Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Can PhonePe build a profitable payments business?

How did quick commerce fare this quarter?

One of India’s largest fintech players, PhonePe, is preparing for an IPO.

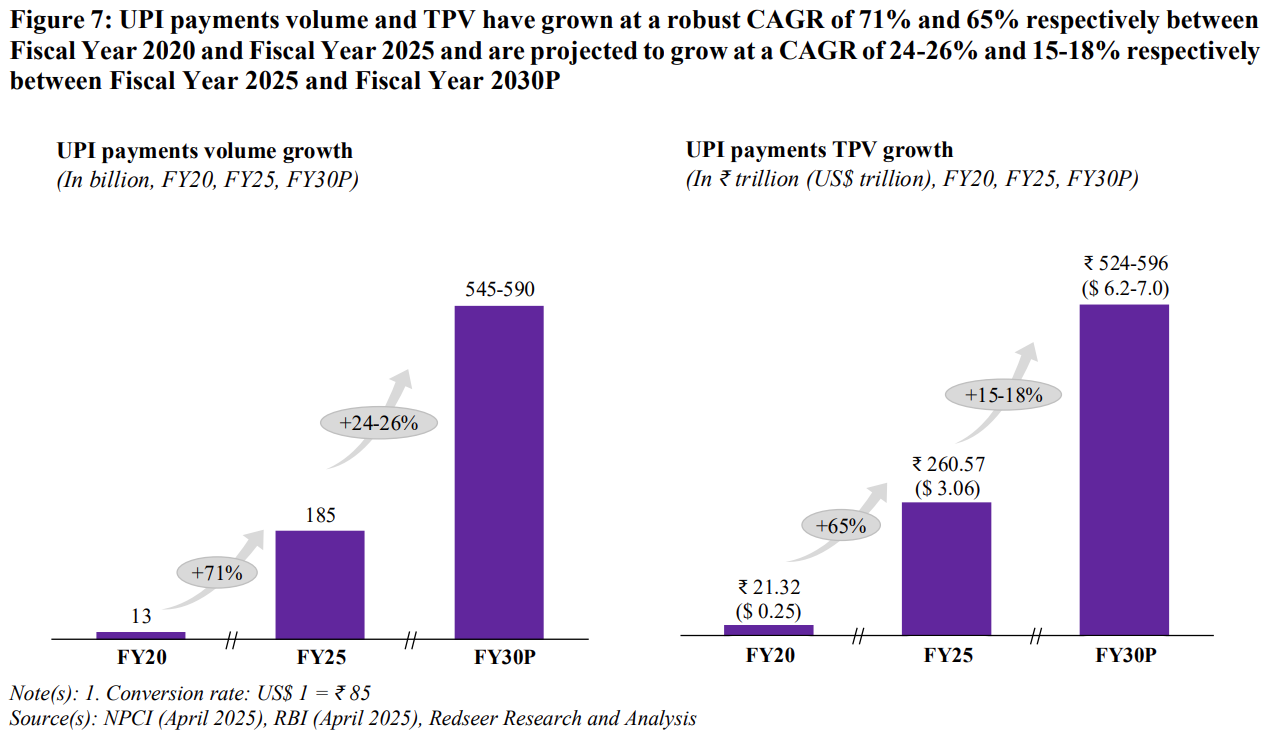

For most of us, PhonePe simply means UPI. And it’s hard to overstate how big UPI has become. In FY20, Indians did about 13 billion UPI transactions. By FY25, that number was ~185 billion, more than 14x growth in five years, at population scale. And companies like PhonePe have been the biggest beneficiaries of that shift.

So the debate isn’t really about whether PhonePe has scale — it clearly does. The real question is simpler, yet tougher: can PhonePe turn that scale into a profitable, sustainable business? That’s an exercise we are doing, to better understand their business. So, let’s begin.

