Launch in 2028: CPF Board will introduce a voluntary life-cycle option under the CPF Investment Scheme for members willing to take some investment risk.Auto rebalancing: Portfolios will shift to lower-risk assets over time, with proceeds supporting payouts under CPF LIFE.Low-cost, limited options: Two to three providers will be appointed, with capped all-in fees.

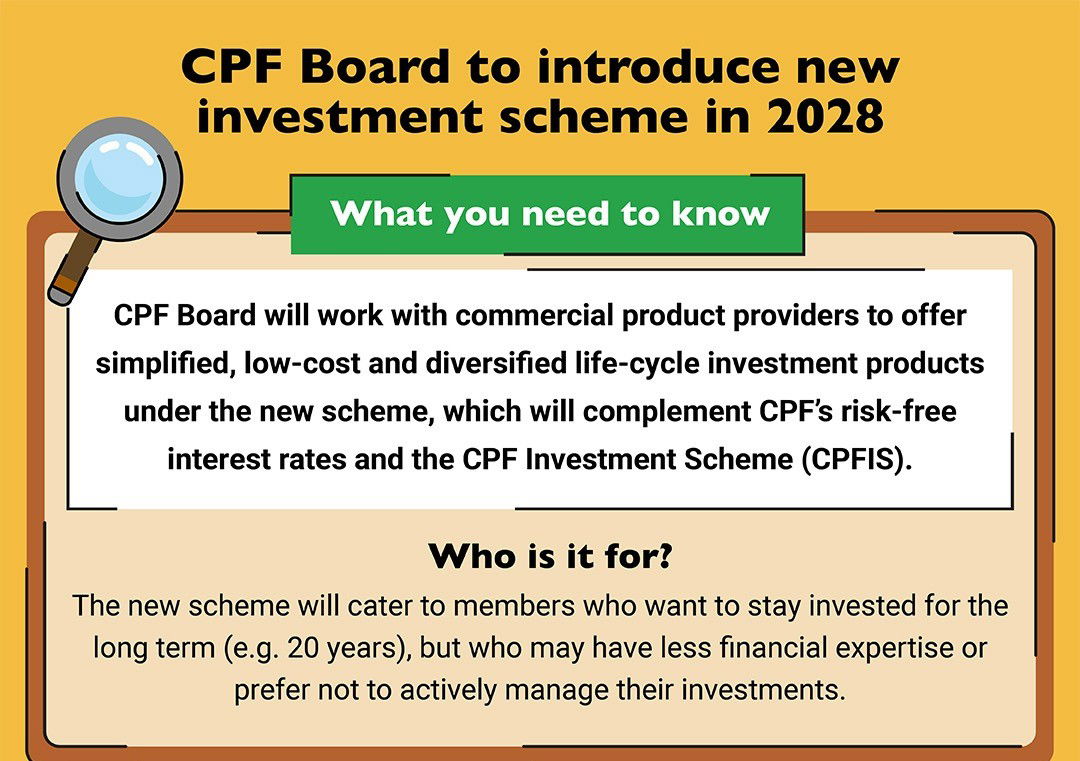

The Central Provident Fund (CPF) Board will introduce a new investment scheme in 2028, following the CPF Advisory Panel’s recommendation for a Lifetime Retirement Investment Scheme.

For members with investible savings, the CPF Investment Scheme (CPFIS) currently offers the option to invest CPF savings in a wide range of instruments.

The new scheme will complement the existing system. It is aimed at long-term investors who are willing to take some investment risk for potentially higher returns, but who may have less expertise in navigating CPFIS offerings or prefer not to actively manage their investments. Participation will be voluntary.

Simplified, low-cost lifecycle products

Under the new scheme, CPF Board will work with commercial product providers to offer simplified, low-cost, and diversified lifecycle investment products.

These products will automatically rebalance investors’ portfolios towards lower-risk assets as they approach a target date, typically retirement. This means portfolios will shift gradually from higher-risk assets such as equities to lower-risk assets such as bonds over time.

