Industrial automation is nothing new. Rockwell Automation has given factories a means of controlling the speed of their electric motors since 1903, while Zebra Technologies has been around since 1969, first launching as a maker of electromechanical solutions but making a name for itself in the 1980s by pioneering and then perfecting the scannable bar codes that now seem to be printed on, well, almost everything.

But just when it seemed as if efficiency-creating technology had reached the limits of its capabilities, the advent of artificial intelligence (AI) has turned automation that was once unthinkable into the possible. And one company in particular is poised to win more than its fair share of the industry’s annualized growth of 17% that Opto Foresight anticipates through 2035, when the industry should be worth more than $375 billion per year. That company is Symbotic (SYM 1.55%). Here’s why.

What’s Symbotic?

Symbiotic is not a household name. There’s a good chance, however, you or someone in your household regularly benefits from its tech.

See, Symbotic makes AI-powered robotics specifically for warehouses that house and handle a high-volume of consumer goods. The company’s biggest customer is Walmart, if that tells you anything. The retailer uses its solutions in its warehouses used to fulfill customers’ online orders, as well as to handle the distribution of goods to its stores.

The chief goal is efficiency, of course. While advanced robotics may not be a cost-effective option for smaller operations, at a scale of more than $700 billion in annual revenue, Walmart’s investment in high-capacity, near-perfect, constant-uptime automation like this will readily pay off.

Today’s Change

(-1.55%) $-0.84

Current Price

$53.20

Key Data Points

Market Cap

$6.7B

Day’s Range

$51.57 – $54.57

52wk Range

$16.32 – $87.88

Volume

27K

Avg Vol

2M

Gross Margin

18.90%

Just bear in mind that while Walmart is this company’s biggest customer, as well as a major shareholder, that’s hardly the end of Symbotic’s growth opportunity. As big as Walmart is, it still only produces less than one-tenth of the United States’ total retail spending (more in groceries, less in general goods), while the Bureau of Economic Analysis reports that retailing itself only accounts for less than one-tenth of the United States’ total GDP. There are plenty of other industries like manufacturing or logistics, or even farming or waste management, that could eventually be handled by Symbotic’s artificial intelligence-powered platform, which currently combines articulated arms with self-driving pallet movers. This retail-minded technology could be adapted in a number of ways, some of which have yet to be foreseen.

Proven practicality, with the reward on the near horizon

It’s not the only name in the nascent AI robotics business, for the record, nor is its tech the stuff of the artificial intelligence robotics revolution’s most scintillating stories. That honor still arguably belongs to Tesla’s Optimus, which is a human-shaped and human-sized automaton expected to be doing chores in peoples’ homes by the end of next year, if chief executive Elon Musk can meet his own timeline target.

That being said, it’s worth mentioning that some lesser-known companies, including Agility, 1X, Apptronik, and Boston Dynamics, are just some of the company’s also developing general-purpose AI-directed humanoid robots, a handful of which are already in use, while others seem to be at least as far along in their development as Tesla’s Optimus is.

Image source: Getty Images.

Then there are the other makers of more practical automation solutions needed right now, such as Teradyne or UiPath. The former makes self-directed materials-handling delivery platforms that look a lot like Symbotic’s pallet-transporting carts, while the latter — mostly a workflow software service provider — is easing its way into the business with manufacturing automation solutions like Kuka AG’s physical robotics capable of painting, welding, packaging, and more.

