We all know how Trump likes to make up crazy numbers, which his lackeys then repeat. He has $18 trillion in foreign investment coming into the country. He won the 2020 election by millions of votes. He is lowering drug prices by 1,500 percent.

We can usually just laugh these off as the ramblings of an old man suffering from dementia. But there is one crazy Trump number that it is important people know should not be taken seriously. This is the claim on stock returns that lackeys like Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick tout when telling people how much money their newborn kid can get from their Trump Accounts.

In their telling, the $1,000 that the government is putting into the Trump accounts, starting this year, will grow to more than $590,000 when the kid reaches retirement age. If their families are able to put the full $5,000 allowed into the account, they will have more than $2.5 million when they reach retirement, and that assumes no further contributions. (They can put up to $5,000 a year into the account.)

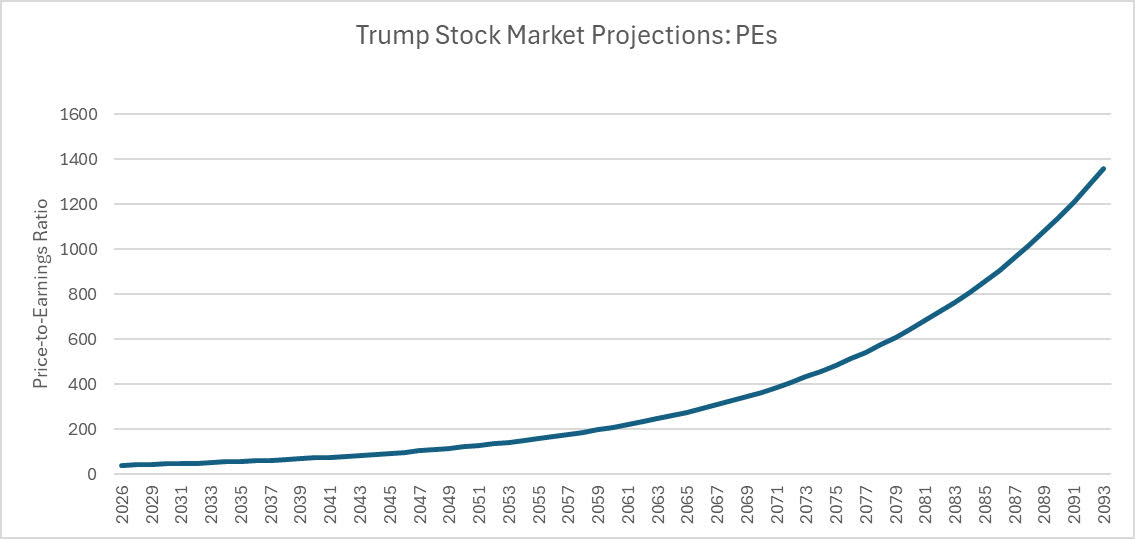

That’s a serious chunk of money, even if we cut it by four to adjust for projected inflation over this period. It’s also serious nonsense. The problem is that there is no plausible story whereby the stock market can provide the 10 percent nominal return the Bessent-Lutnick gang is pushing. In their story, price-to-earnings ratios would have to go through the roof.

By 2093, when our newborn kid plans to cash out the fortune in their Trump Account, their 10 percent compounded returns would imply a price-to-earnings ratio (PE) of almost 1,400. The problem is that will the Trump accounts are growing at the rate of 10 percent a year, the economy and corporate profits are only growing at a bit less than 4.0 percent annually. This causes the PE to go through the roof.

This is not an old problem. Some of us have been trying to point this one out to arithmetic fans ever since the Social Security privatization debates of the 1990s. While the stock market has historically provided returns that were higher than the economy’s rate of growth, this was possible because the PE in the stock market has averaged around 14 to 1. It is currently close to 40 to 1.

The simplest way to calculate the real rate of return consistent with a stable PE is to simply take the reciprocal of the PE ratio. When the PE ratio is 14, the sustainable real rate of return is 7.1 percent. Adding in inflation that has averaged close to 3.0 percent gets the 10.0 percent that we can see going back 100 years.

But with the current PE close to 40, this sort of rate of return is not possible unless the PE gets ever higher. The sustainable real rate of return would be just over 2.5 percent. Adding in projected inflation of 2.3 percent gets us to 4.8 percent, well below the Bessent-Lutnick promise.

The moral of this story is that just as no one in their right mind would take health advice from RFK Jr., no one in their right mind should take financial advice from the Bessent-Lutnick gang. As the saying goes, do your own research.

This first appeared on Dean Baker’s Beat the Press blog.