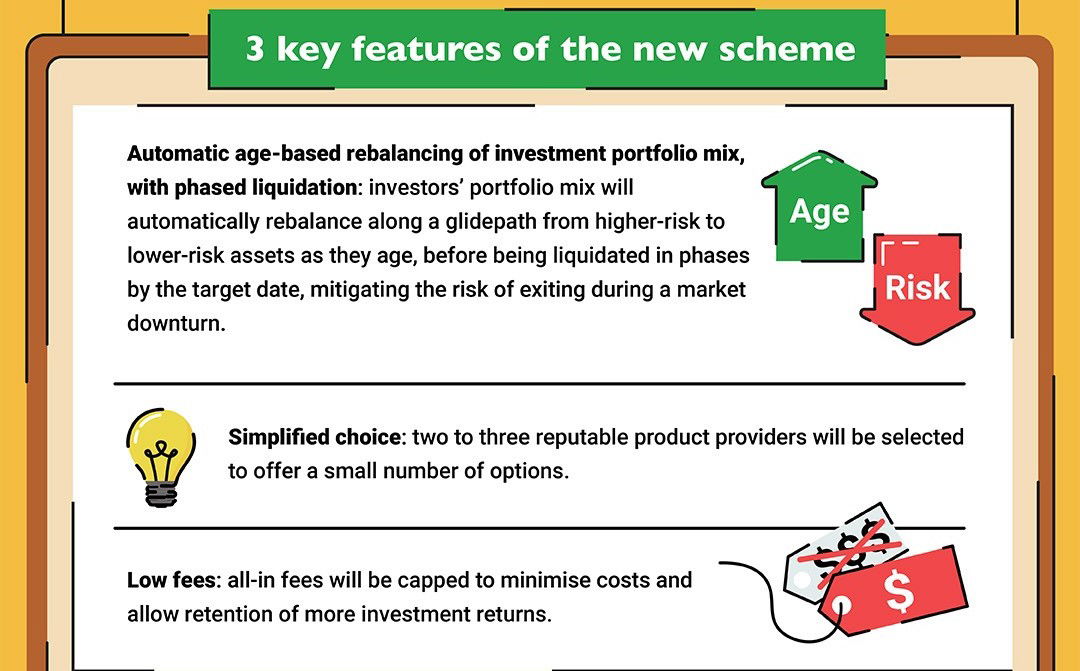

The automatic age-based rebalancing follows a glidepath approach. As members grow older, their exposure to investment risk will be calibrated to reflect their life stage. Portfolios will also be liquidated in phases before the target date to mitigate the risk of a market downturn during exit.

For example, if the target date is the payout eligibility age of 65, the portfolio could be liquidated progressively in the years leading up to that age.

Upon phased liquidation, investment sale proceeds will be transferred to the member’s retirement account (RA), up to the full retirement sum (FRS). Any remaining proceeds will be transferred to the ordinary account (OA). Funds in the RA can then be used to join CPF LIFE when the member chooses to begin monthly payouts from age 65, helping to boost retirement income.

Fewer options, capped fees

To simplify decision-making, CPF Board is looking to appoint two to three reputable product providers to offer a small number of options under the new scheme.

All-in fees will be capped to minimise costs, enabling investors to retain more of their returns.

