Slowly unwinding a phenomenon that wrecked the housing market.

By Wolf Richter for WOLF STREET.

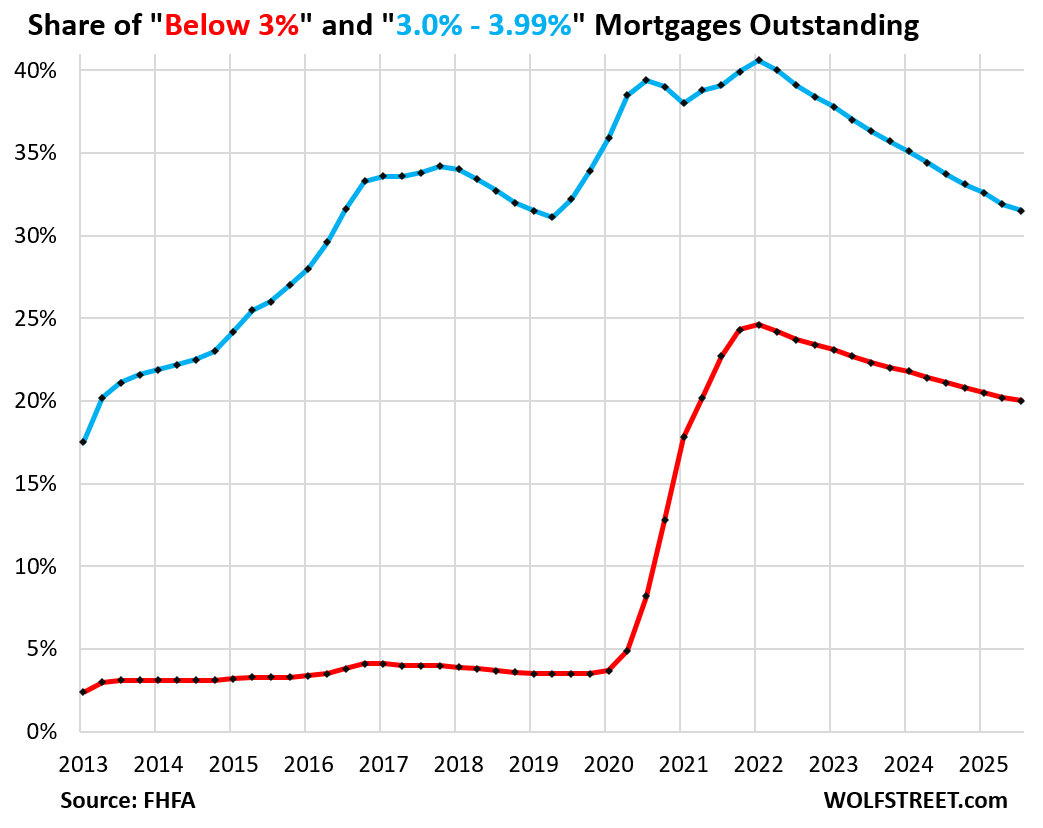

The share of below-3% mortgages outstanding, by number of mortgages, declined to 20.0% of all mortgages outstanding in Q3, the smallest share since Q1 2021, and down from a share of 24.6% at the peak in Q1 2022 (red in the chart), according to data by the Federal Housing Finance Agency (FHFA).

The share of below-3% mortgages had exploded from early 2020 through Q1 2022 when the Fed’s interest rate repression – via trillions of dollars of asset purchases, including mortgage-backed securities (MBS) and 0% policy rates – created a tsunami of homeowners refinancing their homes to get these new ultra-low interest rates.

The share of 3% to 3.99% mortgages declined to 31.5%, the smallest share since Q3 and Q2 2019, and beyond that, the smallest share since Q2 2016 (blue).

All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.

