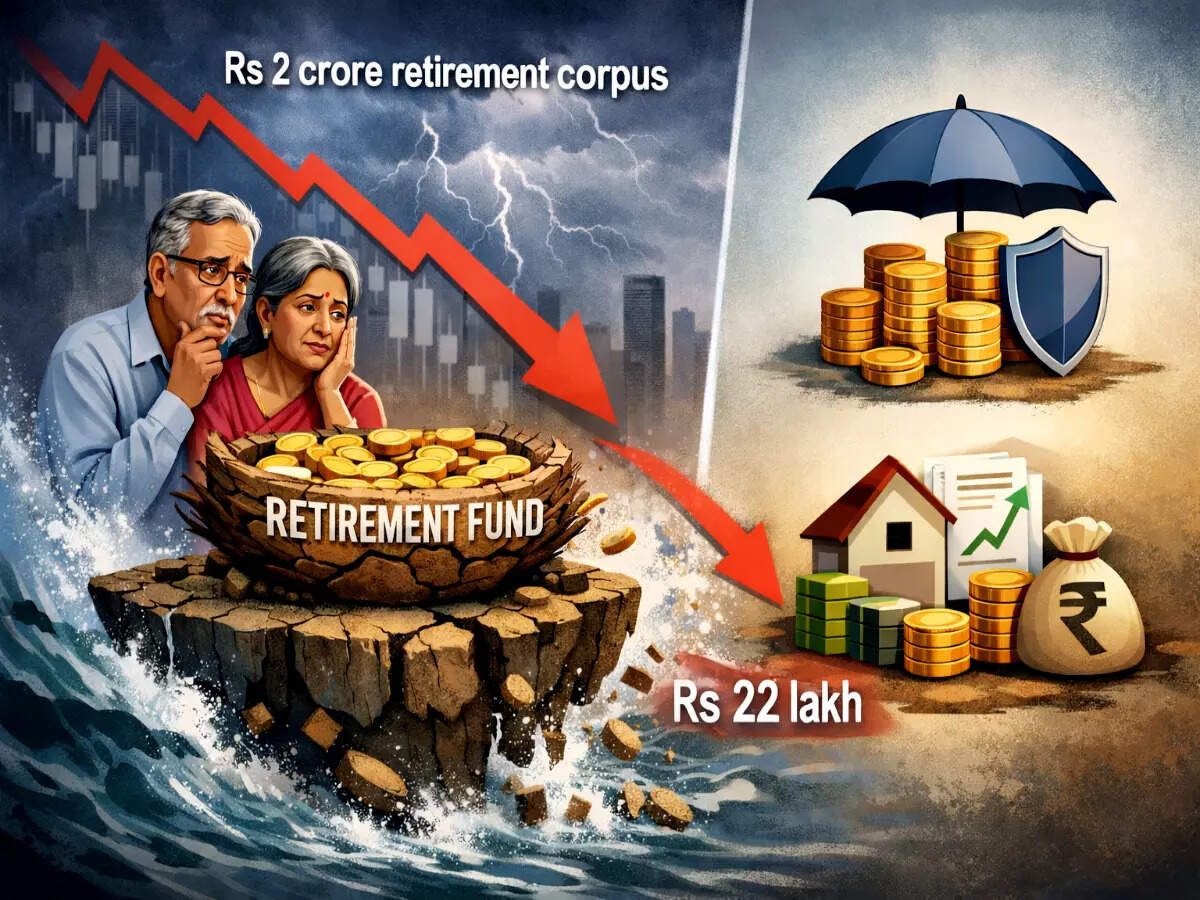

Sharp market swings can drain your retirement savings faster than you may imagine, especially if a big chunk is in stocks. For example, if you had a retirement corpus of Rs 2 crore on January 1, 2026, invested in Nifty 50 index funds, you would have seen a drop of Rs 22 lakh by March 13, 2026, 12:27 PM, due to an 11% year-to-date (YTD) decline in the index.

If your investments were spread across a broader range of indices, with 60% in the Nifty 100, 20% in Nifty Midcap 150 and 20% in Nifty Smallcap 250 indices, your fund would have lost over Rs 18.40 lakh..

For those nearing retirement, market volatility can impact their corpus severely if a significant part is in equities.

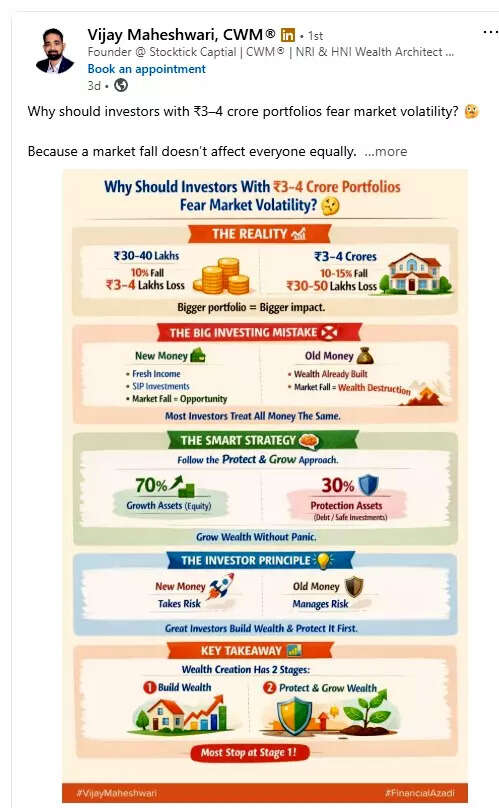

Financial expert Vijay Maheshwari recently shared on LinkedIn why investors with Rs 3-4 crore portfolios should fear market volatility. He highlights a common mistake that many people close to retirement make and offers strategy to avoid corpus depletion.