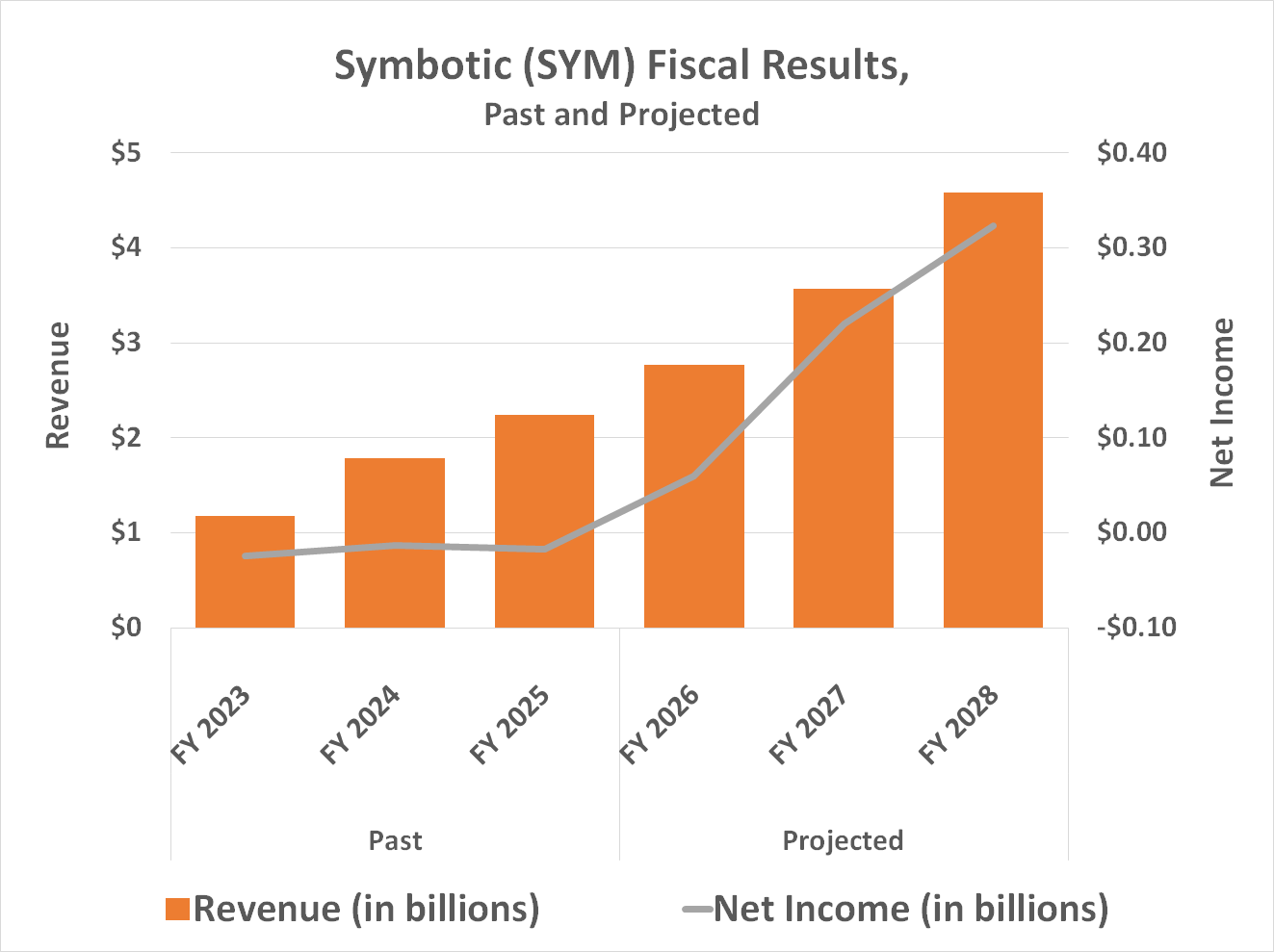

Symbotic arguably has an advantage on all of these other prospective investments though. That is, it’s well proven. The company generated a little more than $2.2 billion worth of revenue last fiscal year, up 26% year over year. And while still technically suffering losses on a trailing basis, it’s making progress on this front, with this year’s and next year’s projected top-line growth of around 24% and 28%, respectively, likely to push the company out of the red and permanently into the black.

Data source: Simply Wall St.

On the verge of reaching this major milestone, this stock that’s made no net progress since August of last year could soon start moving higher again. Only this time, unlike previous rally efforts, the advance should be sustained by continually growing profits.

Yes, it brings above-average risk to the table, and will almost certainly remain volatile even if it starts making bullish progress soon. That’s just the nature of the stock. If you can stomach the risk and inevitable volatility though, its potential upside may be worth it for most growth-seeking investors.