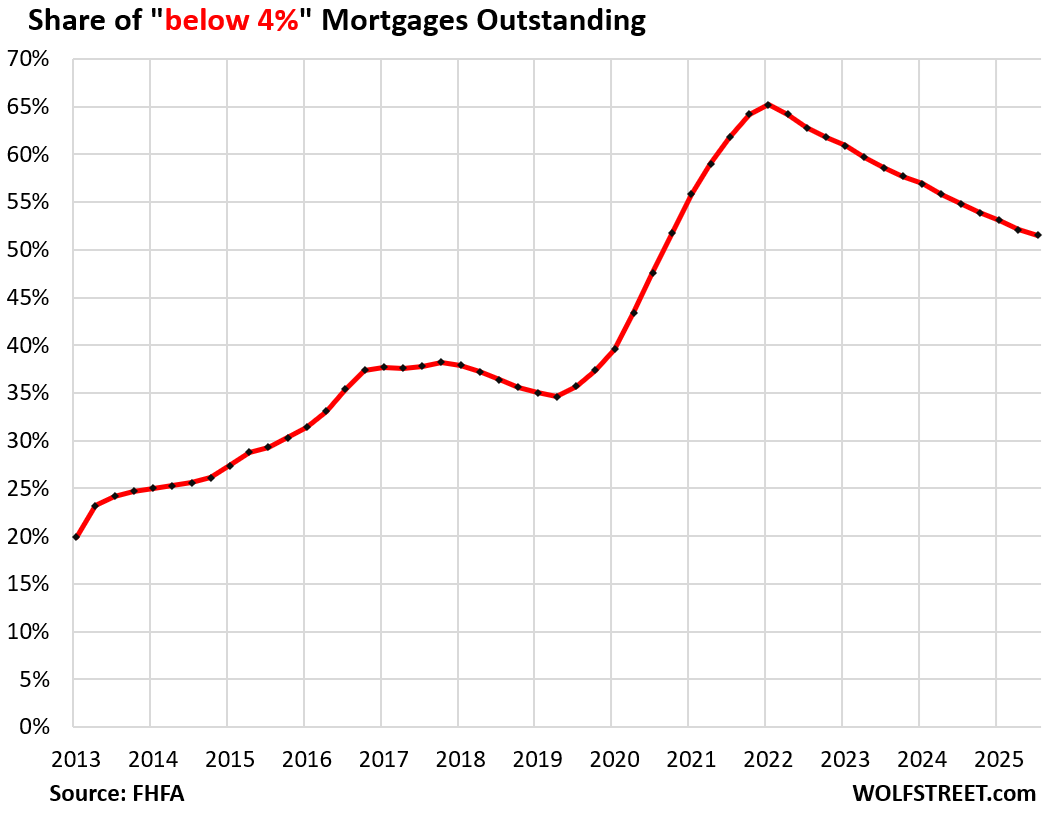

Combined, the share of below 4%-mortgages dropped to 51.5% of all mortgages outstanding, the lowest since Q4 2020, as homeowners, facing changes in life – new job in a different city, divorce, growing family, death, etc. – ever so reluctantly sell their home and thereby let go of these ultra-low interest-rate mortgages.

At the peak in Q1 2022, over 65% of all mortgages outstanding had interest rates below 4%.