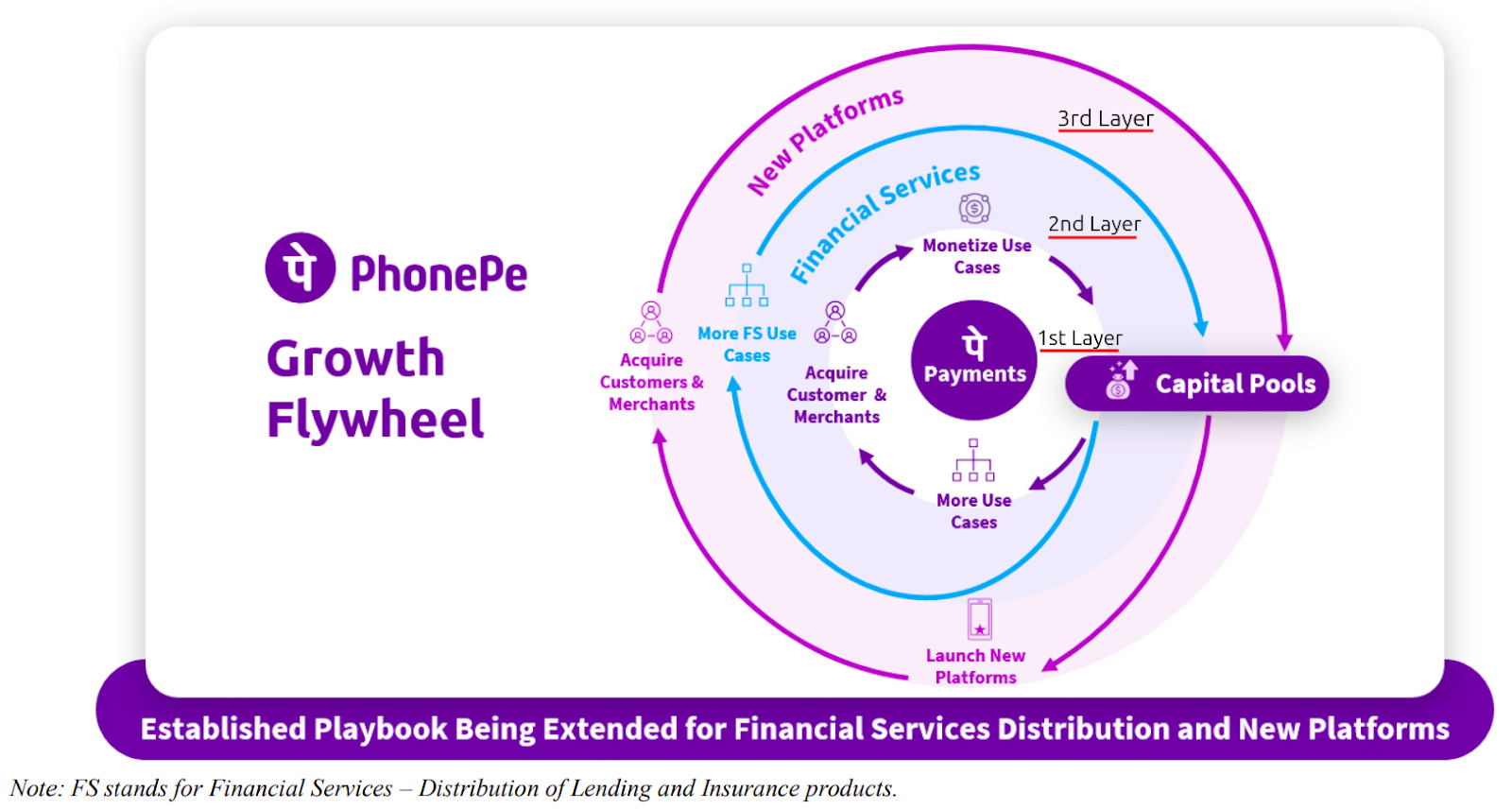

PhonePe does a lot of things. So you need a simple mental model to keep yourself from getting lost. For that, we don’t have to look much further than PhonePe’s own framing of it as a three-layer cake:

Layer 1 is daily payments. It’s the foundation where habits are built through UPI transfers, QR payments, bill payments.

