The Best Asset Allocation Entering Retirement

The trigger for this post was some recent reading on vacation in Belize.

Our morning view from the villa in Belize, March 2026.

With retirement just over a month away for me (with my wife already retired since 2025), I’ve been reading a bit more on this subject – more specifically, what might be an optimal asset allocation to enter retirement with – if there is one!?

I examine some options and reference some literature in today’s post, concluding with my own plan good, bad or indifferent. 🙂

First, a primer:

Asset allocation is the mix in your portfolio amongst different asset classes—primarily stocks, bonds, and cash for most—to balance risk and reward based on an individual’s goals, risk tolerance, and time horizon.

It is a central feature to portfolio management that helps minimize volatility and align investments to an investor’s personal long-term financial objectives.

That said, asset allocation can change over time, over an investor’s lifecycle and it probably should – including entering retirement. Consider the following options.

Option #1 – Use a Constant Equity Asset Allocation

One of the simplest strategies to enter retirement with might be using a single, all-in-one, asset allocation ETF across your registered accounts (i.e., RRSP/RRIF, LIRA/LIF) – and continue to maintain that fund for years on end.

Consider something like a “VBAL or XBAL or ZBAL and chill” approach in a 60% equities and 40% fixed income mix. The idea here is you simply sell off “BAL” units over time to fund your lifestyle at a modest withdrawal rate of 4-5% per year.

I know a few DIY investors that do this, very successfully.

I did a case study on my site about doing just that as well.

Can you retire using a 60/40 portfolio?

Selling off the capital you’ve accumulated is absolutely normal and fine and largely intended – why you saved money for retirement in the first place.

The challenge with this approach becomes what withdrawal rate to selloff at.

A withdrawal rate lower than 3-4% is likely too low over many years – your portfolio will just continue to grow and you are likely underspending in retirement. A withdrawal rate in the range of 4-5% is probably just fine. A withdrawal rate higher than 5-6% could put you at risk of outliving your money.

Simple solutions are great but eventually in retirement you need to get more tactical about what your portfolio can really deliver.

I’ll link to how I can help later on…

Option #2 – Use an Age-Based Equity Asset Allocation

Unlike option #1, this one is about using your age as an anchor.

Traditional retirement income planning looks like this:

Source: For illustrative purposes only. T. Rowe Price, August 2025.

This implies the following:

As you accumulate assets, the portfolio is heavily weighted towards equities. As we know by now, equities deliver higher volatility associated with stocks relative to fixed income but that’s the price you pay or have to stomach for long-term gains. As you age, get closer to retirement or start retirement, traditional thinking is you might follow an age-matches your bond or fixed income allocation formula. Traditional wisdom also says as retirement continues, the portfolio should glide-down in equities to be more conservative – with less time on your side to recover from bad market cycles.

More conventional thinking turns the tables on this below in option #3.

Option #3 – Use a Rising Equity Asset Allocation

If traditional thinking was about lower equites as you age, a rising equity glide path is the opposite: more equities as you age throughout retirement.

Because: investing doesn’t end when you retire.

A rising equity glidepath has demonstrated that a portfolio that starts out conservative and becomes more aggressive throughout retirement can deliver a few key benefits:

it can reduce the probability of long-term failure starting out with secure retirement spending, since higher fixed income is available to deliver the meaningful income desired by retirees by avoiding selling any equities at all during any market dips early in retirement, such that, by naturally increasing equity exposure over time you will earn greater capital appreciation in the latter, aging years of retirement, helping to combat inflation with any increased life expectancy.

The rising equity approach works well since if bad returns occur early in retirement (say in the first few years) the portfolio might otherwise be prematurely depleted by equity withdrawals.

So, lower up-front allocations to equities leave retirees less susceptible to a series of bad market returns for a few years.

Here a deep dive on rising equity glidepaths:

Should Equity Exposure Decrease In Retirement, Or Is A Rising Equity Glidepath Actually Better?

Here are two (2) key things to keep in mind when it comes to asset allocation in retirement, at least what I think about:

1. What do you need the money for, and when?

Saving for retirement is different than saving for a single expenditure like a Belize vacation: a one-time event. Figuring out what your annual retirement spend will forever be essential to income planning.

There is little value chasing a $1.7-million retirement number if you don’t need that much anyhow….

