In late February and early March 2026, International Business Machines Corporation expanded its board to fourteen directors with the election of Ramon Laguarta and announced new AI-focused partnerships and contracts, including a US$112.00 million Defense Commissary Agency deal to modernize electronic shelf labels worldwide.

Together with the Deepgram voice-AI integration into watsonx Orchestrate and ongoing quantum and data-integration advances, these moves underscore IBM’s intent to anchor its future around enterprise-grade AI, hybrid cloud, and research-intensive computing.

With these AI partnerships and government wins in mind, we’ll now examine how the news flow reshapes IBM’s investment narrative.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

To own IBM today, you need to believe the company can turn its enterprise-grade AI, hybrid cloud, and quantum research into durable, high-margin software and services, while managing debt and legacy mainframe exposure. The recent AI partnerships and federal wins appear supportive of IBM’s near term AI and z17 adoption catalyst, but they do not materially change the immediate risk that faster moving AI competitors could pressure consulting and mainframe related work.

Among the latest announcements, the US$112.00 million Defense Commissary Agency contract stands out as most relevant. It reinforces IBM’s position in mission critical government infrastructure, a segment closely tied to its hybrid cloud and AI catalyst. While the ESL deal is modest next to IBM’s US$67.54 billion in annual revenue, it illustrates how AI, data integration, and services can bundle together in long duration contracts that support the broader enterprise AI investment case.

Yet, beneath IBM’s AI momentum, investors should also weigh the risk that accelerating AI tools could erode parts of its high value mainframe and consulting franchise…

Read the full narrative on International Business Machines (it’s free!)

International Business Machines’ narrative projects $74.4 billion revenue and $10.5 billion earnings by 2028. This requires 5.1% yearly revenue growth and a $4.6 billion earnings increase from $5.9 billion.

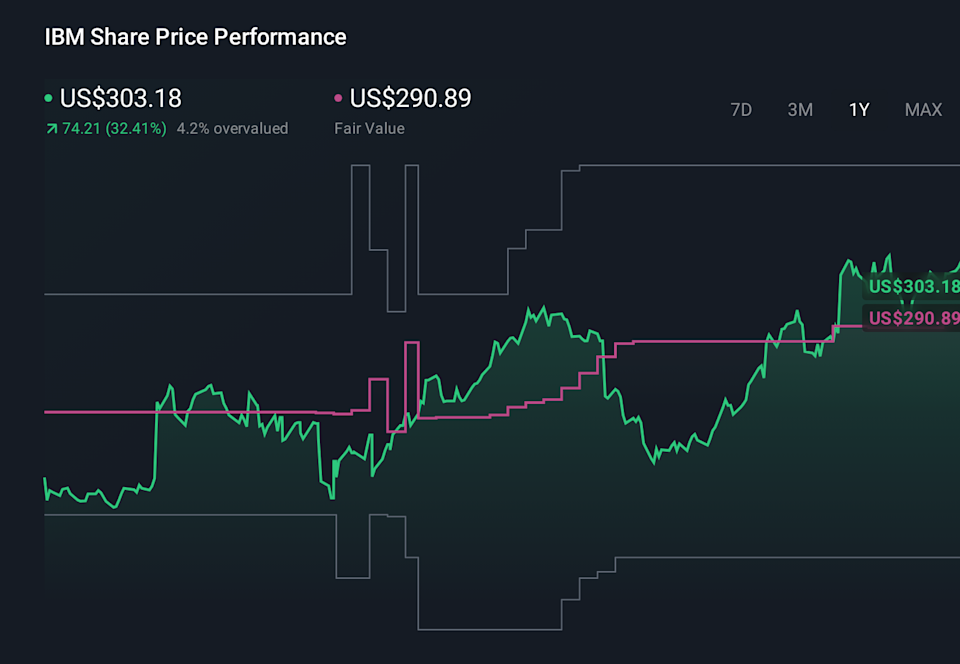

Uncover how International Business Machines’ forecasts yield a $302.05 fair value, a 18% upside to its current price.

IBM 1-Year Stock Price Chart

IBM 1-Year Stock Price Chart

Before this news, the most optimistic analysts were modeling IBM revenue at about US$76.6 billion and earnings of roughly US$12.1 billion by 2028, a far more upbeat view than consensus that also assumes legacy pressures and high debt stay manageable. The new AI contracts and partnerships could either support that bullish case or expose its limits, which is why it is worth comparing how your own expectations line up with these very different narratives.

Explore 14 other fair value estimates on International Business Machines – why the stock might be worth as much as 52% more than the current price!

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include IBM.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com