Layer 2 is the monetization layer. This is where PhonePe tries to make meaningful money through merchant tools and devices, plus selling/distributing financial products like insurance, loans, gold and mutual funds.

Finally, the new platform layer. Things like its stockbroking app and app store, built on top of the cash and distribution from the first two layers.

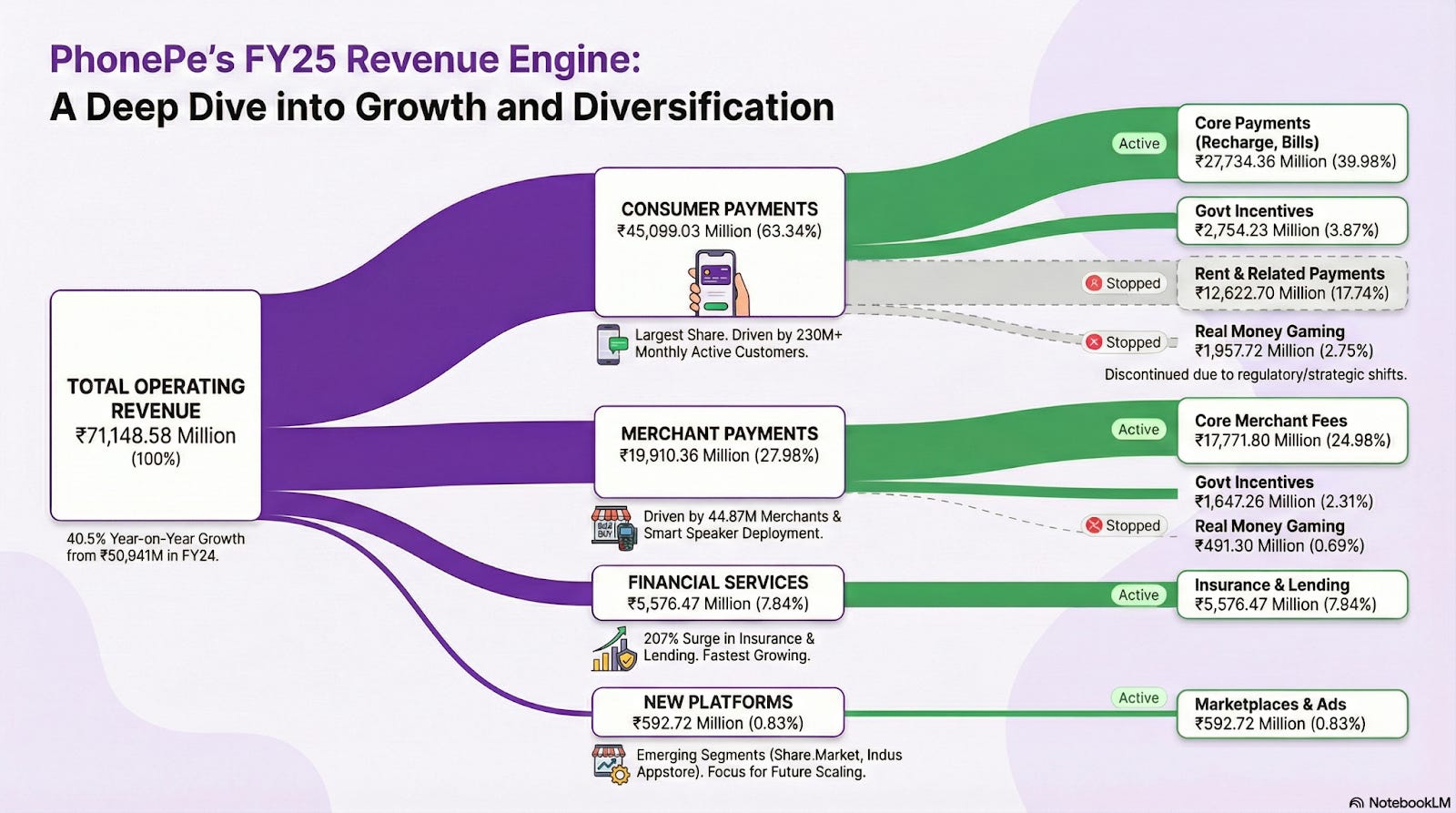

Now this model isn’t theoretical, as it helps us understand PhonePe’s ~₹7,115 crore revenue of FY25.

The biggest part of PhonePe’s business is consumer payments. At first glance, this sounds contradictory. If UPI is technically free for you and me, why does “consumer payments” contribute 63% of revenue?

That’s because “consumer payments” here doesn’t mean only P2P UPI transfers. It includes multiple smaller fee pools that sit around the payment experience. It includes things like recharges, bills, etc. where PhonePe earns money through commissions from service providers, and sometimes convenience/platform fees. Additionally, they also receive state incentives to process low-value digital transactions that are otherwise free for users.

Beyond these, there are two more consumer lines that were meaningful in FY25….but are now stopped. Together, they made up roughly one-fifth of PhonePe’s revenue.

Firstly, PhonePe used to let tenants pay rent, maintenance, or brokerage to non-merchants using credit cards, and it took a chunky fee for enabling that. But the RBI shut this down. The issue was that these were essentially peer-to-peer transfers to recipients who weren’t verified like merchants, which raises money-laundering risks.

Real-money gaming was the second hit. When the government cracked down on it last year, the damage spread beyond gaming apps. Payment players like PhonePe also took a knock because they used to earn fees when users made UPI transfers into these gaming platforms.

The second biggest business line for PhonePe is merchant payments, which contributed ~₹2,000 crore (28%) in FY25.

