Personal savings dropped from 6.2% in early 2024 to 4.2% by mid-2025 while Social Security approaches insolvency.

Social Security replaces roughly 40% of pre-retirement earnings. Benefit cuts will compound annually with 2.16% inflation.

Delaying claims past full retirement age increases benefits by 8% per year until age 70.

A recent study identified one single habit that doubled Americans’ retirement savings and moved retirement from dream, to reality. Read more here.

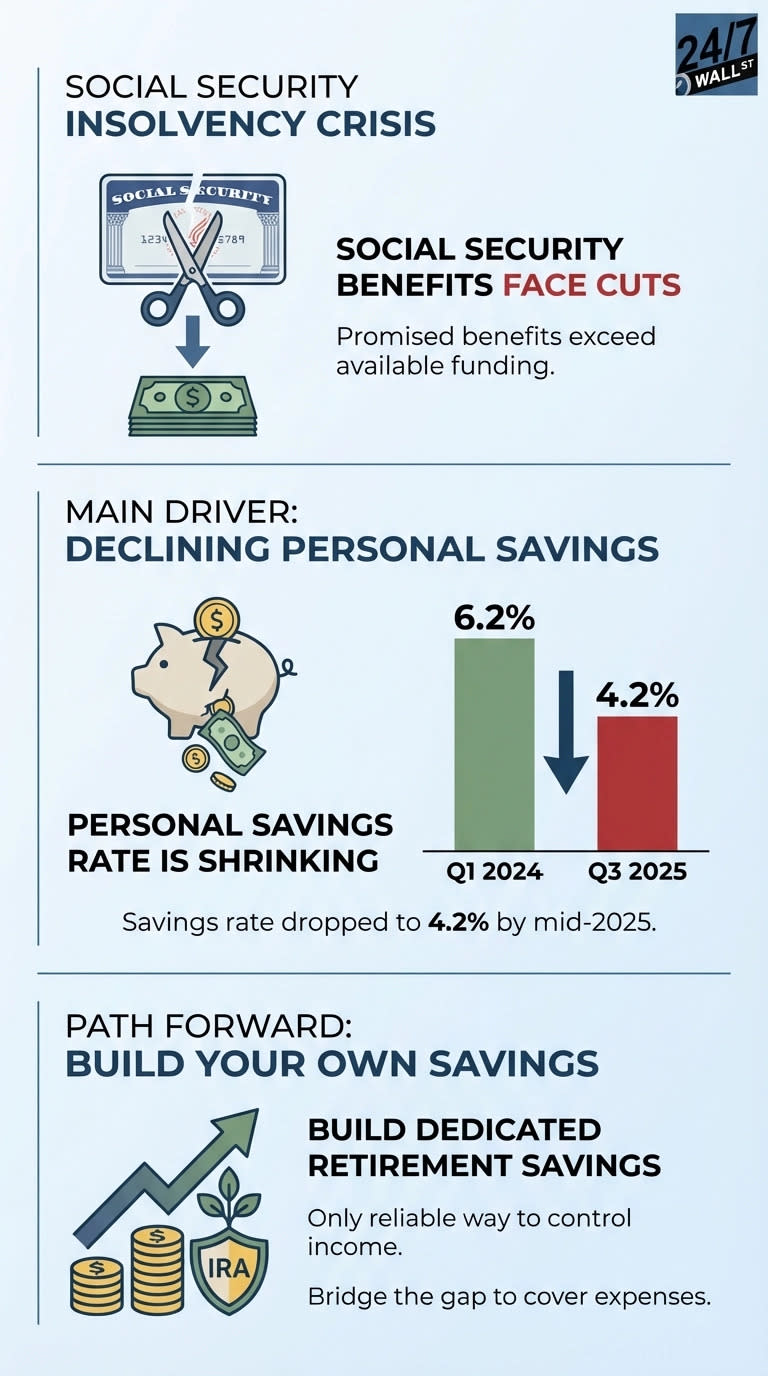

Social Security’s trust fund faces a critical deadline that most Americans aren’t prepared for. The 2025 Trustees Report shows the system approaching a fundamental shift in how benefits are paid. Instead of drawing from accumulated reserves, the program will transition to paying benefits directly from incoming payroll taxes, a change that means promised benefits will exceed available funding.

American households are entering this crisis unprepared. The personal savings rate has dropped from 6.2% in early 2024 to just 4.2% by mid-2025. This decline reflects families struggling with rising costs and stagnant wage growth, leaving them with no financial buffer when benefit cuts arrive. The timing creates a perfect storm: reduced Social Security income hitting households that have already depleted their savings.

24/7 Wall St. · 24/7 Wall St.

24/7 Wall St. · 24/7 Wall St.

As Social Security benefits face cuts due to insufficient funding, a declining personal savings rate highlights the urgency for individuals to build dedicated retirement savings.

Social Security was never designed to be anyone’s sole retirement income. It currently replaces roughly 40% of pre-retirement earnings for average workers. The real risk isn’t that benefits disappear, but that they shrink when you’re already retired with limited ability to adjust.

Social Security was designed to replace about 40% of pre-retirement earnings, never intended as a complete solution. But the real danger lies in how benefit cuts compound over time. With inflation running at 2.16% annually, each year of reduced benefits erodes purchasing power further. A retiree facing a 20% benefit cut doesn’t just lose that amount once—they lose it every year, and inflation makes each dollar worth less, creating a growing lifetime shortfall that becomes impossible to recover from on a fixed income.

Maximize earnings now. Social Security calculates benefits using your highest 35 years of inflation-adjusted earnings. Each additional year of higher income can replace a lower-earning year, directly increasing your benefit base before any cuts apply.

Build dedicated retirement savings. The gap between what Social Security promises and what it can deliver is widening. Contributing to a 401(k) or IRA isn’t optional—it’s the only reliable way to control your retirement income. Even modest increases matter: consistent additional contributions over time can build substantial reserves.

Delay claiming if possible. Every year you wait past full retirement age increases your benefit by 8%, up to age 70. That boost applies before any insolvency cuts, giving you a larger base to work from.

Plan for reduced income. Don’t assume full scheduled benefits when modeling retirement. Build a buffer into your planning to account for potential benefit reductions. This creates protection if cuts happen and leaves upside if Congress fixes the shortfall.

Check your Social Security statement at ssa.gov to see your projected benefits. Then calculate what a reduced amount would actually cover in your budget. The gap between that number and your expected expenses is what you need to fund through savings.

Most Americans drastically underestimate how much they need to retire and overestimate how prepared they are. But data shows that people with one habit have more than double the savings of those who don’t.

And no, it’s got nothing to do with increasing your income, savings, clipping coupons, or even cutting back on your lifestyle. It’s much more straightforward (and powerful) than any of that. Frankly, it’s shocking more people don’t adopt the habit given how easy it is.