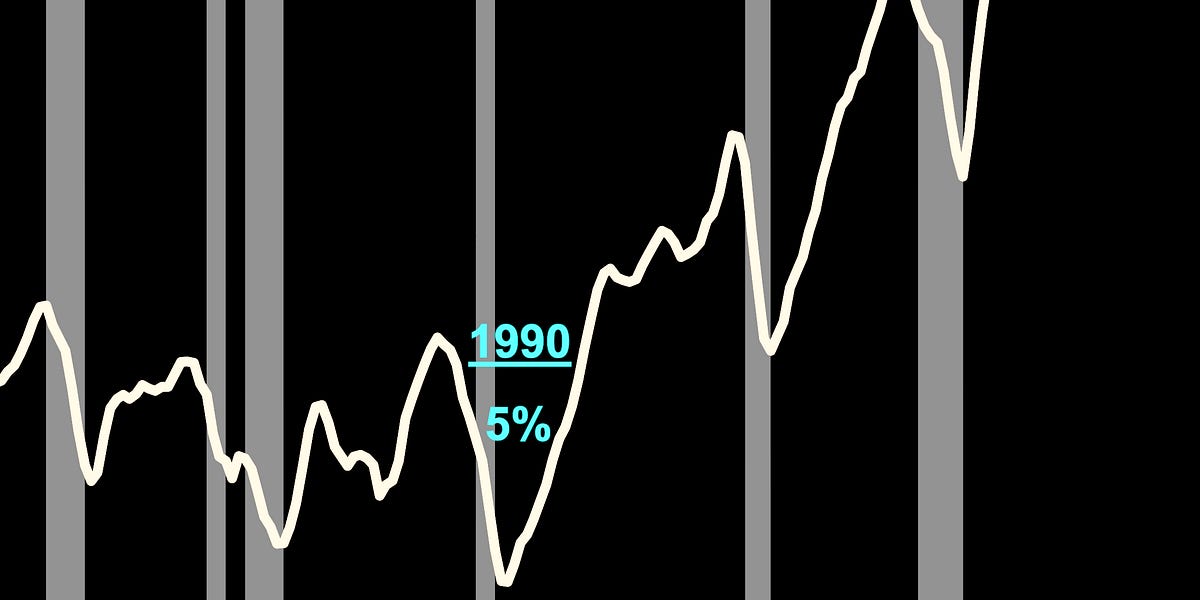

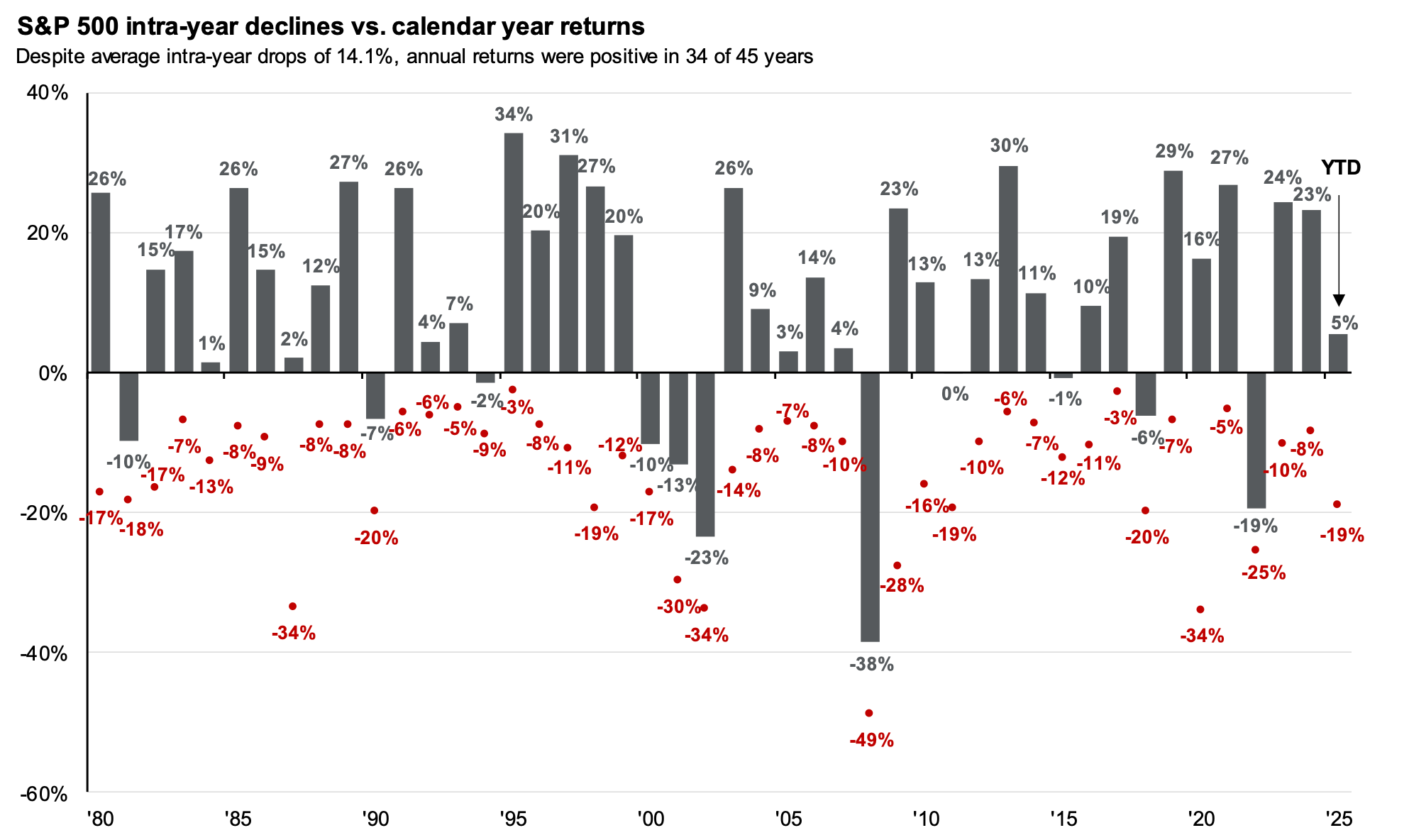

Investors should always be mentally prepared for some big sell-offs in the stock market. It’s part of the deal when you invest in an asset class that is sensitive to the constant flow of good and bad news. Since 1950, the S&P 500 has seen an average annual max drawdown (i.e., the biggest intra-year sell-off) of 14%.

(Source: JPMorgan)

(Source: JPMorgan)

Every recession in history was different. And the range of stock performance around them varied greatly. There are two things worth noting. First, recessions have always been accompanied by a significant drawdown in stock prices. Second, the stock market bottomed and inflected upward long before recessions ended.

(Source: Goldman Sachs via TKer)

(Source: Goldman Sachs via TKer)

Since 1928, the S&P 500 generated a positive total return more than 89% of the time over all five-year periods. Those are pretty good odds. When you extend the timeframe to 20 years, you’ll see that there’s never been a period where the S&P 500 didn’t generate a positive return.

While a strong dollar may be great news for Americans vacationing abroad and U.S. businesses importing goods from overseas, it’s a headwind for multinational U.S.-based corporations doing business in non-U.S. markets.

(Source: FactSet via TKer)

(Source: FactSet via TKer)

