The world is drowning in debt: Global borrowings hit a record high of over $324 trillion in the first quarter of this year, jumping by around $7.5 trillion in those first three months alone.

We’ve become so accustomed to the idea of excessive borrowing to cover excessive expenditure that we’ve lost sight of just how unsustainable the level of both private and public spending is: and we’ve also lost sight of the fact that debt must be repaid.

That might be because global debt now involves bewilderingly large sums of money. Are we even cognisant that every trillion borrowed is a million million dollars, and the Gross Domestic Product of the entire world in 2024 – coming in at €111 Trillion according to the World Bank – was less than one third of total global borrowing?

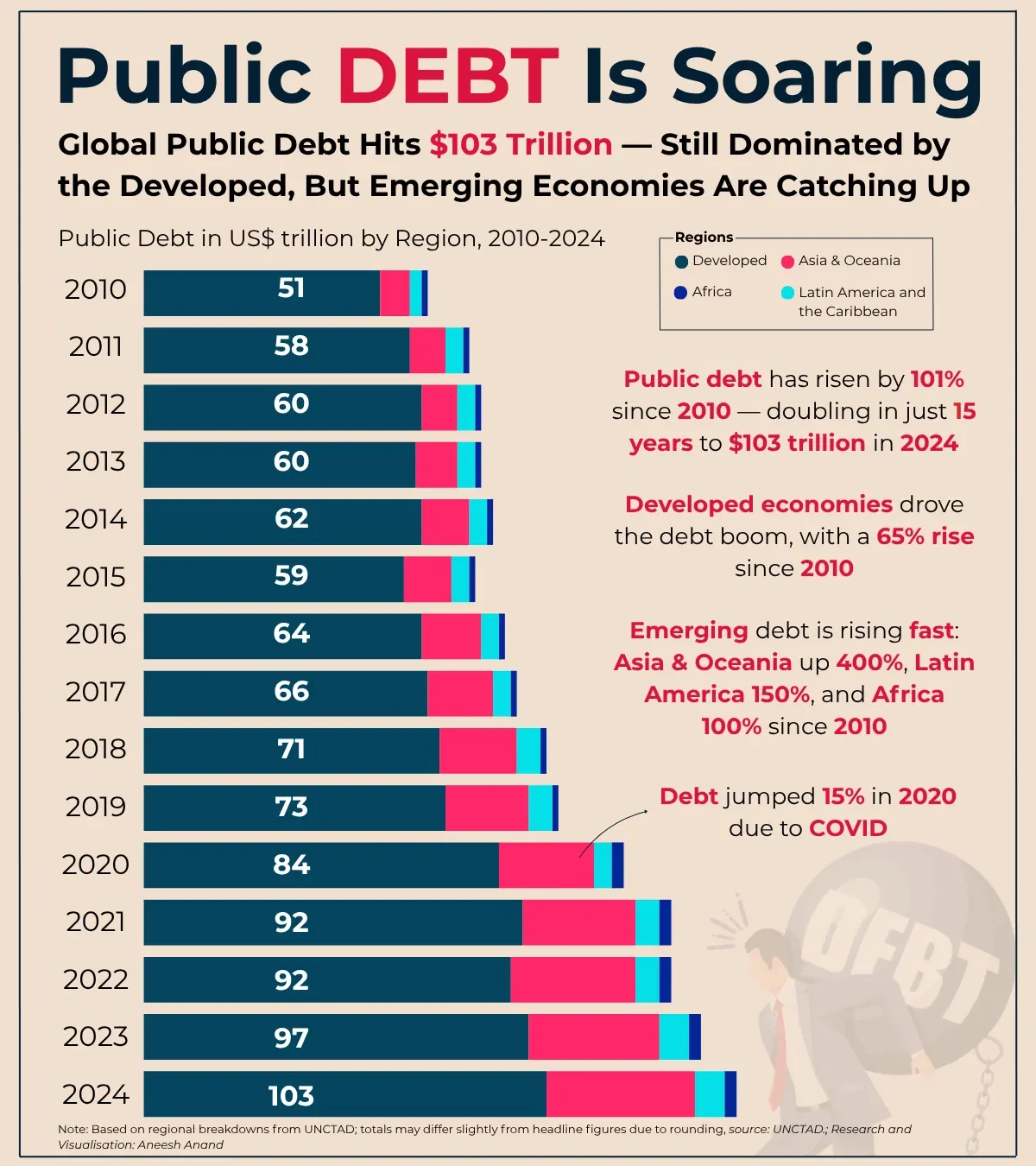

Global public debt – the amount to which nations are indebted – continues to soar, and hit €103 Trillion by the end of 2024. The alarming trend is captured in this graphic from United Nations Conference on Trade and Development which shows that public debt doubled in just 15 years, with debt of emerging countries – especially in Asia – rising fast, while developed economies continue to become more and more indebted, mostly due to ever-accelerating government spending.

In what are now called emerging countries, that increased debt intake comes with a heavy cost as they are far more likely to pay crippling interest rates, in some cases being then forced to divert funds from essential services to cover debt repayment and interest costs.

But developed economies are also ridiculously indebted. As shown above, the Covid lockdowns saw public debt leap 15%, and that was followed by a sustained period of higher interest rates after years of cheap loans and low yields on government bonds. Yet governments, including our own, kept spending like there is no tomorrow. In fact, the lavish spending during Covid – to effectively try to compensate for the absurd length of time that the economy, and everything else, was placed on pause – seems to have lowered the bar when it came to fiscal prudence, with Irish public spending up 50% since before the Covid panic, a pattern also seen elsewhere.

