Weekend Reading – Why not celebrate a $3M Portfolio?

Hey Folks,

Welcome to a new Weekend Reading edition, about celebrating a $3M portfolio (over the same value of a house). More on that in a bit!

A reminder about some recent reads:

80-something Henry Mah continues to enjoy his cashflow for life.

Income Growth Investing and Cashflow for Life

And more recently…I shared our own income journey and update.

January 2026 Dividend Income Update

Weekend Reading – Why not celebrate a $3M Portfolio?

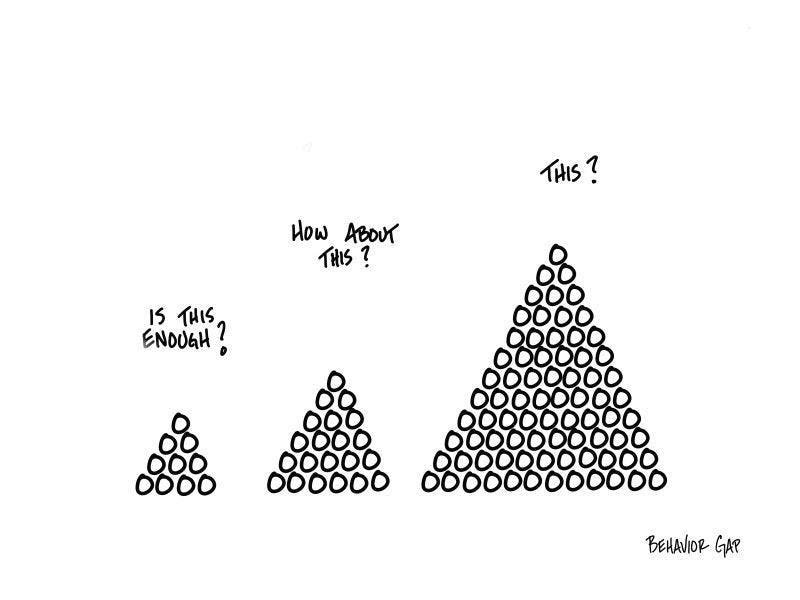

One of my favourite sketches:

Source: The Behavior Gap.

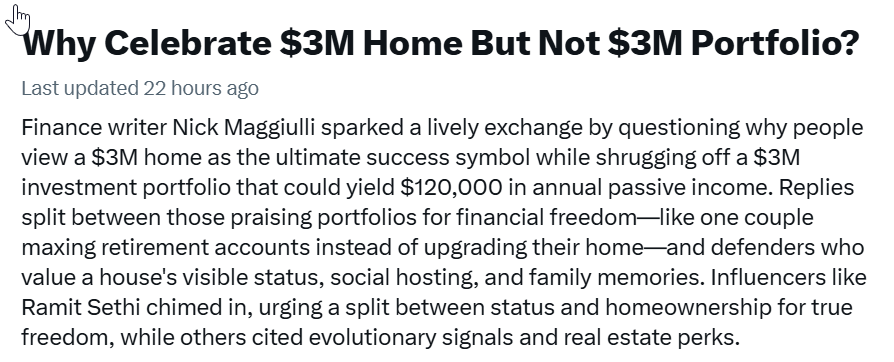

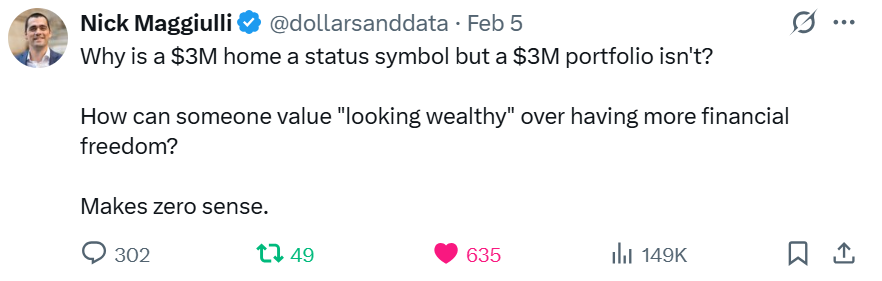

Inspiration for this headline arrived from this social media post this week – my goodness – I know my answer!!!

Kudos to Nick Maggiulli from Of Dollars and Data for this one that went viral.

And…

As someone who is not really into status, although I do like nice things for sure, I don’t need the biggest McMansion and I don’t aspire to own the nicest car in my neighbourhood that stays parked in my garage 90% of the time…

What’s your take on this? Surely you would rather have a tidy $3 million portfolio vs. a $3M dollar home?

In other reading material this week:

I found this article interesting, what Berkshire might sell next now that Buffett is no longer in charge.

I actually sold out of all my U.S. stocks including Berkshire over the past few years. All ETFs now for my ex-Canada investing so I continue to own Berkshire albeit indirectly via indexing.

Weekend Reading – Selling my U.S. stocks

Here are some things that Ben Carlson has been wrong about including:

“I thought the meme stock crash of 2021 would slow the speculation. At the time it felt like GameStop, AMC and the other meme stocks were a flash in the pan thing.”

“…Nope”.

Always interesting to read how much other retirees spend. U.S. blogger Accidential FIRE spent “…$43,051…only $403 higher than my total for 2024 for an increase of 0.9%. So why the hell aren’t I spending more!?!?!”

Very simple but good advice in The Globe and Mail (subscription) about this financial case study – the need to downsize to free up home equity for retirement – since this couple has “…a house worth $1.5-million, with a mortgage of about $400,000″ at age 59 and 65 respectively today. They will be forced to work into their early 70s if they don’t make any changes.

They want to spend $80,000 per year in retirement.

They won’t be able to make this spending plan happen unless they downsize and clear the debt.

Assets: Cash $7,000; her TFSA $139,530; his RRSP $138,755; residence $1,500,000. Total: $1,785,285.

Estimated commuted value of Cyril’s pension plan (provided by applicant): $675,000. That’s what someone with no pension would have to save to generate the same income.

Liabilities: Mortgage $394,780 at 4.9 per cent; CGHL $25,915 at zero interest; car loan $5,690 at zero interest. Total: $426,385.

Do you have the same thoughts as I do along with the financial expert = clear the debt??

Thoughts?

Have a great weekend!

Mark

My name is Mark Seed – the founder, editor and owner of My Own Advisor. As my own DIY financial advisor, I’ve reached financial independence. Now, I share my lessons learned for free on this site. Join the newsletter read by thousands every week.