To print this article, all you need is to be registered or login on Mondaq.com.

Article Insights

Curtis A. Cusinato’s articles from Bennett Jones LLP are most popular:

within Corporate/Commercial Law topic(s)

with Inhouse Counsel

in Canada

with readers working within the Technology industries

The value of Canadian M&A transactions surged in 2025,

driven primarily by large cap deals and an acute focus on

infrastructure and resources. Total deal value last year was US$118

billion higher than 2024 on slightly fewer deals. Transaction value

hit a remarkable US$131 billion in the third quarter of

2025—the highest three-month tally since Q4 2020, according

to S&P Global Market Intelligence.

It is the same story globally. Bloomberg data highlights that

megadeals pushed M&A transaction value to a near-record US$3.6

trillion last year. This total is 38% higher than 2024 and second

only to 2021.

In our year-end update on Canada’s M&A landscape and

look-ahead to 2026, we provide key takeaways from the latest data

and market trends and examine:

the dynamics of large cap deals in Canadian M&A this past

year

challenges that remain in Canadian dealmaking

how infrastructure is taking centre stage in Canada

mid-market activity and what to watch out for in 2026 in

Canada

the Canadian credit markets in 2025 and what’s ahead in the

coming year

The aggregate value of announced or completed Canadian M&A

deals reached US$389.69 billion in 2025, surpassing the total from

2021. Large cap transactions drove this increase as the number of

deals decreased. We take a closer look below at the dynamics of

large cap dealmaking in Canada this past year.

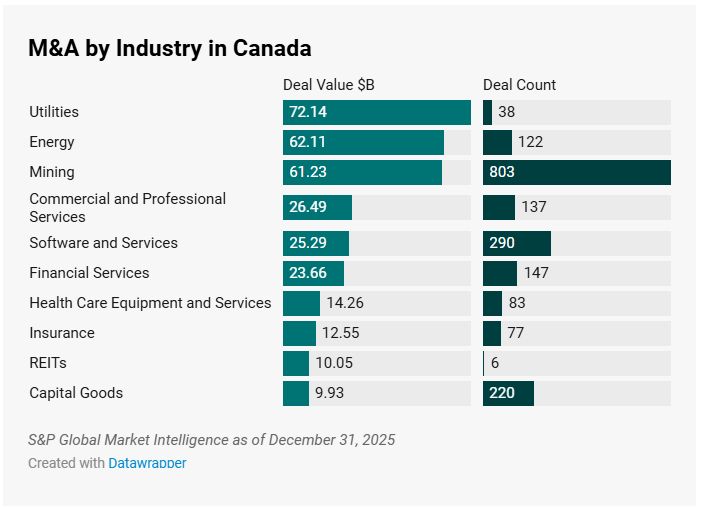

Utilities, energy and mining were the most active Canadian

industries, with a combined deal value of US$195.48 billion. This

is just over half of total Canadian M&A value in 2025. The

aggregate value of utilities deals rose by 82% in 2025 YOY, energy

is up by 257% and mining increased by 220%. Actual deal count

declined in all three industries last year.

The increased activity in these industries is not surprising

given the focus on digital assets and the intense demand for energy

and infrastructure resources. Globally, data center M&A and

investment set records in 2025, with more than US$61 billion

flowing into this market.

Gold had a standout year as Canadian deal value in the sector

more than tripled. In 2025 there were 8 gold transactions worth US

$1 billion or more—compared to 1 in 2024. Bloomberg reported

that globally, metals and mining M&A deal activity is up 61%

this year and 139% in North America alone.

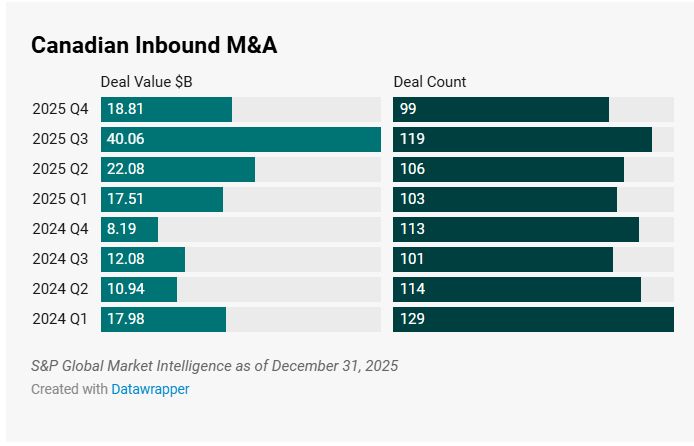

Canadian inbound M&A shot up in 2025, despite the continued

uncertainties and challenges to the country’s economy. Deal

value doubled to US$98.45 billion from US$49.19 billion in 2024, on

slightly fewer deals. Last year, there were 16 inbound deals worth

US$1 billion or more. In 2024, there were 12. Outbound

M&A—where a Canadian organization is the buyer or

investor and the target is outside the country—edged

higher.

Large Cap Deals Drive Canadian M&A in 2025

The surge in higher-value, strategic transactions has been the

most prominent trend in the Canadian M&A market throughout

2025. Publicly announced or completed M&A deals worth US$1

billion or more where a Canadian company is the acquirer, target or

seller totaled US$321.9 billion, according to S&P Global data.

This is an increase of 62% from last year and a staggering 130%

jump compared to 2023. The number of billion-dollar deals spiked to

78 in 2025—up from 54 in 2024 and 52 two years ago.