Canadians now need $1.7 million to retire

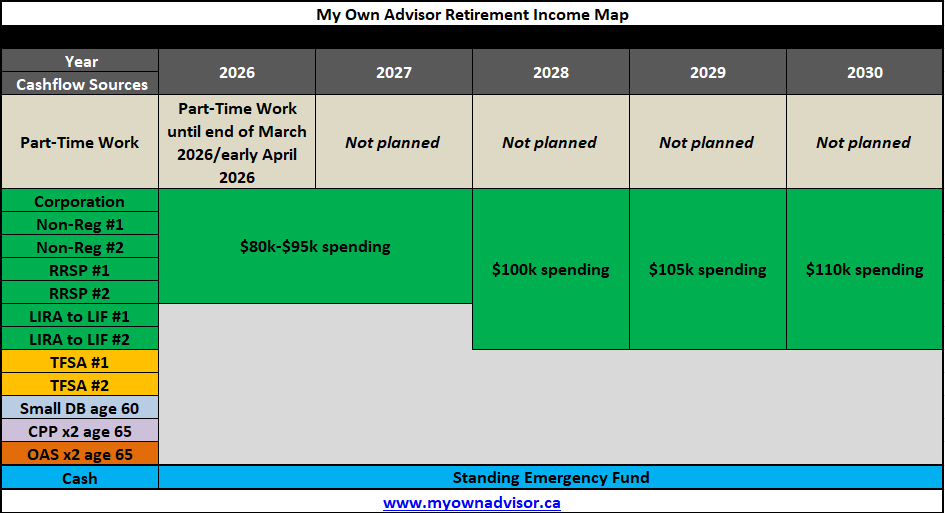

I’ve envisioned and therefore created a Retirement Income Map for my wife and I to forecast our first five (5) years of retirement spending needs. Your spending may be different. That’s OK. I would recommend you figure it out though.

(Five years’ worth of planning seems about right. Planning out what might happen 30 years from now for us is just far too much.)

Our Retirement Income Map.

2. What is your appeitite for risk?

If you have ample money and cashflow from your portfolio to retire comfortably – however you define “comfortably” – you can afford to take on more risk as any potential losses can be absorbed while you remain invested.

For some investors, annual cashflow via just dividends and distributions alone that exceeds annual expenses is ideal. While ideal, that’s also a lot of capital to get to that point that most retirees won’t need.

I/we always wanted the annual income/returns generated from our personal investment portfolio to be > annual expenses.

We use 5% annualized investment returns as our assumption for long-term portfolio returns.

We realized financial independence in 2024 with that return assumption in mind.

For most investors, they don’t know their risk tolerance until really bad market things happen and they change their approach.

I also can’t rely on 5% portfolio returns in any given year although that should be very doable over future decades.

So, we’ve determined we’ll hold cash/cash equivalents for spending 1-2 years’ in advance at all times.

You can see above in our Retirement Income Map I have a very good idea where our money is coming from for the next few years without selling or tapping any other assets at all…

The Best Asset Allocation Entering Retirement

Life does not end when you retire – at least I hope not!!

Asset allocation decisions entering retirement can be the following:

Use a constant equity allocation.Use a declining equity glidepath.Use a more modern-accepted rising equity glidepath.

A few months ago, I shared this RBC link:

Asset allocation in retirement – the “safest” option may surprise you – August 29, 2025 | Robin Gullason

Source: The Harbour Group.

“Determining an appropriate spending rate is one of the biggest challenges for new retirees. Spend too much, and one risks running out of money, severely tarnishing what should be the “golden years”. Those that spend less may find out that they could have retired earlier or dedicated more funds toward consumption when they were younger. Without perfect foresight around market returns, health span and life expectancy there is of course no right answer.”

That said:

The “safest” allocation turns out to be a typical growth-oriented asset allocation of 75% stocks and 25% bonds.

Do you need to have 75% equities and 25% fixed income to start retirement with?

Of course not.

Your asset mix (just like mine) will depend on:

Your investing time horizon.Your tolerance for risk/tolerance to accept losses near-term. Other dependable income sources for spending needs.

When it comes to us, we’re entering retirement next month with a 90% equity and 10% cash/cash equivalents/fixed income mix.

That higher 90% equity mix is full of dividend stocks and low-cost ETFs.

That 10% cash mix is for near-term spending – a mix in place to navigate remaining 2026 and 2027 spending in advance.

We will adjust and change our minds as things move forward I’m sure…no doubt. This is our asset allocation entering retirement.

I welcome your thoughts on this subject, anytime!!

When you entered retirement, what was your asset mix? If you are entering early retirement now like I am, what will be your asset mix?

Mark

Related Reading and Other Sources:

I’ve helped hundreds of DIY investors over the years via some low-cost retirement income projections – I am happy to help you too – providing all My Own Advisor readers with an instant 10% discount.

Here is a deeper dive on rising equity glide paths in retirement – a preferred, modern approach advocated by many experts.

Here is our bucket approach to generate retirement income.

My name is Mark Seed – the founder, editor and owner of My Own Advisor. As my own DIY financial advisor, I’ve reached financial independence. Now, I share my lessons learned for free on this site. Join the newsletter read by thousands every week.