We’ve felt cushioned from the obvious effects of increasing spending beyond our actual means by the corporation tax from multinationals which has filled our coffers until now – relying on the precarious position where just ten firms account for about €1 in every €8 of all tax revenue. The writing is on the wall, however, in regard to that particular income source, and, as I have written previously, the Irish Fiscal Advisory Council has shown that, without the now-unreliable corporation tax from global corporations here for tax purposes, the country’s finances are running at a huge deficit each year.

We are not alone in that. The sovereign debt of the United States, reached a staggering $30.3 trillion at the end of the second quarter of 2025 is a result of persistent deficits – when the government spends more in a year than it receives in revenue. As goes the U.S., goes the world: and out of control spending under successive administrations means that, as with the global situation, the nation’s debt previously matched and has now overtaken the entire U.S. economy.

Gross domestic product (GDP), the sum of all goods and services produced by the U.S. economy, was $30.3 trillion at the end of the second quarter of 2025 (June 30), according to the latest estimate by the Bureau of Economic Analysis (BEA). That means the debt, which stood at $36.2 trillion at the end of the second quarter, was 119.4% of GDP.

The same story can be seen across Europe. In 2024, all EU member states, with the exception of 6 countries, reported a deficit – and in 12 countries the deficit was higher or equal to 3% of GDP, a threshold set by the Stability and Growth Pact (SGP) to ensure fiscal stability. Additionally, the overall debt of Eurozone countries is now dangerously close to the GDP of same, having grown significantly since 2000. The latest figures show that the Eurozone public debt to GDP ratio has significantly increased in that time, rising to 87.4% by the end of 2024.

(In regard to Ireland, previously, my colleague Matt Treacy, in looking at figures for 2022, observed an enormous difference in our artificially inflated GDP and GNI for this country that year: GDP for 2022 was €500 billion while GNI was €360 billion, he observed – a huge difference of €140 billion or 28%. So, while our GDP to debt ratio at that time looked healthy, in fact the ratio that actually mattered – the ratio of public debt to our GNI – was a different story entirely at 86%, equal to a per capita debt of €44,250 for each person living in the state.)

This endlessly accumulating debt pile now seems to be bringing some of the world’s most established economies to the natural conclusion we’d all expect if we persistently lived beyond our means. The kind of borrowing for emergencies such as the 2008 financial crash and the (ridiculously long) Covid lockdowns became the norm. But highly-indebted countries, like highly indebted people, are eventually all too often heading towards a point of crisis. An addiction to borrowing can really only lead to a sorry end.

Much of the excessive borrowing is, of course, because of the short-term need of politicians to keep voters happy. Printing money – just a way of borrowing – and ratcheting up spending might ensure politicians keep their seats, and keep politicial parties in power, but it is a delusional way to manage public and private finances. Voters demand ever-increasing services and resources, governments borrow to keep voters happy, the cost of living is driven up by this reckless, inflation-boosting spending, and the spiral has to come crashing down at some point.

This spiralling public debt scenario is also reflected in private and personal debt, and the delusion is the same everywhere, with the situation exacerbated by mismanagement of public services by the same governments addicted to profligate spending. There seems to no sense of reality in how many of us live our lives. We expect a Kim Kardashian lifestyle on Tesco wages, and we’ll get the cards maxed out to the hilt to facilitate that. At some point, the whole pretence has to come crashing down.

Hence the headlines regarding the possibility of an IMF bailout for both the UK and France, which would be a disastrous outcome, not just for the government, but for the economy and, of course, the citizens of those countries. The Telegraph says that economists have said the current handling of the British economy “risks a return to the years of high inflation and borrowing that ended with Britain being forced to borrow billions from the International Monetary Fund (IMF) 50 years ago.”

They point to a £50bn black hole in the proposed Budget, caused by “rampant borrowing”, and quote one economic expert, Prof Jagjit Chadha, as saying that the economy is at risk of collapse, and another as predicting that the UK would not be able to roll over debt. Bond yields have soared: meaning that the British government is forced to pay higher interest rates to those willing to lend, and this week the long-term cost of borrowing hit its highest level since 1998. None of this is really high finance: if you keep maxing out credit cards and taking out loans while your ability to repay isn’t improving, you’ll be forced to pay higher interest rates too.

Other sources say the IMF bailout talk is hysteria. But with the rising cost of borrowing, the likely alternative is increasing taxes if governments won’t cut spending – though perhaps spending more efficiently instead of pouring money into NGOs, for example, might be an another option.

And the headlines aren’t confined to Britain. France’s long-time overspending problem is also being punished by the bond markets – and France’s record public debt ratio, at 113% of GDP, is even worse than Britain’s, plus their budget deficit for the current year looks set to reach 5.5% of GDP. Almost 15 % of France’s annual economic output is being spent on pensions and that situation is about to worsen, and not just in France.

The IMF is a lender of last resort. Will the UK and France be forced to go cap in hand for help? The next few months may see turbulent times? But what is certain is that most developed countries have unsustainable borrowing and spending habits and a correction is looming if not inevitable.

Finally, much of the largesse we’ve seen in developed countries has been driven by ideological commitment to spending – such as the hundreds of billions thrown at green energy and initiatives. Now EU leaders want similar sums spent on defence, as if money is actually growing on trees. Defence commitments are being talked up at the same time that bond yields are rising. And coming down the tracks like a train is the certain demographic crash that will see a sustained and irreversible shrinking of economies.

It’s not looking good, to be honest. And if we think we can spend our way out of this particular concatenation of circumstances, we are completely deluded. We are drowning in debt, and need a rescue plan.