This includes monetization from devices like soundboxes, tools that help merchants accept payments outside of UPI, and related value-added services. PhonePe also has a payment gateway that contributes here. And, much like consumer payments, here too they earn some ~₹165 crore from government incentives.

PhonePe’s revenue has gradually been moving away from consumer convenience-fees and toward merchants. The share of this segment has doubled from 15% in FY23 to ~31% in the latest numbers. It makes sense, too — after all, this looks far more monetizable than “free” consumer transactions.

Then, financial services revenue comes in at nearly 8%. But, while small, it’s one of the fastest-growing parts of the business. It is the monetization bet that they are making for the future.

This bucket mostly includes insurance and lending distribution. PhonePe distributes products from partners and earns commissions and referral fees. Importantly, this is not the same as lending or insuring from your own balance sheet. The risk profile is different. Instead, they leverage the balance sheets of their 56 lending partners (NBFCs & Banks) and 29 insurance partners.

There is a nuance, though. PhonePe has disclosed that it offers limited credit guarantees in certain partner-lending setups. That’s not the same thing as becoming a lender, but it’s worth tracking as a potential source of balance sheet risk.

Finally, new platforms contributed barely ~1% of FY25 revenue.

But strategically, it matters because this is where PhonePe is trying experiments at longer-term bets — like its stockbroking platform and its app store effort. These businesses are still early. They are also mostly loss-making today. One of its experiments in quick commerce, Pincode, has already shut down after running for a couple of years.

Once you understand PhonePe’s revenue engine, the next question is obvious. Is this business actually getting profitable in a real, durable way?