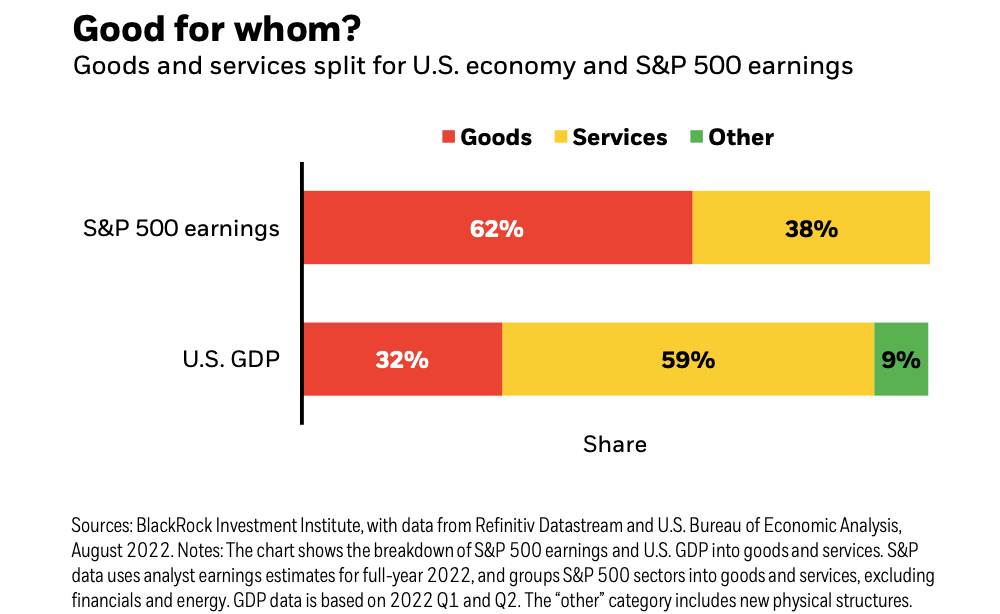

The stock market sorta reflects the economy. But also, not really. The S&P 500 is more about the manufacture and sale of goods. U.S. GDP is more about providing services.

(Source: BlackRock via TKer)

(Source: BlackRock via TKer)

…you don’t want to buy them when earnings are great, because what are they doing when their earnings are great? They go out and expand capacity. Three or four years later, there’s overcapacity and they’re losing money. What about when they’re losing money? Well, then they’ve stopped building capacity. So three or four years later, capacity will have shrunk and their profit margins will be way up. So, you always have to sort of imagine the world the way it’s going to be in 18 to 24 months as opposed to now. If you buy it now, you’re buying into every single fad every single moment. Whereas if you envision the future, you’re trying to imagine how that might be reflected differently in security prices.

Some event will come out of left field, and the market will go down, or the market will go up. Volatility will occur. Markets will continue to have these ups and downs. … Basic corporate profits have grown about 8% a year historically. So, corporate profits double about every nine years. The stock market ought to double about every nine years… The next 500 points, the next 600 points — I don’t know which way they’ll go… They’ll double again in eight or nine years after that. Because profits go up 8% a year, and stocks will follow. That’s all there is to it.

Long ago, Sir Isaac Newton gave us three laws of motion, which were the work of genius. But Sir Isaac’s talents didn’t extend to investing: He lost a bundle in the South Sea Bubble, explaining later, “I can calculate the movement of the stars, but not the madness of men.” If he had not been traumatized by this loss, Sir Isaac might well have gone on to discover the Fourth Law of Motion: For investors as a whole, returns decrease as motion increases.

