Bangladesh is set to spend over $30 billion this fiscal year to service its debts, covering both principal repayments and interest on domestic and foreign loans, according to projections by the International Monetary Fund.

The global lender has warned that unless Bangladesh significantly improves its revenue collection, the country will face heightened “rollover risks”, meaning the government may find it increasingly difficult and expensive to borrow new money to pay off its maturing debts.

In its Article IV Consultation Report published last month, the IMF estimated that public debt servicing would jump to $30.59 billion this fiscal year, up from $26.63 billion previously. This figure is expected to rise further to $33.84 billion in the next fiscal year.

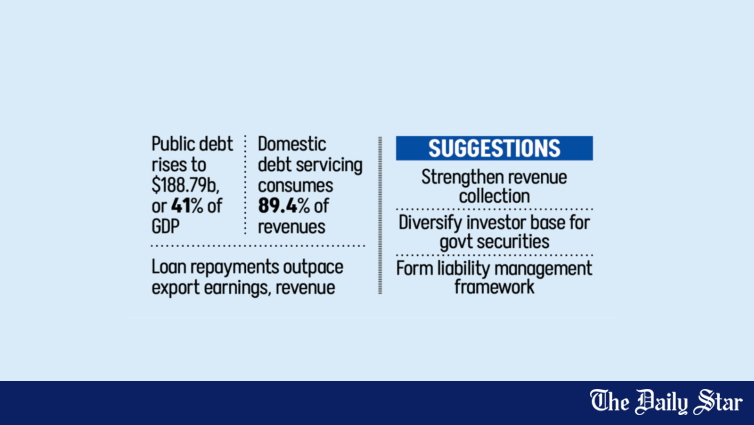

According to IMF data, Bangladesh’s total public debt now stands at $188.79 billion, rising to 41 percent of GDP in the 2024-25 fiscal year, up from 39 percent the previous year. This includes $101.24 billion in domestic borrowing and $87.55 billion in foreign loans.

In FY25, domestic debt repayments amounted to 4.2 percent of the GDP, while external debt servicing remained stable at 1.2 percent.

However, the strain on government coffers was severe. In the 2024-25 fiscal year, domestic debt stood at 22.6 percent of the GDP while servicing domestic debt consumed 89.4 percent of government revenues — a figure significantly higher than similar countries. Both ratios are expected to continue rising.

After falling to 0.3 percent of GDP in FY25, net domestic debt issuance is projected to average about 2 percent of the GDP over the forecast period, compared with a historical average of around 1 percent over the past decade.

“The elevated debt service-to-revenue ratio, including interest payments, poses significant rollover risks over the medium term,” the IMF said in its report.

The IMF noted that all public debt indicators are on a more prominent upward trend than in the previous analysis, reflecting higher borrowing costs and slower economic growth.

While tax reforms may slightly lower the debt service-to-revenue ratio by fiscal year 2026–27, extreme scenarios, such as a major natural disaster, could see it surge to over 110 percent of the GDP by 2030.

“This underscores the importance of raising the revenue-to-GDP ratio to reduce growing domestic debt vulnerabilities,” the IMF said.

Bangladesh’s tax-to-GDP ratio currently remains below 7 percent, limiting its ability to manage debt. Addressing this, Finance Minister Amir Khosru Mahmud Chowdhury has announced that the BNP government aims to raise this ratio to 8 percent in the upcoming budget.

The IMF warned that heavy reliance on domestic borrowing, particularly from banks, could “crowd out” private businesses, which means less money is available for the private sector, and strain the financial system’s capacity to absorb government debt, potentially pushing up borrowing costs.

Furthermore, if the government relies on the central bank to support insolvent banks, it risks losing control over short-term interest rates. This could trigger currency devaluation and inflation, creating a harmful economic cycle that would further undermine debt sustainability.

Overall risks to Bangladesh’s debt-servicing capacity are “notable and rising”, the IMF said. Delayed reforms in the banking sector or slow progress in boosting revenues — currently projected to reach only 12.2 percent of the GDP gradually — could weigh on economic activity in both the near and medium term.

To mitigate these risks, the report stressed the need to diversify the investor base for government securities, noting that authorities are already working on reforms, including to the primary dealer system.

A primary dealer system is an institutional arrangement where a select group of financial intermediaries, typically banks or large investment firms, are authorised to trade directly with the government to support the issuance and distribution of securities.

The IMF report also said that a liability management framework is essential to address increasing rollover risks.

Former finance adviser Salehuddin Ahmed, in a note to his successor, acknowledged that Bangladesh’s debt risk has been downgraded from low to moderate.

While the debt level is still considered tolerable by IMF benchmarks, he emphasised that caution is essential.

He noted that loan repayments are outpacing export earnings and government revenue.

The note advised strengthening revenue collection and avoiding high-interest, non-concessional loans whenever possible.

The recently dissolved interim government had also acknowledged these challenges in its response to the IMF. It recognised that low revenues, rising costs, and banking sector vulnerabilities pose urgent hurdles to meeting the country’s growing financial requirements.