To answer that, you have to look at two profit metrics often thrown around:

EBITDA — which is profit from operations before interest, tax, depreciation and amortisation

PAT (Profit After Tax) — the final bottom line: what’s left after everything

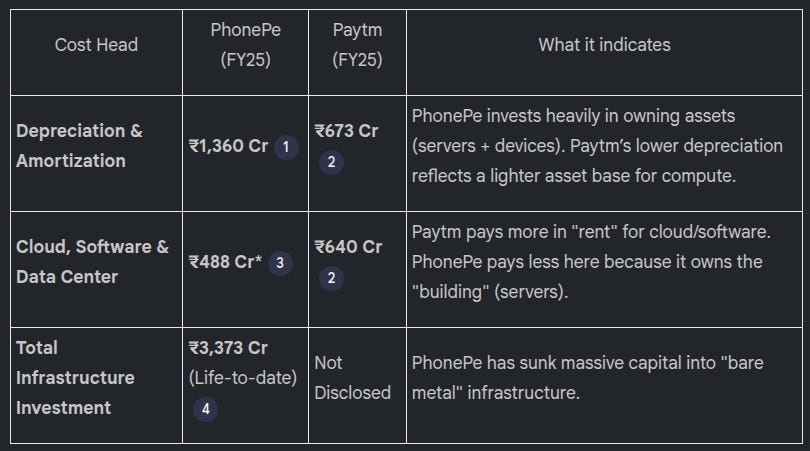

PhonePe looks much better on the first than the second. And that gap is not accidental by any means.

Since inception, PhonePe has invested over ₹3,800 crore to build its own on-premise data centres in India, instead of running most of its workloads on a public cloud like many competitors. In simpler terms: rather than renting computing power from a provider like AWS, it decided to buy its own servers and run them inside its own facilities.

In fact, it even became the first company in India to set up an “underwater” data centre.

The logic here is pretty straightforward.

On the cloud, your costs scale almost linearly with usage. So more transactions usually mean a bigger cloud bill. But when you own the infrastructure, a big chunk of the cost is paid upfront. If you grow enough, your cost per transaction can drop sharply.

In other words, this is a bet on operating leverage. It also gives them control: data localisation, performance tuning, energy optimisation, hardware-level efficiency — all the stuff that matters when you’re running population-scale transactions.

But there’s a trade-off. When you own infrastructure, you also own the risk of depreciation. And right now, that depreciation load is heavy enough that it can exceed what a cloud-first competitor (like PayTM) might be paying as a running expense. That doesn’t mean the decision is wrong — it just means the decision only looks brilliant once you sustain scale.

So a simple way to frame it is that PhonePe’s infra model can be cheaper in the long run, but it is expensive in the short run — until scale fully catches up. It’s a software company that, weirdly, is quite physical asset-heavy.

But depreciation is only part of the story. There’s another non-cash expense that messes up their finances.

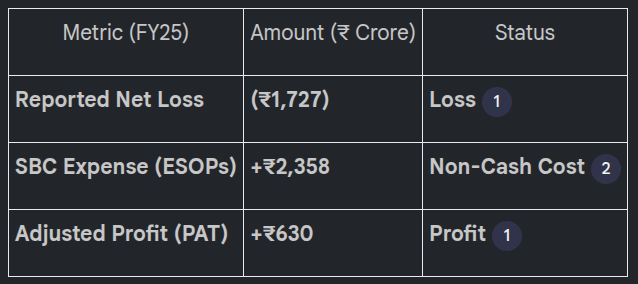

PhonePe’s share-based compensation (SBC) is very high. In fact, it is the single biggest factor determining whether PhonePe looks profitable or loss-making on paper. If PhonePe did not have to record ESOP expenses, it would have posted a profit of ₹630 crore in FY25 instead of a loss.

You’ll often hear people dismiss SBC as “non-cash”, and therefore treat adjusted EBITDA as the real story. But that’s not honest. SBC is still a cost just paid in equity instead of cash.

And that matters because it does two things at once. Firstly, it makes the company look more profitable on a cash basis in the short run, because you’re not paying that compensation out as salary. Secondly, it is still dilutive. Over time, it transfers value from shareholders to employees.

It’s also one reason why cash conversion can look underwhelming relative to operating profitability. The business may show a decent EBITDA, but the “true cost” of running it is partly being paid via dilution.

