The total amount of automotive debt in the United States is now at a level that exceeds the Gross Domestic Product of Turkey. That’s a lot of automotive debt, although it’s not necessarily a bad thing. Don’t let it scare you. It’s not the end of the world, yet.

Will that number rise next year? Yeah, probably. I have no crystal ball, nor does The Morning Dump ever achieve perfect foresight. Honestly, sometimes my hindsight is suspect. Here’s a prognostication: Incentives for gasoline-powered cars will likely increase, but not enough to offset the price increases next year.

![]()

![]()

Aston Martin isn’t waiting to find out and is therefore going to cut its workforce by about 20% as it tries to survive the downturn. Nissan, on the other hand, is going to double the number of Pathfinders. I wonder if that’ll work.

Debt Isn’t Bad Until It Is

I did not watch the State of the Union last night. It was clear it was going to be long, and I thought the time would be better spent sleeping rather than seeing if some White House staffer’s Kalshi prop bet pays off.

The full transcript is available over at the AP, and my general view is: I ain’t reading all that. I’m happy for you, though, or sorry that happened. Don’t tell Robert Caro, but I didn’t turn every page. I just did a Ctrl+F for the word “auto” and came up with this:

The cost of chicken, butter, fruit, hotels, automobiles, rent is lower today than when I took office by a lot. And even beef, which was very high, is starting to come down significantly. Just hold on a little while. We’ll get that down. And soon you will see numbers that few people would think were possible to achieve just a short time ago.

I will only speak to the automotive part of it; that’s maybe true if you compare January of this year to January of last year and look, specifically, at affordability. Here’s Cox Automotive on the costs:

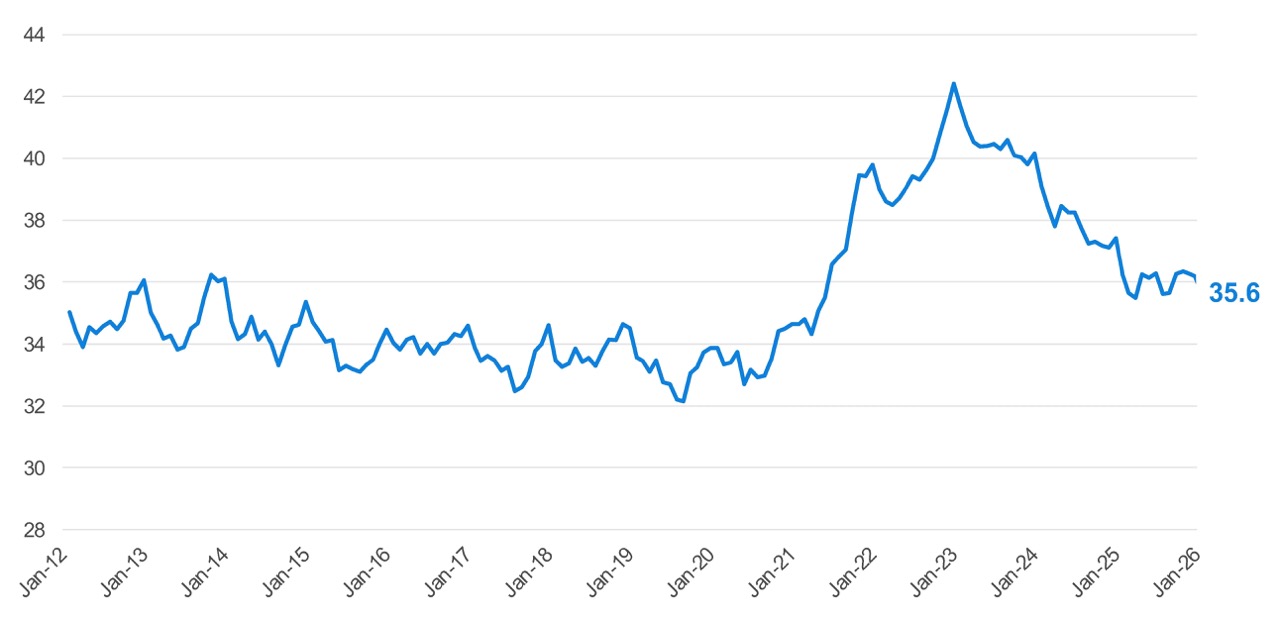

New-vehicle affordability in January was better than a year ago, when prices were 1.9% lower but interest rates were higher. Incomes were also lower a year ago. January incentives were 6.4% lower than a year ago, yet affordability still improved – a sign that macro tailwinds from lower rates and higher incomes continue to outweigh reduced manufacturer support. The new-vehicle affordability index fell by 1.8% year over year, indicating affordability improved last month. A year earlier, it required 36.2 weeks of median income to purchase the average new vehicle.