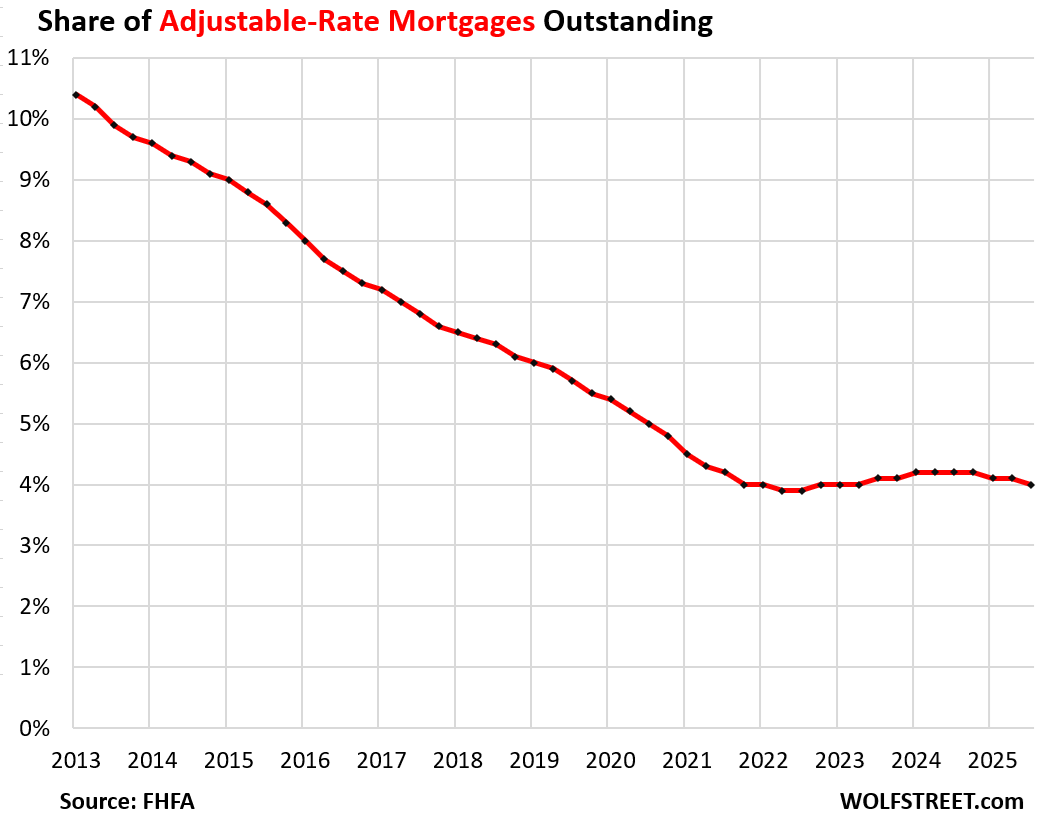

The share of Adjustable-Rate Mortgages has been hovering at low levels since 2021, and dipped in Q3 to 4.0%, down from over 10% in 2013, the extent of the FHFA’s data.

Some ARMs had rates below 3% even before 2020, which is one of the factors in why the below 3% mortgages (red line in the top chart) was between 2.5% and 4% before 2020.

Homeowners with ARMs that were originated when rates were low experienced payment shock when their mortgage rates adjusted as rates began to rise in 2022. But that payment-shock phase has mostly passed by now.

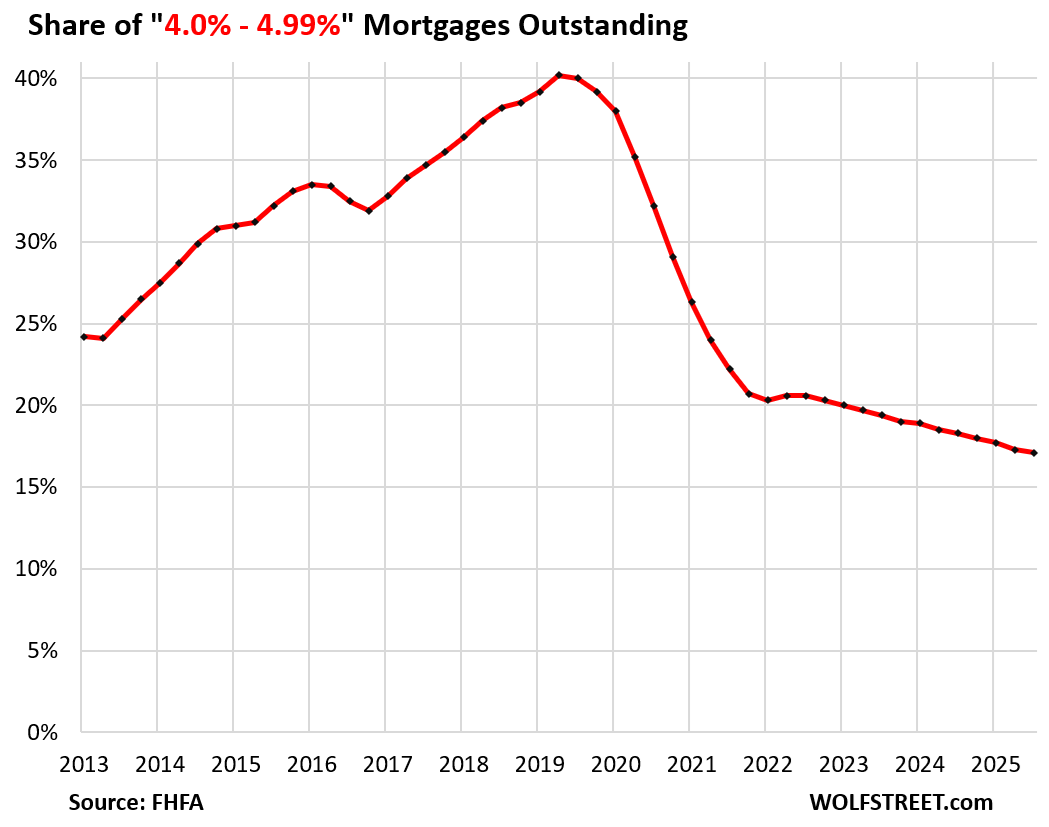

The share of 4.0% to 4.99% mortgages declined to 17.1%, the lowest share in the FHFA’s data going back to 2013, and down from the peak in 2019 of 40%.

