I take requests. Last month I proposed that while affordability was a crisis for low-income households, for most of us it’s a rear-view mirror problem: a thing of the past, but some well-documented tricks of the mind are making that thing appear closer than it really is. Average wage growth caught and passed inflation a while ago. We tend to fixate on nominal prices, but we’ve actually established a new equilibrium.

One self-described fan of The Logic was unconvinced. She shared the story of an “older family friend” who can’t retire because her pension income doesn’t cover basic costs. This person, a caregiver, occasionally visits a food bank. “I would love to see you dig into the degree to which averages distort the painful financial reality for many people,” the fan wrote.

Higher food and shelter costs are a real thing for too many people. But that was true in 2019, before the inflation shock. The question today is whether affordability is the national crisis so many polls make it out to be. The answer matters because of the polycrisis. We have neither the fiscal nor the mental capacity to deal with everything at once. Fighting on one front will mean abandoning another.

One way to triage is to make sure we’re not obsessing over something that’s being magnified by the rear-view mirror. That could mean recognizing that there’s a qualitative difference between an older caregiver who can’t afford groceries and the apocryphal 30-something stuck in his parents’ basement. The former is a crisis. The latter is what David Adams Richards has called “comfortable victimization.”

Pierre Poilievre asked the Conservative convention last weekend what has changed since Mark Carney became Liberal leader and prime minister roughly a year ago. One answer to the Conservative leader’s question is that most of us are wealthier. That has little to do with Carney. Free-market economies have a way of correcting for shocks, even if most of their participants fail to notice. Remember all the fear and loathing over what would happen when millions of mortgages reset at higher rates? Nothing happened. The best answer to the affordability question at this point might be patience.

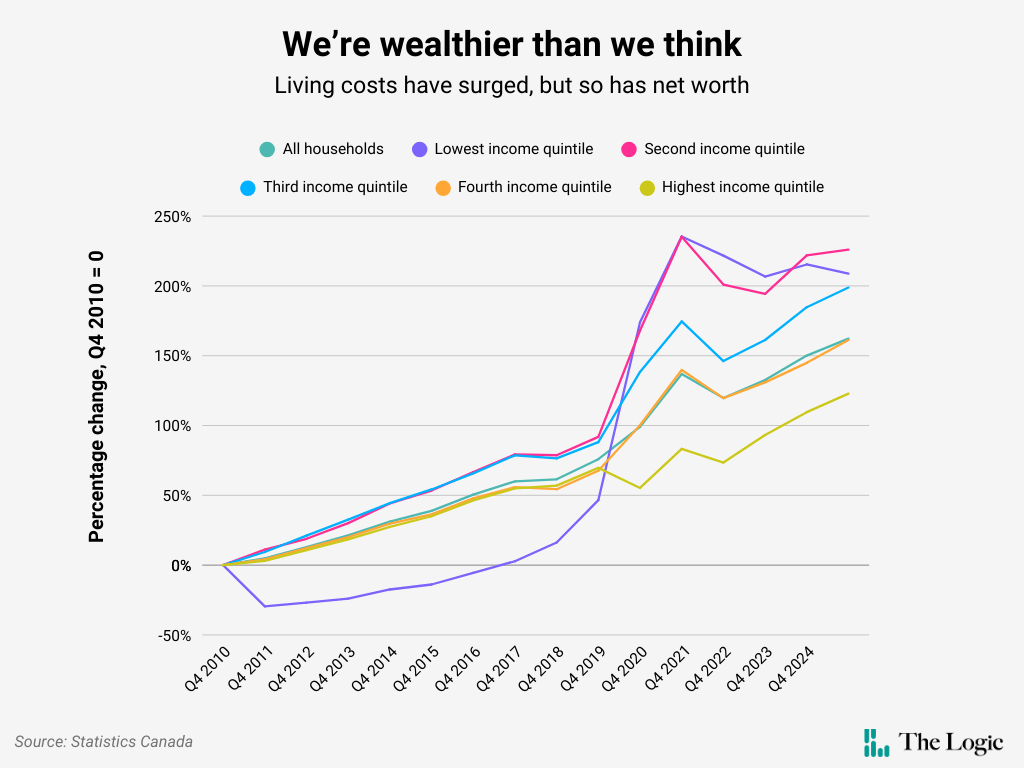

Statistics Canada knows that aggregate numbers obscure individual realities. One of the ways it attempts to draw a more complete picture is by dividing its entire sample of households into quintiles. Let’s stick with Poilievre’s 12-month yardstick. Household net worth—assets such as investments and real estate minus liabilities such as mortgages—increased 6.1 per cent in the third quarter of 2025 from a year earlier, compared with a 7.8 per cent increase over the previous 12 months. There’s foam on the runway if things go badly.

To be sure, that foam isn’t evenly spread. The net worth of the lowest income quintile declined 0.6 per cent, and has been essentially stagnant since 2020 and 2021, when poorer households got a temporary boost from COVID-19 benefits. The net worth of all other quintiles was higher, led by that of the third-highest income group, whose net worth increased 8.1 per cent after advancing a similar 8.3 per cent in the 12 months ending in the third quarter of 2024.

Those higher mortgage payments might have stung, but they continued to finance appreciating assets. The real driver of wealth in recent years has been the stock market. That’s what’s separating the lowest-income households from everyone else. The value of that quintile’s financial assets increased 4.9 per cent over the most recent four quarters, compared with 10.2 per cent for all households. Makes you wonder if we’re sleeping on financial literacy as a powerful way to address poverty.

Of course, we aren’t thinking about our stock portfolios when we check the price of ground beef or scan the rental listings. Nor do we consider that the cost of gasoline, internet access and child care are significantly cheaper now than they were a couple of years ago.

But given the stakes, do we really want our lizard brains making all the decisions right now? The Liberals and the Conservatives are essentially tied in public opinion polls. The political class has a huge incentive to give us what we think we want. Carney already scrapped the consumer carbon tax in the name of affordability, and Poilievre would sacrifice the revenue from the industrial carbon tax. The Conservative leader insists those taxes have added to the cost of food. Maybe a little, but research by Bank of Canada economist Olga Bilyk suggests the biggest issue is the cost of imported food items. International exporters don’t care about Canada’s carbon price.

About 80 per cent of the labour force—some 14 million people—works in eight of Statistics Canada’s broad occupation categories: wholesale and retail; health care; manufacturing; education; professional, scientific and technical services; construction; finance and real estate and public administration. The median wage in each of those classifications increased between 5.9 per cent (construction, 1.3 million workers) and 11.4 per cent (finance, 1.2 million workers) over the two years ending in December.

The all-items consumer price index increased 4.5 per cent over that two-year period. Food purchased from stores increased 5.8 per cent and Statistics Canada’s proxy for shelter costs increased 8.9 per cent.

I could be guilty of quantification fixation, our tendency to give weight to hard data over softer measures, or confirmation bias, given my hypothesis that the idea of a broad-based affordability crisis is now fuelled by narrative more than anything else. But my assessment of the data is that wage increases have at least offset higher prices, and quite often exceed them. That doesn’t mean affordability isn’t an issue, but it does raise questions about whether it’s the thing that should drive policy right now.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.