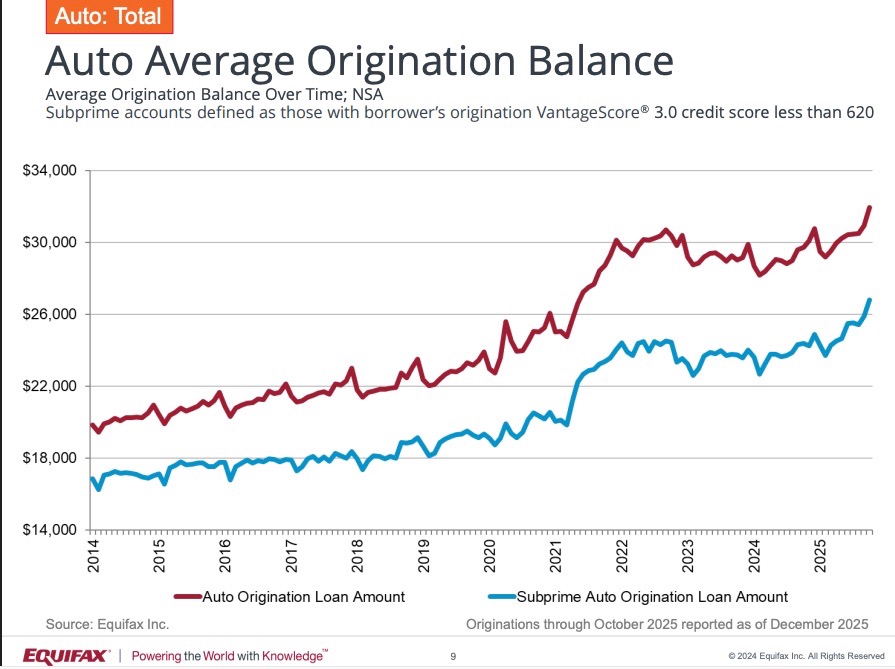

The cost of cars built outside of the U.S. (and thus the overall average) has gone up a lot, though, and terms have gotten longer, which means that the total amount people have spent financing cars has risen to new heights. According to Equifax, the total amount of automotive loan debt reached about $1.589 trillion in December of 2025, which is up by about 0.6% year-over-year. Add in leases, and that number grows to $1.685 trillion.

What you have to worry about with auto loans is not specifically the size, although it’s a fun number to put in the headline. It’s who is getting those loans and for what. Are subprime buyers taking a bunch of loans on wildly depreciating cars? Are delinquencies getting out of control? Equifax’s analysts don’t seem to think so:

Severe auto delinquency (share of balance 60+ DPD increased to 1.61%, up three basis points year-over-year, while auto write-offs decreased to 25.9 basis points. Delinquency trends have remained largely stable since late 2023, including within the subprime segment, where auto loans continue to rank as the top payment priority for borrowers.

There’s nothing about this that seems extreme. We’re now on year three of me writing about the bad loan vintages from the pandemic, and those haven’t all been paid off yet.

Here’s what stands out to me, though:

The average origination balance for all auto loans and leases issued in October 2025 was $31,962. This is a 7.6% increase from October 2024. The average subprime loan amount was $26,813. This is a 10.0% increase compared to October 2024.

This is the reality of today. Car prices have slightly improved, and the slow lowering of interest rates is, finally, starting to positively impact car buyers. To meet monthly payments, though, consumers are stretching further and further out into the future.

Again, it’s one of those situations where it’s not bad until it is. If unemployment stays low and the economy grows, then those loans are probably fine. President Trump said many times last night that the economy is strong and “roaring like never before.”