ET Online

ET Online

Retirement planning

Nifty indices’ performance since Jan 1, 2026 and corpus depletion

Index Performance Corpus value on Jan 1, 2026 Corpus value on March 11 Loss Nifty 100 -10.31% 1.2 crore (60%) 1.076 crore Nifty Midcap 150 -9.03% 40 lakh (20%) 36.28 lakh Nifty Smal cap 250 -10.72% 40 lakh (20%) 35.71 lakh Corpus value Rs 2 crore (100% Rs 1.82 cr (approx.) Rs 18.41 lakh (approx.) Source: NSE website

Rs 30 lakh -Rs 50 lakh loss on Rs 3 cr-4 cr portfolioMaheshwari tells that if someone has a Rs 30 lakh-Rs 40 lakh corpus and the market falls by 10%, they will lose Rs 4 lakh-Rs 5 lakh of their corpus value.

However, if the corpus is Rs 3 crore to 4 crore, and the market loses 10%-15%, the loss can be up to Rs 50 lakh.

Big investing mistakeMaheshwari describes two scenarios proving how a market fall can work in different ways for a new investor and one with old money.

In case of a young investor, if the market falls, they can start making investments through systematic investment plan (SIP) to make the most of the opportunity. They can do so for the simple reason that they can wait for the market to recover.

But for someone has already amassed wealth, a market fall will lead to wealth destruction.

In nutshell, while new investors can take it on the chin, old investors need to learn to manage risk.

What should investors who are going to retire soon do?Maheshwari suggests that investors nearing retirement should follow the protect and grow approach where they can invest 70% of their corpus in growth assets such as equities and 30% in protection assets such as debt and safe investments.Wealth creation has two stages The expert says that retirement planning is a two-step strategy where an investor can first build wealth and then protect and grow it.What should be your key tactics to protect your Rs 1 crore- Rs 2 crore retirement corpus from market swings?

Advice to long-term investors

Vinayak Magotra, Product Head & Founding Team, Centricity WealthTech, says If the retirement corpus is invested in equities and the investment horizon is more than five years, it is generally advisable to ride through market corrections rather than reacting to short-term volatility. Market declines are a natural part of the investment cycle, and long-term investors tend to benefit from staying invested through these phases.

Advice to short-term investors

However, if a part of the corpus is needed in the near term, investors should gradually rebalance their portfolio and shift allocations towards relatively stable hybrid strategies such as balanced advantage funds or equity savings funds, which can help moderate downside risk while still participating in equity markets, suggests Magotra.Suggestions for investors not comfortable with equality volatility

For investors who are uncomfortable with equity volatility, Magotra suggests allocating a portion of the portfolio to performing credit AIFs or high-quality Non-Convertible Debentures (NCDs), which can provide relatively stable accrual-based returns and help preserve capital.How to protect a Rs 1-crore retirement corpusChakrivardhan Kuppala, Co founder and Director of Prime Wealth Finserv, Hyderabad, says with a Rs 1 crore corpus, the margin for error becomes smaller and the structure tends to lean more heavily toward stability because essential expenses must be covered with greater certainty.

“A larger share of the portfolio typically sits in predictable income sources such as government-backed savings schemes, deposits, or high-quality fixed-income instruments. Growth assets like equity may still form a part of the portfolio because inflation remains a long-term risk, but the allocation is usually lower compared with larger retirement portfolios,” Kuppala.

How to protect Rs 2-crore retirement corpusKuppala says with a Rs 2 crore retirement corpus, the focus typically shifts to structuring the money according to time horizon.

Kuppala recommends that investors should invest a portion of the corpus equivalent to two to three years of living expenses in highly liquid and stable instruments such as savings accounts, bank deposits or liquid funds.

“This portion acts as a buffer for regular spending,” says Kuppala.

For the next three to five years of expenses, Kuppala suggests investing in relatively stable income assets such as government-backed schemes, high-quality debt instruments or similar fixed-income products.

“The remaining portion of the corpus continues in diversified growth assets such as equity or balanced funds, which help the portfolio keep pace with inflation over the long term,” says Kuppala.

Investment strategy for Rs 2-crore corpus

Investment Horizon Where to Invest Purpose 2–3 years of living expenses Savings accounts, bank deposits, liquid funds Acts as a buffer for regular spending and provides high liquidity 3–5 years of living expenses Government-backed schemes, high-quality debt instruments, other fixed-income products Provides relatively stable income and moderate safety Remaining corpus (long term) Diversified growth assets such as equity or balanced funds Helps the portfolio grow and keep pace with inflation over the long term

Kuppala says with this structure, near-term expenses remain insulated from market movements.

What he is saying that one can’t take risk with money they require for their immediate years after retirement. So, it should be invested in low-risk, high liquidity instruments, such as savings accounts, FDs and liquid funds.

For the subsequent years, the investor can invest in instruments providing relatively stable income and moderate safety.

For long-term needs, one can invest in riskier assets such as hybrid funds or equity which provide growth.