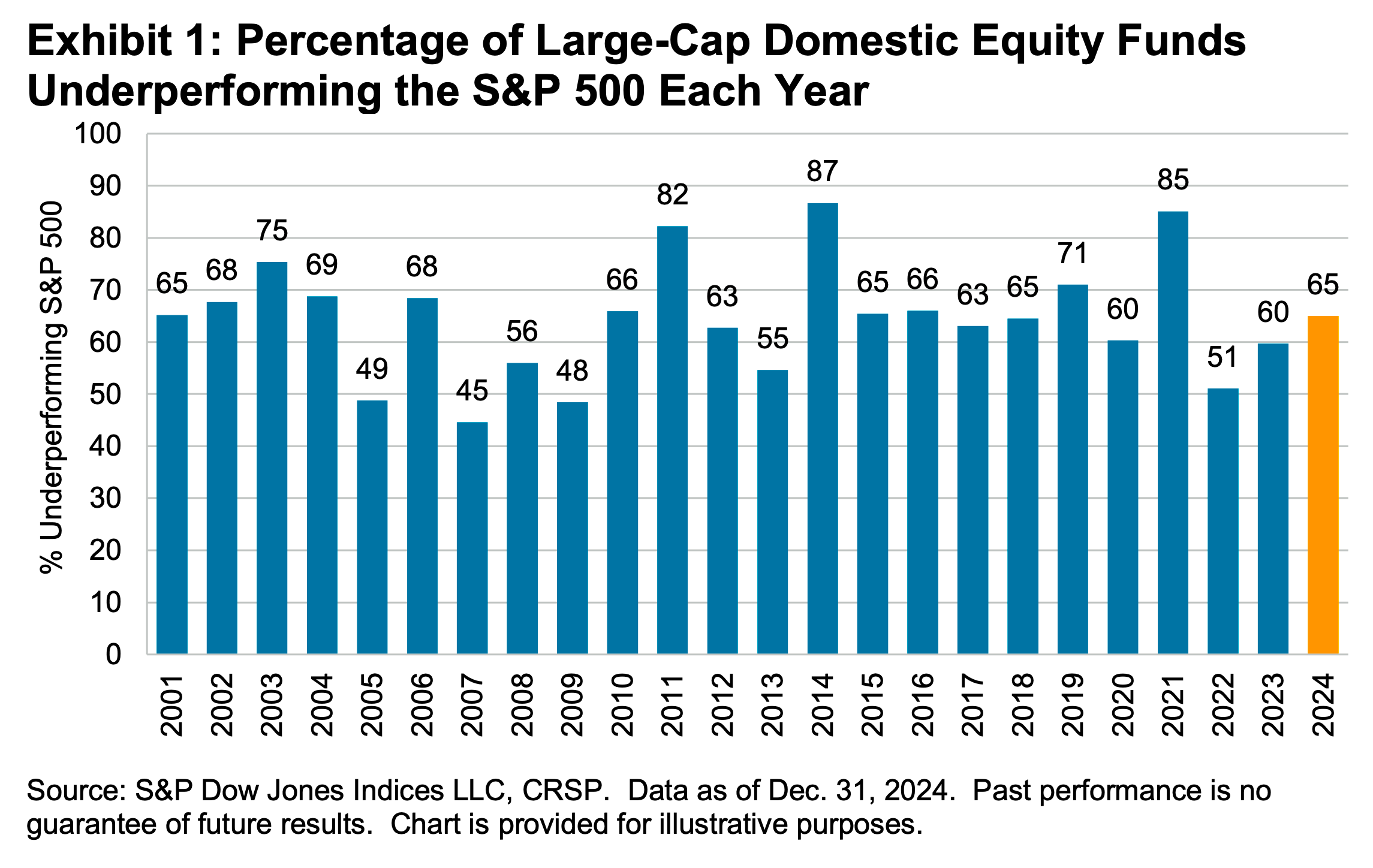

According to S&P Dow Jones Indices (SPDJI), 65% of U.S. large-cap equity fund managers underperformed the S&P 500 in 2024. As you stretch the time horizon, the numbers get even more dismal. Over a three-year period, 85% underperformed. Over a 10-year period, 90% underperformed. And over a 20-year period, 92% underperformed. This 2023 performance follows 14 consecutive years in which the majority of fund managers in this category have lagged the index.

(Source: SPDJI via TKer)

(Source: SPDJI via TKer)

Even if you are a fund manager who generated industry-leading returns in one year, history says it’s an almost insurmountable task to stay on top consistently in subsequent years. According to S&P Dow Jones Indices, just 4.21% of all U.S. equity funds in the top half of performance during the first year were able to remain in the top during the four subsequent years. Only 2.42% of U.S. large-cap funds remained in the top half

SPDJI’s report also considered fund performance relative to their benchmarks over the past three years. Of 738 U.S. large-cap equity funds tracked by SPDJI, 50.68% beat the S&P 500 in 2022. Just 5.08% beat the S&P in the two years ending 2023. And only 2.14% of the funds beat the index over the three years ending in 2024.

Very few funds consistently beat their benchmarks over extended periods. (Source: SPDJI via TKer)

Very few funds consistently beat their benchmarks over extended periods. (Source: SPDJI via TKer)

Picking stocks in an attempt to beat market averages is an incredibly challenging and sometimes money-losing effort. Most professional stock pickers aren’t able to do this consistently. One of the reasons for this is that most stocks don’t deliver above-average returns. According to S&P Dow Jones Indices, only 24% of the stocks in the S&P 500 outperformed the average stock’s return from 2000 to 2022. Over this period, the average return on an S&P 500 stock was 390%, while the median stock rose by just 93%.

(Source: SPDJI via TKer)

(Source: SPDJI via TKer)