Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE.

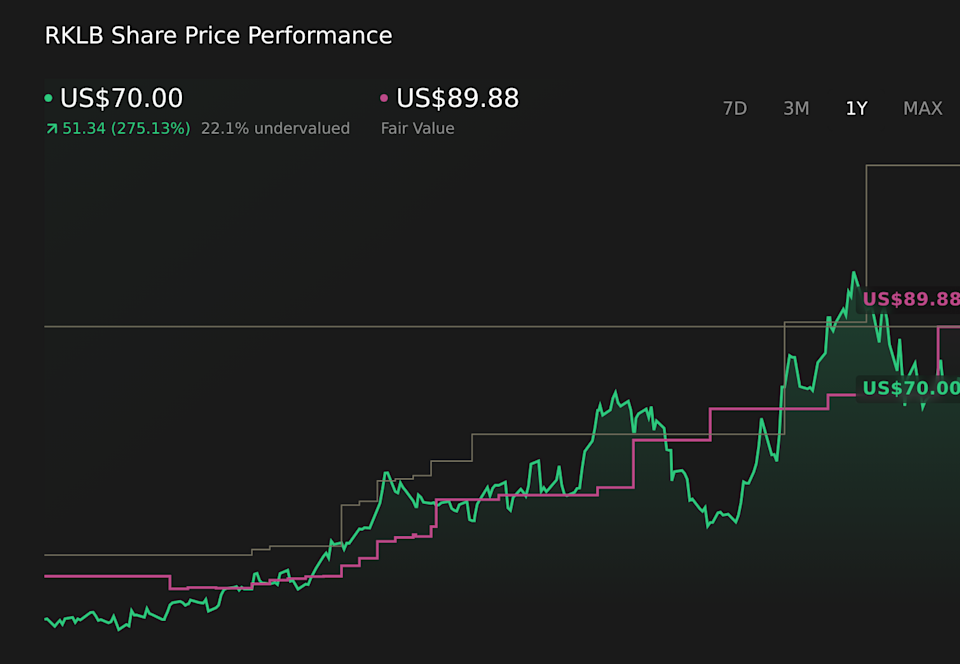

Analyst fair value for Rocket Lab has shifted from US$83.96 to US$89.88, giving investors fresh context for where some on the Street currently anchor their views. The move lines up with more positive research commentary overall, with several bullish analysts lifting targets even as others highlight execution and growth expectations as key watch items. As you read on, you will see how these changing targets, mixed opinions, and recent company updates feed into an evolving narrative you can track over time.

Stay updated as the Fair Value for Rocket Lab shifts by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Rocket Lab.

Cantor Fitzgerald raised its Rocket Lab price target to US$85 from US$72 and kept an Overweight rating, highlighting the Geost acquisition as a key step that adds payloads as a new offering and could help the company compete for U.S. National Security Missions.

Roth Capital lifted its target to US$90 from US$75 and maintained a Buy rating, pointing to what it calls steady space systems revenue, very strong launch results in the quarter, and a growing backlog in space systems as core parts of the thesis.

Stifel also moved its target to US$90 from US$85 while keeping a Buy rating, and Deutsche Bank took its target to US$73 from US$55, adding to the cluster of higher valuation anchors after recent updates.

KeyBanc downgraded Rocket Lab, arguing that growth catalysts are now well known, which for more cautious investors can raise questions about how much upside is already reflected in current expectations.

TD Cowen flagged that a Neutron rupture could affect launch timing, putting execution risk and schedule reliability on the radar for investors who are focused on how closely operations track to plan.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

NasdaqCM:RKLB 1-Year Stock Price Chart

NasdaqCM:RKLB 1-Year Stock Price Chart

We’ve flagged 3 risks for Rocket Lab. See which could impact your investment.

Fair value moved from US$83.96 to US$89.88.

Assumed revenue growth moved from 37.69% to 37.52%.

Assumed net profit margin moved from 10.12% to 15.70%.

Assumed future P/E multiple moved from 465.10x to 316.91x.

Discount rate moved from 7.47% to 7.64%.

Story Continues

Narratives connect Rocket Lab’s business story to a set of financial assumptions, so you can see how launches, contracts, and setbacks flow through to an earnings forecast and fair value. They refresh as new guidance, test results, and contract wins or delays come through.

Head over to the Simply Wall St Community and follow the Narrative on Rocket Lab to stay up to date on:

How end to end space solutions, including the Geost acquisition and vertically integrated payload and satellite capabilities, are tied to potential national security and defense contracts like Golden Dome and SDA constellations.

Why higher Electron launch cadence, space systems manufacturing, and the planned reusable Neutron rocket sit at the center of the multi year revenue growth and margin improvement assumptions.

Which risks analysts are focused on, including sustained high R&D and capital spending, dependence on large government contracts, Neutron test and schedule risk, integration challenges from acquisitions, and exposure to changing launch and defense budgets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include RKLB.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com