Key market drivers of the large-cap M&A trend include

strategic consolidation by large corporations to enhance market

positions, favourable financing conditions due to easing interest

rates and increased private equity investment as a result of

significant amounts of undeployed capital.

While large-cap M&A activity has spanned a variety of

Canadian industries this year, a particular concentration of

high-value deals has occurred in the energy, natural resources,

financial services and infrastructure sectors.

Large-cap M&A activity in the energy and natural resources

sectors has been fuelled by significant investment in energy

transition and critical minerals, the strong balance sheets of

large industry players, efficiency-driven consolidations aimed at

operational synergies and enhanced scale and the strategic desire

of companies to secure reliable supply chains amidst ongoing

geopolitical uncertainty.

Major energy transactions this year included:

A notable large-cap renewable infrastructure deal in the year

was

British Columbia Investment Management Corporation (BCI)’s

£1.0 billion take-private acquisition of BBGI Global

Infrastructure S.A.

Challenges Remain in Canadian Dealmaking

Despite the rise in large-cap M&A deals in the year,

dealmakers in Canada continue to navigate ongoing regulatory

scrutiny, tariff uncertainty and economic and political volatility.

High-value deals are being creatively structured and carefully

drafted to pre-empt and mitigate these risks.

New deal protections have been introduced into the Canadian

marketplace to address new risk profiles for possible national

security reviews under the amended Investment Canada

Act, to quell uncertainties around tariffs and

tariff-related legal issues, and other specific industry deal

protections where regulatory, trade, economic or other

uncertainties continue to prevail.

Infrastructure Takes Centre Stage

The vision for infrastructure development in Canada is an

ambitious one. The country’s strategy to be globally

competitive now depends on getting massive projects built quickly

and attracting billions of dollars in private sector

investment.

The federal government abruptly shifted its policy in 2025 on

advancing nation-building projects and launched the new Major

Projects Office (MPO) in late August. Since then, two tranches of

projects have been referred to the MPO in energy, critical minerals

and trade corridors.

Investors are keenly aware of the opportunities in Canada. The

head of North American Infrastructure for US private equity giant

KKR told The Globe and Mail in December,

“In the key sectors that are driving the biggest growth, be

it energy, digital infrastructure, both Canada and the U.S. should

play a really big role going forward. You have these two

mega-themes that are probably the two biggest ones bearing down on

the economy broadly, and they both squarely hit on

infrastructure.”

We similarly view the Canadian infrastructure industry as

remaining a key barometer of foreign investment and a leading

driver of M&A activity in Canada in 2026.

Canada’s Mid-Market

M&A activity in Canada’s mid-market (US$20

million

Mining was the most active industry by far with US$10.58 billion

in mid-market deals in 2025—with gold accounting for 54% of

this activity. Financial services came next, followed by software,

energy, capital goods and pharmaceuticals, biotechnology and life

sciences.

The defence industry will be one to watch in 2026, especially in

private capital dealmaking. Investment in defence and dual-use

technologies is accelerating as government policy initiatives push

the industry into the mainstream. We have previously written on

the

spike in global VC deftech deal value in this new era for

defence.

Trends in the Canadian Credit Markets

As we look back at 2025 and into 2026, we see several trends in

credit markets and M&A financing which have been developed over

the past decade and continue to reshape how acquisition debt plays

through M&A.

The practical takeaway is that credit is increasingly accessible

and available on economic and deal terms that are conducive to

transacting for both strategic and financial buyers. What that

credit looks like, and from where it is sourced, may differ

depending on several factors, including transaction value and

nature of the buyer (corporate strategic vs sponsor).

Today, private credit has a seat at the table in almost any

discussion around acquisition financing options in Canada. South of

the border, PE direct lenders have emerged as a viable and robust

option to traditional banks in financing acquisitions of all types

and sizes, from mega deals to small-cap. It is now common to see

US-based direct lenders as the sole financing source (either in

club structures or unilaterally) on inbound cross-border M&A

transactions.

In Canada, our banks continue to be comparatively conservative

in their leveraged acquisition underwriting standards. However,

they remain the usual acquisition financing option for their key

relationship large corporates and top tier Canadian sponsors. That

said, hybrid debt financing stacks are often seen in Canadian

middle market sponsor-driven transactions, with banks providing a

senior financing solution and private credit filling in the junior

or mezz piece required to complete the transaction. The private

credit option, which is now an entrenched part of the broader

credit market, offers buyers an alternative that fills gaps left by

banks constrained by regulation, risk tolerance or other

underwriting limitations, and terms which may be more flexible and

buyer friendly.

With rates continuing to improve (even if still above their

Covid historical lows) and credit markets continuing to be robust

and evolving in ways which will help facilitate transactions,

access to credit will be a key driver to continuing strength in

M&A activity in 2026.

Looking Ahead

Predictions for M&A activity in 2026 are positive but

nuanced. Many dealmakers expect to see the trends of larger

transactions and certain key industries in Canada remain in high

demand in 2026. The AI boom is driving growth far beyond the

technology sector and the level of investment in data centres and

the infrastructure that supports them is astounding. In particular,

we expect there will be continued growth in AI for certain

participants in this industry, including equipment, cooling

systems, structural and other integral products.

That said, the outlook for the global economy is unsettled and

trade tensions continue. In Canada, regulatory scrutiny remains a

concern and our economic relationship with the US is still in flux.

And as we saw in 2025, unexpected policy announcements can change

the dealmaking landscape quickly and profoundly.

While the path ahead requires a steady hand, the abundance of

high-quality opportunities suggests that 2026 is well-positioned to

be a year of strategic growth in dealmaking.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.