All of this — infra leverage, depreciation load, SBC — can only be managed as long as PhonePe achieves scale. It is what allows a business like PhonePe to absorb fixed costs and keep pushing unit costs down.

But that scale engine has been challenged recently. Two revenue pools that mattered in FY25 — real-money gaming and credit-card funded rent-related payments — have been switched off. Together, they were a meaningful portion of revenue, and they were also relatively high-margin.

The government is also withdrawing many of the incentives it has been giving to this ecosystem. First, RBI decided not to extend the Payments Infrastructure Development Fund after 31st Dec, 2025. And now, the latest budget saw a 10% drop in outlay towards subsidizing UPI and Rupay. That’s a loss of revenue from the government side too.

So in FY25, you see a business that looks like it’s gaining operating leverage. Then, in H1 FY26, you see the discomfort: growth stalls, and profitability metrics soften.

If you’ve read everything so far and thought, “Okay, so PhonePe just needs to keep scaling and the rest will sort itself out” — that’s exactly where the risks begin. In many ways, PhonePe may have gotten used to a world where scale was almost automatic. UPI kept growing, PhonePe kept riding that wave, and the flywheel kept spinning. But many things are now getting in the way.

For starters, NPCI has been talking about capping any single UPI app’s market share at 30% for years now. Enforcement has been delayed repeatedly, but the latest deadline is 31 December 2026. PhonePe’s disclosed UPI share is well above that cap. If that cap becomes real, the implication is simple. PhonePe can’t simply rely on “scaling” as their path to profitability.

This also forces them to focus on monetization much sooner than they would have liked. That’s not always bad — In fact, it can sometimes make a business more disciplined. But it does mean PhonePe’s next phase will be judged far more on monetization and unit economics, not just usage charts.

And then, things like regulatory kill-switches, and government incentives being sunset, only further complicate the story for PhonePe.

This leaves us with a very simple framework to fall back to. Does revenue shift from “easy but fragile” pools to durable, repeatable pools? How much does it have to depend on revenue that can vanish with a policy tweak? How much does it make just because customers keep coming back to the platform?

In practice, that means watching the mix shift from consumer revenue — where a meaningful chunk comes from policy-sensitive fee pools — to merchant revenue. Here, monetisation tends to be deeper and stickier because it’s tied to daily business workflows. It also means tracking how much comes from lending and insurance distribution, which can be higher-quality revenue if risk is controlled.

And finally, it means keeping an eye on the new platform bets—the ones burning money today in the hope that they eventually turn into profit engines.

Quick commerce is one of those spaces that we have been tracking very closely. Since the last time we covered the results of Swiggy and Zomato, we wrote about why quick commerce seems weirdly suited for India and went into great detail about how it’s doing overseas. In our weekend show, “Who Said What”, we spoke about the developments in China’s quick commerce companies.

Now, let’s cover what the 3rd quarter results say about Swiggy and Zomato.

Zomato reported more than ₹16,000 crore in revenue in a single quarter and posted a profit.

Swiggy reported revenue of a little over ₹6,000 crore and continued to make sizable losses.

If one were to judge purely by headline numbers, the conclusion would seem obvious: Zomato is far ahead, and Swiggy is still struggling to catch up.

That conclusion would miss what is actually going on. The gap in reported revenue is not a reflection of a five-fold difference in customer demand or order volumes. It is primarily the result of a conscious strategic choice made by Zomato in how it runs its quick commerce business.

Before getting into this, it is worth noting a change that says more about Zomato’s priorities than any quarterly disclosure. Deepinder Goyal stepped down as Group CEO of Zomato. Albinder Dhindsa, the CEO of Blinkit, will take over as CEO of Eternal. It looks like Zomato no longer sees itself primarily as a food delivery company. Instead, quick commerce has now taken centre-stage. That shift frames everything that follows.