If the economy does stumble, though, and car values drop, then the underlying value of these cars will go down, and buyers will find themselves even more upside down as the loan term extends off into 60, 70, or even 80 months.

Cars Are Probably Not Going To Get Cheaper, Even If They Become More Affordable

Source: Cox Automotive

Source: Cox Automotive

Affordability is not that complex a metric, which is why it amuses me that it’s often misunderstood. When it comes to things you buy directly, affordability is a measure of the price of that object relative to your income. When it comes to things you finance, there’s the added dimension of the cost of borrowing.

The chart above is the Cox Automotive/Moody’s Analytics Vehicle Affordability Index referenced in the first story, which looks at how many weeks of income the average household needs in order to buy the average new car. This number spiked during the pandemic and has sort of flatlined this year as financing got easier, but cars really didn’t get cheaper.

With flat sales this year, it’s likely that some incentives will be out there in the market. Will this make cars cheaper? Probably not, as pointed out in this Detroit Free Press article on incentives and car sales:

“Our full year 2026 forecast is that incentives will increase $400 to $3,500, but given that last year had such a substantial electric vehicle incentive spend in the baseline, the true change is over $500 for (gasoline) powered cars,” Tyson Jominy, vice president of data and analytics at J.D. Power, told the Detroit Free Press.

How each automaker spends that extra $500 or more in incentive money will vary depending on their inventory and cost pressures, he said, and the competition for sales might not mean car buyers walk away paying less.

“Consumers will see higher transaction prices net of incentives on average, because automakers continue to increase (Manufacturer Suggested Retail Prices),” Jominy said. “Final transaction prices (for the full year) are expected to average $46,600, an increase of $800 versus 2025.”

With refunds coming, many buyers might have a slightly higher household income this year. If interest rates come down, then borrowing money gets cheaper. At the same time, if loans get longer, the total cost of a car then goes up.

Ultimately, it depends a lot on the car you want and the buyer you are. If you’ve got cash and you want something from a brand that’s trying to grow this year, then you might get a deal. If you’re financing a Tacoma, it might be a bit tougher.

Aston Martin Cuts 20% Of Staff

Source: Aston Martin

Source: Aston Martin

It’s been a while since I’ve driven an Aston Martin. I should fix that. Unfortunately for Aston Martin, the company sells many of its cars in the United States but does not build them here. Perhaps an Alabama Aston plant next year?

Blaming tariffs, the company is cutting.

Aston Martin, which has its headquarters in Gaydon, Warwickshire, employs about 3,000 people, meaning job losses will total around 600.

The firm said the job cuts should deliver annual savings of around £40m and did not specify when the job cuts would be implemented, but said most of the savings would be made this year.

A spokesperson for Aston Martin said US tariffs had been “extremely disruptive” and demand had also been “extremely subdued” in China, the world’s biggest auto market.

It has also trimmed its five-year capital spending plan to £1.7bn from £2bn by delaying investment in electric vehicle technology.

Clearly, the answer is to bring back the Cygnet.

Inside You, Are Two Nissan Pathfinders

Source: Nissan

Source: Nissan

The Nissan Pathfinder was once a stout body-on-frame SUV. Then it became a unibody blob. Now it’s a unibody car that looks like it could be a body-on-frame SUV.

Why can’t we have both?

According to Automotive News, that’s exactly what’s happening.

According to a person with knowledge of the plan, Nissan will continue selling an updated version of the unibody Pathfinder alongside a new body-on-frame model as soon as mid-2029.

This expanded Pathfinder lineup aims to target different buyer preferences: the unibody entry for those seeking affordability, car-like comfort and family practicality, and the truck-based variant for customers who demand a rugged aesthetic and greater capability.

The duration of the models overlapping in the market remains flexible and would depend on sales performance.

Will… will they both be called Pathfinder? That’s wild.

What I’m Listening To While Writing TMD

Have I really never done Paramore’s “Misery Business” for my TMD song? Hayley Williams remains undefeated in my book.

The Big Question

What’s the best example of a car or truck completely abandoning its customers from one generation to the next?

Top photo: Subaru/DepositPhotos.com