When mortgage rates plunged in 2020, massive numbers of homeowners refinanced their mortgages into lower-rate mortgages – but not everyone could get a below-4% mortgage.

Homeowners who had qualified for mortgage rates between 4.0% and 4.99% before 2020 refinanced into the lowest-rate categories. But homeowners who had 6% or 7% mortgages before 2020, due perhaps to a tarnished FICO score, also refinanced into mortgages with sharply lower rates, but the lowest rates they might have had available were in this 4% to 5% range.

In other words, many homeowners refinanced out of this category in 2020-2022 and into lower rates, while a smaller number of other homeowners refinanced from higher rates into this category over the same period.

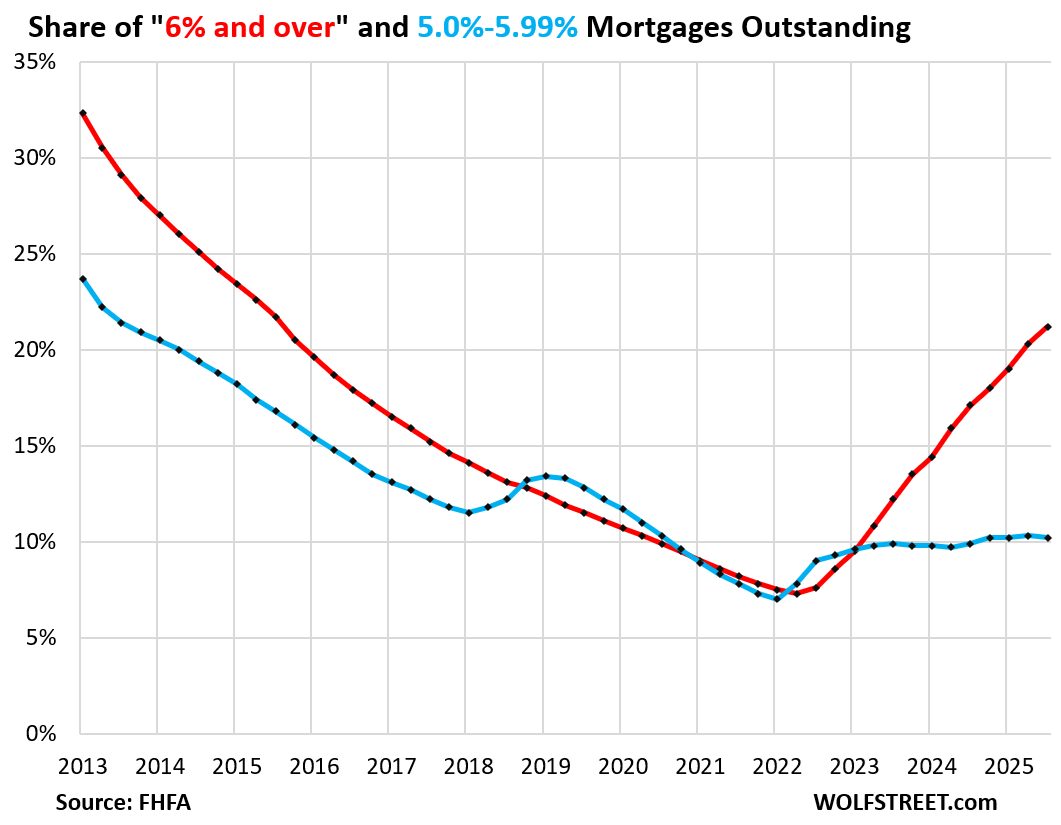

The share of 5.0% to 5.99% mortgages has remained roughly stable in 2023-2025, near 10% of all mortgages outstanding (blue in the chart below).

There are currently lots of fixed-rate mortgages offered in this range. For example, the interest rate of the average conforming 15-year mortgage was 5.44% in the latest week, according to Freddie Mac, but 15-year mortgages are not very popular.

The share of 6%-plus mortgages rose to 21.2% of all mortgages in Q3, the highest since Q3 2015, up from a share of 7.3% at the low point in Q2 2022 (red in the chart).