The key to understanding this divergence lies in how Blinkit and Instamart account for their sales.

Blinkit operates largely on an inventory-owned model. It buys goods directly from brands, stores them in its dark stores, and sells them to customers. Because Blinkit owns the inventory, the full value of every item sold is recorded as revenue. If a customer buys a ₹100 bottle of shampoo, Blinkit records ₹100 as revenue.

Instamart, by contrast, still operates largely as a marketplace. In many cases, the inventory in its dark stores is owned by brands or distributors. Swiggy facilitates the transaction, handles logistics, and earns a commission. In accounting terms, it records only that commission — like ₹15 on a ₹100 order — as revenue.

This difference alone explains most of the headline gap. Zomato’s revenue number looks much larger, but not because it is delivering five times as many orders. It’s because it is booking the entire value of the basket rather than a slice of it. Zomato itself acknowledges this by providing “like-for-like” numbers that strip out inventory sales, where the difference gets far less dramatic.

The cost of moving from platform to marketplace model is visible in the financials. In Q3 FY26, Eternal spent over ₹10,000 crore on “purchase of stock-in-trade” alone. That is ~60% of reported revenue. This money is paid up front, long before customers place their orders. Inventory ties up working capital, and any miscalculation in demand or assortment can quickly become a drag on returns.

Food delivery, which once defined both Zomato and Swiggy, is now a far more predictable business. Growth has slowed meaningfully from the breakneck pace of a few years ago, and the focus has shifted from expansion to optimization.

At Zomato, food delivery growth in Q3 FY26 was in the high-teens, with management indicating a gradual improvement in growth momentum across cities. Swiggy reported similar numbers, with its food delivery business growing about 21% during the quarter.

These are still healthy growth rates, but they are a far cry from the 40–50% growth the category saw in its earlier years when penetration was low.

Margins in food delivery now appear to have reached a more stable phase. Zomato reported an all-time high adjusted EBITDA margin of 5.4% of Net Order Value in Q3 FY26, a level that management has previously suggested is close to where the business should structurally settle. Importantly, the company is no longer talking about aggressive margin expansion in food delivery. Instead, the emphasis has shifted to maintaining discipline while redeploying incremental profits into newer businesses.

Profitability in Swiggy’s food delivery business remains lower than Zomato’s, and the company continues to operate with thinner margins as it balances growth and competitive intensity.

One subtle but telling change in Zomato’s reporting is how it now frames the food delivery business. The company has moved away from emphasising Gross Order Value and instead focuses on Net Order Value — the amount customers actually pay after discounts. While this arguably provides a cleaner view of monetisation, it also reduces visibility into how much demand is being driven by promotions. The shift signals that management wants investors to judge the business less on volume and more on value.

For both companies, the role of food delivery has changed. It is no longer the primary growth engine. Instead, it functions as a relatively stable cash machine that helps fund the far more uncertain battle currently unfolding in quick commerce.

Coming to quick commerce, Blinkit currently operates roughly 2,000 stores and has indicated that this number could rise significantly over the next year or two. Instamart operates a little over 1,100 stores and is expanding rapidly, but from a lower base.

Both businesses are growing quickly. Blinkit’s net order value grew well over 100% year-on-year. Instamart’s gross order value grew at a similar pace, though slightly slower. Both are also pushing average order values higher by expanding into non-grocery categories such as electronics, toys, and small appliances. Delivering a ₹700 order costs roughly the same as delivering a ₹400 order, so larger baskets materially improve unit economics.

The question, however, is whether this growth is translating into sustainable profitability.

Blinkit reached adjusted EBITDA breakeven in this quarter, an important psychological milestone. Management believes steady-state margins of 5–6% are achievable over time, pointing to certain mature markets where this is already the case. At the same time, the tone on margin visibility has become more cautious.

As Eternal’s CFO, Akshant Goyal put it on the Q3 FY26 call:

“It’s very hard to predict the trajectory of margin… Competitive intensity, even if it’s high, is not steady always.”