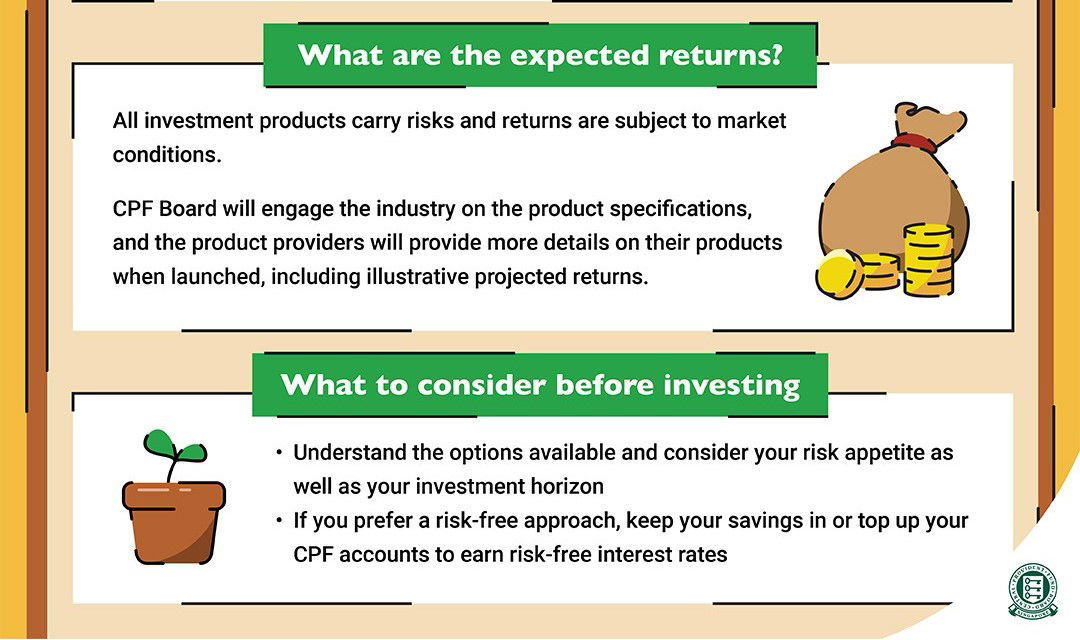

As with all investment products, returns are subject to market conditions and investment risks. CPF Board will engage the industry on detailed product specifications. Selected product providers will share further details, including illustrative projected returns aligned with the risk profile of their products, when the scheme is launched.

Why introduce the scheme now?

CPF Board said market developments have made it timely to introduce lifecycle investment products to CPF members.

Lifecycle products are designed to automatically adjust an investor’s asset allocation along a glidepath as the investor approaches a target date, typically retirement. Technological advancements and the growth of digital investment platforms may enable commercial providers to offer such products at more affordable costs.

Based on market studies, lifecycle investment products show potential to achieve good returns over the long term. Adoption of these products has also increased internationally in recent years.

Industry engagement from 2026

CPF Board will begin engaging the industry from March 2026 on product specifications and will invite expressions of interest from providers keen to offer such products.

Similar to the fund selection process for CPFIS, CPF Board will work with independent investment consultants to evaluate applications. Selected providers are expected to be announced in the first half of 2027. The new scheme is scheduled to launch in the first half of 2028.

While the products will be provided and managed by commercial product providers, the government is prepared to provide time-limited support to help kick-start the scheme. It will also support interested members in understanding how the new scheme works and whether it is suitable for them. Further details will be announced later.

Considerations for members

The government noted that CPF members have diverse financial goals and risk preferences.

Members who prefer a risk-free approach can continue to keep their savings in their CPF accounts to earn CPF interest rates. They may also consider cash top-ups or transferring OA savings to their Special Account to boost future monthly payouts under CPF LIFE.

For members who are willing to take some investment risk, the new scheme will provide an additional option alongside existing choices under CPFIS. Existing CPFIS eligibility criteria will apply.

Launch in 2028: CPF Board will introduce a voluntary lifecycle option under the CPF Investment Scheme for members willing to take some investment risk.

Auto rebalancing: Portfolios will shift to lower-risk assets over time, with proceeds supporting payouts under CPF LIFE.

Low-cost, limited options: Two to three providers will be appointed, with capped all-in fees.

Members are encouraged to understand the options available and consider their risk appetite and investment horizon before deciding to invest their CPF savings.

Infographic / SG Press Centre