“Locked in” by Free Money. Below 3%-mortgages are free money in real terms because inflation is currently running at about 3%, and if borrowing costs run at the rate of inflation or below, it’s the equivalent of borrowing money at no cost … free money.

These ultra-low mortgages were a result of the Fed’s reckless monetary policies that caused home prices to explode in many markets by 50% and much more in just two years through mid-2022.

Those too-high home prices and ultra-low-interest-rate mortgages have now locked up part of the housing market – with those homeowners not selling and therefore not buying because they don’t want to finance a more expensive home with much higher interest rates.

This “lock-in effect” has haunted real-estate brokers, mortgage brokers, and mortgage lenders– as transactions and mortgage originations have plunged, and therefore income from commissions and fees has plunged, triggering waves of mass-layoffs and voluntary departures since late 2021.

Nevertheless, life happens – new job, return-to-the-office mandate, divorce, family additions, death, natural disasters, whatever – and so some of those “locked-in” homes with ultra-low-interest-rate mortgages get sold anyway, and the mortgages get paid off, and their share shrinks slowly, unlocking the housing market bit by bit.

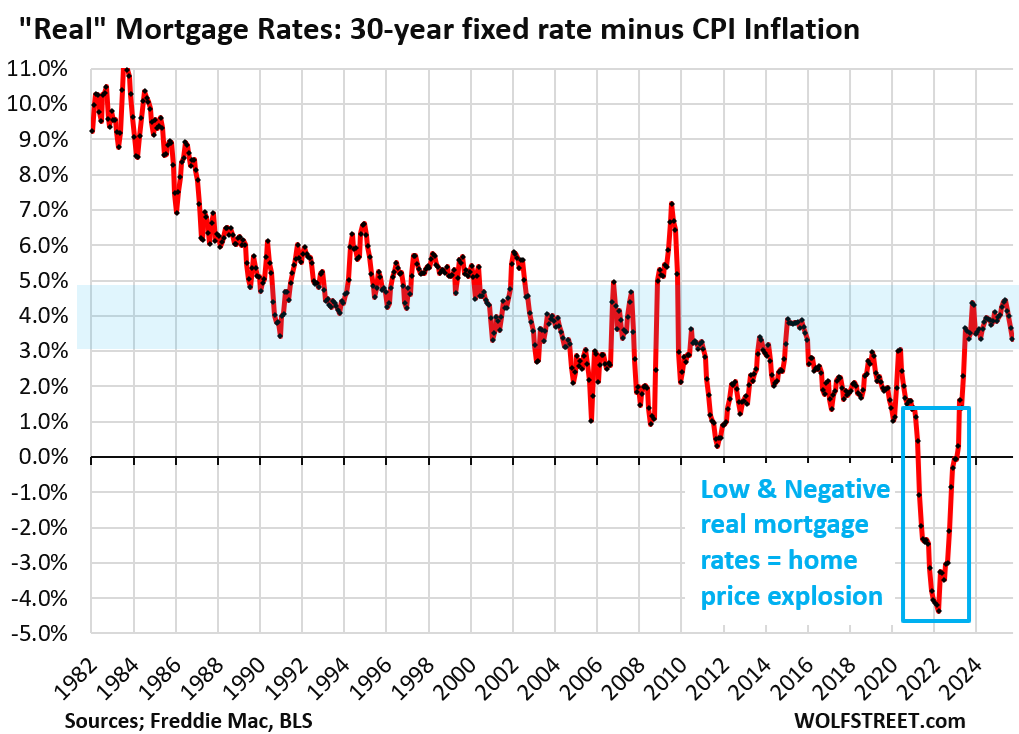

Just how crazy were those ultra-low mortgage rates? Between early 2021 through 2022, the average 30-year fixed mortgage rate was below CPI inflation – negative “real” mortgage rates – free money!

At the peak of the Fed’s craziness, “real” mortgage rates were 4 percentage points below CPI, with the average 30-year fixed mortgage rate below 3% and CPI inflation exceeding 7%.

Those were the craziest times ever in the mortgage market, and in the housing market, and those negative real mortgage rates wrecked the housing market through a historic home price explosion (now being unwound in many markets).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

WOLF STREET FEATURE: Daily Market Insights by Chris Vermeulen, Chief Investment Officer, TheTechnicalTraders.com.