Pressed further on whether margins would continue to improve at the same pace, Goyal was explicit:

“We’re not able to confidently say that the pace of margin expansion will be the same as what happened in the last quarter.”

That uncertainty is not rhetorical. Management has openly said it is willing to take margin hits if competition turns irrational. Albinder Dhindsa was blunt about this trade-off: Blinkit will respond to aggressive pricing or incentives from rivals if needed, even if that delays profitability.

Swiggy’s Instamart remains loss-making, with adjusted EBITDA losses around ₹700 crore, but the trajectory is improving. Contribution margins have moved meaningfully in the right direction, and losses have narrowed sequentially. Swiggy’s strategy now is less about adding stores and more about increasing throughput per store. The network has been built.

This more disciplined tone around growth did not emerge by accident, though. Over the past quarter, the company actively tested whether it could buy growth more aggressively in quick commerce. This included lowering minimum order values and increasing discounting to see if cheaper entry points could help acquire users more efficiently.

The results were mixed at best. While these experiments lifted short-term volumes, they failed to create lasting behaviour. Management admitted that more than the entire margin improvement achieved in the previous quarter was reinvested into these initiatives, only for retention to fall short once incentives were pulled back. In effect, Swiggy discovered that it could pay for growth, but not for loyalty.

That experience has shaped how the company now talks about scale. Instead of chasing headline metrics such as orders per day, management says it is prioritising what it calls “good growth”: customers who stick, build habits, and generate repeat orders without discounts.

As one executive put it:

“We will never compromise good growth for margin, but we may compromise bad growth.”

That stance, however, comes with its own risk. In a market where speed and density matter, falling too far behind on scale can be costly.

Both companies are well-funded. Neither company is close to running out of money, and both can afford to keep investing for several years if needed. But cash doesn’t buy clarity. Competitive intensity remains high, the eventual size of the quick commerce market is still uncertain, and management teams themselves admit they are learning in real time.

The outcome will not be decided by one lone quarter. It will be decided by who can keep investing without undermining their own economics — and by whose underlying model holds up when this market eventually stops growing at breakneck speed.

As we wrote in our last results piece: whether q-com eventually becomes a stable, profitable business is still unclear. But for now, it’s the part of the business that is shaping almost every major decision they make.

India’s factory activity picks up in January

India’s manufacturing PMI rose to 55.4 in January, showing stronger factory activity after a weak December. New orders and output improved, driven mainly by domestic demand. But business confidence remains low, with companies still cautious about growth ahead.

Source: Business Standard

CPSE land assets to be monetised through REITs

The government plans to monetise land and real estate owned by CPSEs using REITs. The idea is to unlock value from unused assets and recycle capital more efficiently. Dedicated CPSE REITs could also deepen India’s REIT market and attract long-term investors.

Source: The Hindu BusinessLine

Paytm hit by subsidy exit, margins under pressure

Paytm is facing near-term margin pressure after the withdrawal of the PIDF scheme, which could hit revenue by about ₹2,000 crore annually. While payments growth remains strong, higher costs and lost incentives will weigh on profits. Financial services growth may soften the impact over time.

Source: ET BFSI

– This edition of the newsletter was written by Kashish and Krishna

Tired of trying to predict the next miracle? Just track the market cheaply instead.

It isn’t our style to use this newsletter to sell you on something, but we’re going to make an exception; this just makes sense.

Many people ask us how to start their investment journey. Perhaps the easiest, most sensible way of doing so is to invest in low-cost index mutual funds. These aren’t meant to perform magic, but that’s the point. They just follow the market’s trajectory as cheaply and cleanly as possible. You get to partake in the market’s growth without paying through your nose in fees. That’s as good a deal as you’ll get.

Curious? Head on over to Coin by Zerodha to start investing. And if you don’t know where to put your money, we’re making it easy with simple-to-understand index funds from our own AMC.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