Air Canada announced a new interline partnership with Pegasus Airlines, expanding connectivity through key European gateways into Turkey. The airline also detailed a larger summer schedule to Mexico, including new year round routes and higher frequencies on popular leisure corridors.

For investors watching TSX:AC, these route decisions come as the share price sits at about CA$19.25, with a 1 year return of 19.6% and a 5 year return showing a 31.1% decline. The mixed track record over 3 and 5 years highlights how sensitive the stock has been to shifting travel patterns and company specific execution.

Both the Pegasus tie up and the expanded Mexico schedule show how Air Canada is positioning its network around current demand. For you as a shareholder or potential investor, the key question is how effectively these new flows of traffic translate into more resilient passenger volumes and route economics over time.

Stay updated on the most important news stories for Air Canada by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Air Canada.

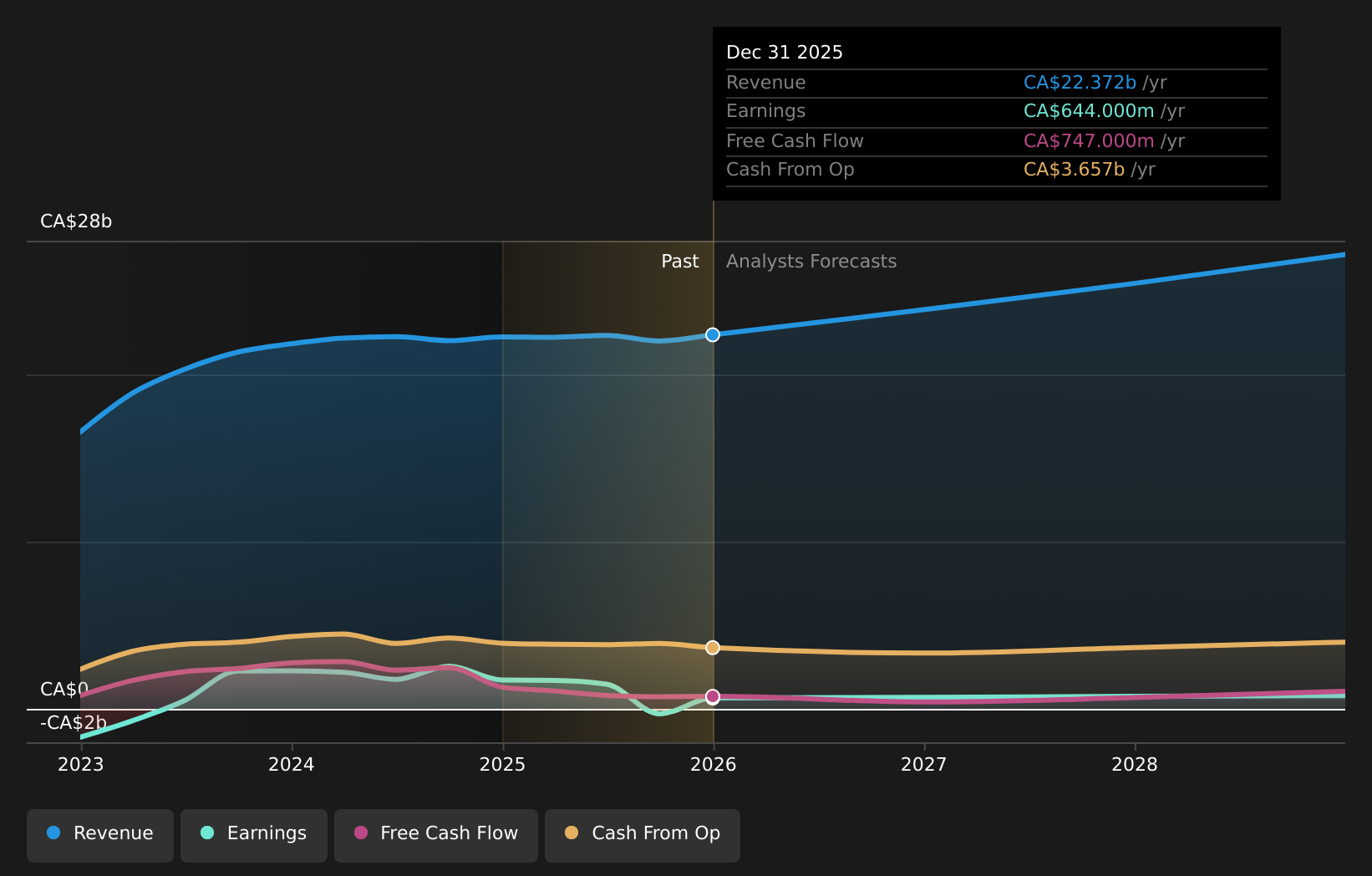

TSX:AC Earnings & Revenue Growth as at Mar 2026

TSX:AC Earnings & Revenue Growth as at Mar 2026

3 things going right for Air Canada that this headline doesn’t cover.

For Air Canada, both moves point to a tighter focus on where demand is currently strongest rather than simply adding capacity across the board. The Pegasus interline agreement plugs a gap in its Turkey coverage by giving access to Istanbul Sabiha Gokcen and Izmir via eight European gateways, without the capital and operating commitment of flying its own metal into those secondary points. That can support better aircraft utilization on core transatlantic routes while still capturing connecting traffic that might otherwise flow through European or Gulf carriers such as Lufthansa, Air France KLM or Emirates.

How This Fits Into The Air Canada Narrative The Pegasus partnership and extra Mexico capacity align with the focus on international network growth and sixth-freedom traffic mentioned in the existing narrative, potentially supporting load factors on long haul routes. At the same time, adding 18% more seats to Mexico could pressure yields if demand softens or competition from carriers like WestJet and Sunwing intensifies, which ties back to concerns about margin pressure. The potential move from interline to a full codeshare with Pegasus, including loyalty integration, is not explicitly covered in the narrative and could influence how Aeroplan contributes to recurring earnings.

Knowing what a company is worth starts with understanding its story.

Check out one of the top narratives in the Simply Wall St Community for Air Canada to help decide what it’s worth to you.

The Risks and Rewards Investors Should Consider ⚠️ Earnings are forecast to decline by an average of 1% per year over the next 3 years, so added capacity to Mexico could weigh on profitability if routes do not reach sustainable economics. ⚠️ Interest payments are not well covered by earnings, so any underperforming new routes or weaker pricing power on competitive leisure corridors may strain financial flexibility. 🎁 Analysts in good agreement that the stock price will rise by 32.7% see potential value in Air Canada expanding international flows, and the Pegasus tie up could support that if it drives steady connecting traffic. 🎁 Trading at what is described as good value compared to peers and industry, successful execution on these partnerships and route additions may strengthen the case that the market is pricing in too much caution. What To Watch Going Forward

You may want to track how quickly the new Montreal Guadalajara route and the higher frequencies to Cancun, Monterrey, Mexico City and Puerto Vallarta reach stable load factors and pricing, as that will indicate whether the extra 18% capacity is well timed. On the partnership side, watch for any move from interline to a full codeshare with Pegasus, including loyalty benefits, and whether Air Canada discloses growth in Turkey related traffic via its European hubs. Together with ongoing labour cost and debt service considerations, these metrics can help you assess whether route and partnership growth is supporting the long term earnings story for TSX:AC.

To stay informed on how the latest news impacts the investment narrative for Air Canada, head to the

community page for Air Canada to keep up with the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com