Weekend Reading – I Don’t Know

Welcome to a new Weekend Reading edition about things I know and things I don’t know.

First up, some reminders on other content:

I believe name changes would be (somewhat) beneficial to many existing financial accounts:

Weekend Reading – Name changes are needed to financial accounts

Here is our latest dividend and distribution income update – I will have a new tally to share soon thanks to investments made inside both of our TFSAs earlier this month.

December 2025 Dividend Income Update

Weekend Reading – I Don’t Know

Inspired by a few articles I read this week and last week, I wanted to share this: I don’t know.

I don’t know what stock market returns might be.

I don’t know what the price of gold or silver will be later this year.

I don’t know if inflation will stay elevated.

I don’t know if house prices will ever flatten out or come down a bit.

I don’t know if Canadian stocks are going to do better (again) than the S&P 500 this year.

This is why you diversify and spread your assets around.

For us, our portfolio diversification means a mix of 1. individual stocks, 2. low-cost ETFs and 3. cash/cash equivalents like GICs, cash-alternative ETFs and money market funds. You can read How We Invest here.

For diversification, you might decide on owning many stocks from many sectors or maybe even better, you own many stocks from many countries around the world. You might even own some gold, silver, bonds, real estate and more assets that should appreciate in value over time…

Beyond our stocks and ETFs for income and growth, we continue to own some cash/keep some cash equivalents on hand for these reasons:

Leveraged from Morningstar:

“And it’s always important to keep some cash on hand to cover unexpected emergencies, such as job loss, car repair, appliance replacement, and so on. Most financial advisors recommend keeping at least six to 12 months’ worth of living expenses in cash as an emergency fund—even if you don’t end up spending it right away.”

And from Morgan Housel:

“We do it because cash is the oxygen of independence, and – more importantly – we never want to be forced to sell the stocks we own.”

Ben Carlson from A Wealth of Common Sense also believes in I Don’t Know.

For fans of U.S. dividend stocks, my friend Dividend Growth Investor shared a list of 2026 Dividend Aristocrats.

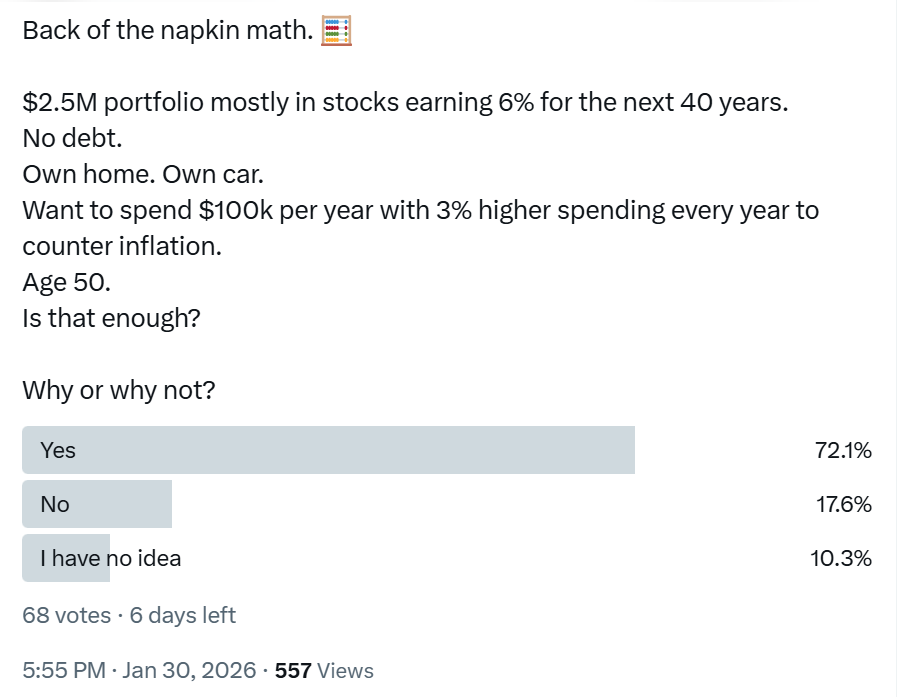

For fun, this poll:

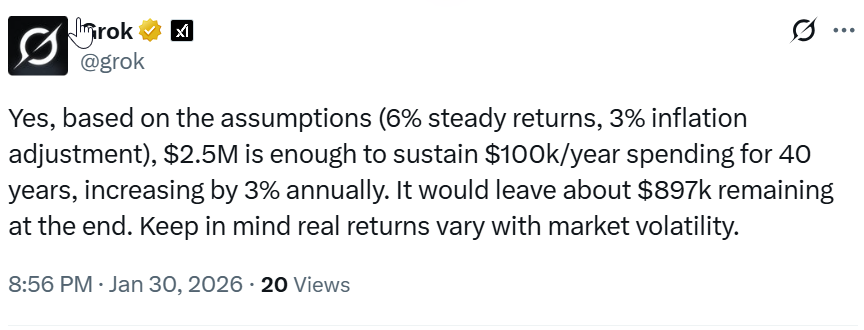

And for some fun back, someone asked AI for an answer:

What do you think? (And before you ask, yes, $100k spending = spending money after-tax.) 🙂

Over on MoneySense, Jon Chevreau highlighted many folks remain wary of creating their own pension via annuities.

Finally, back by demand – what if you simply owned a simple, all-in-one ETF and wanted to retire on just that? Could you retire owning just one ETF across your entire portfolio??

Read on:

Can you retire using a 60/40 portfolio?

Have a great weekend!

Mark

My name is Mark Seed – the founder, editor and owner of My Own Advisor. As my own DIY financial advisor, I’ve reached financial independence. Now, I share my lessons learned for free on this site. Join the newsletter read by thousands every week.