Bank of Montreal (TSX:BMO) reported strong first quarter results, with record revenue across several business segments. U.S. operations were a key contributor, supported by higher margin commercial lending and lower exposure to bad loans. The bank continued its share repurchase program, returning capital to shareholders while closing some branches to streamline operations.

For you as an investor, TSX:BMO sits at the crossroads of Canadian retail banking, U.S. commercial lending, and capital markets activity. Recent results highlight how the bank’s cross border footprint and business mix can influence earnings when management adjusts toward higher margin lending and tighter credit quality. The focus on U.S. growth and capital markets adds another layer of diversification beyond its traditional Canadian base.

Looking ahead, the combination of U.S. growth initiatives, capital markets contributions, and ongoing share buybacks gives you several levers to watch in upcoming quarters. How management balances expansion, branch rationalization, and capital returns will shape the risk and reward profile for shareholders following TSX:BMO’s progress.

Stay updated on the most important news stories for Bank of Montreal by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Bank of Montreal.

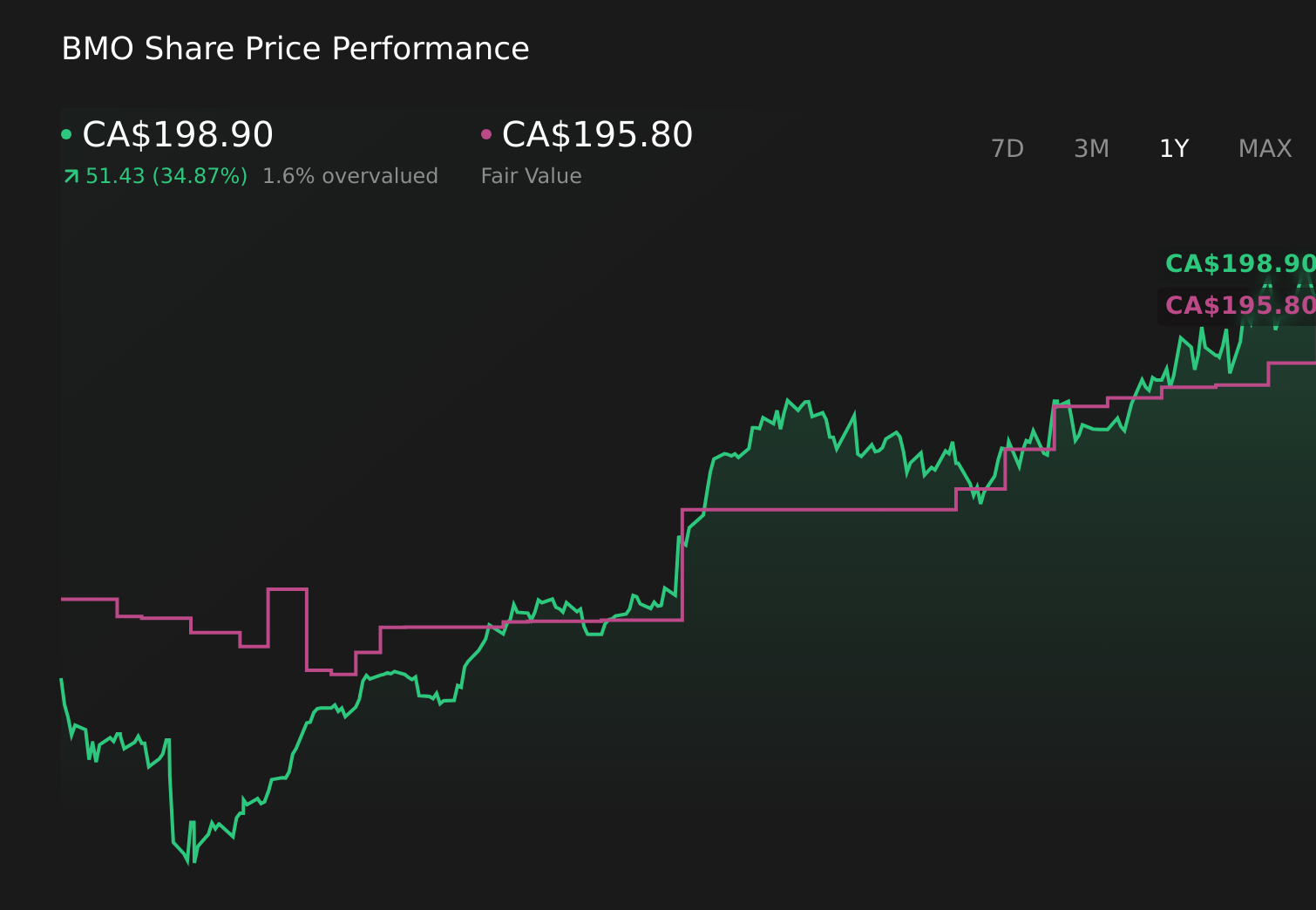

TSX:BMO 1-Year Stock Price Chart

TSX:BMO 1-Year Stock Price Chart

See which insiders are buying and buying and selling Bank of Montreal following this latest news.

Quick Assessment ⚖️ Price vs Analyst Target: At CA$198.90 vs a CA$205.60 target, the share price sits about 3% below consensus. ✅ Simply Wall St Valuation: Shares are flagged as trading roughly 28.2% below estimated fair value. ✅ Recent Momentum: The 30 day return of about 7.3% shows positive short term momentum into these results.

There are various ways to assess whether it is the right time to buy, sell or hold Bank of Montreal. Head to Simply Wall St’s

company report for the latest analysis of Bank of Montreal’s fair value.

Key Considerations 📊 U.S. growth, capital markets income, and active buybacks all contribute to how you might think about earnings quality and capital return at CA$198.90. 📊 Keep an eye on the P/E of 16.3 vs the banks industry average of 15.5, the 3.36% dividend yield, and how management deploys capital between U.S. lending, markets activity, and repurchases. ⚠️ One flagged issue is a relatively low 74% allowance for bad loans, which could matter if credit conditions weaken. Dig Deeper

For the full picture including more risks and rewards, check out the

complete Bank of Montreal analysis. Alternatively, you can check out the

community page for Bank of Montreal to see how other investors believe this latest news will impact the company’s narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Bank of Montreal might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com